Rare Earths and the Dual-Price Market

How SMM's FOB Quote Illustrates the Cost of Western Dependency

Rare-earth pricing now matters to anyone who builds EVs, wind turbines, robots, motors, defence systems or industrial platforms, not only to metals traders. The reason is that material which cannot be delivered has no usable price at all.

A chokepoint material

Neodymium-iron-boron magnets are the strongest permanent magnets in commercial production, and their performance depends on two elements, neodymium and praseodymium, which are almost always sourced and traded together as a single alloy input known as NdPr oxide or NdPr metal. These magnets sit inside EV traction motors, wind turbine generators, robotic actuators and precision defence systems, wherever a large amount of magnetic force is required from a small, lightweight component. No substitute technology matches them at scale, which is why NdPr specifically, rather than rare earths as a broad category, is the material chokepoint for electrification.

NdPr, together with a smaller volume of heavy rare earths such as dysprosium and terbium, used to hold magnet performance at high temperatures, is what makes the wider electrification of the global economy possible. These magnets let an electric motor convert stored energy into mechanical force at an efficiency fossil-fuel drivetrains cannot match, and that efficiency gain, paired with continuing improvements in battery energy density, is the basis of the shift now under way across transport, power generation and industrial equipment. Electrification is a step change in energy conversion efficiency, and NdPr magnets are one of the two components, alongside the battery itself, that make it physically possible.

China's refining advantage

China's pricing power does not come from reserves. It comes from processing. China holds an estimated 40% of global rare-earth reserves and around 60% of mining output, but its share of separation and refining capacity, the step that turns raw ore into tradeable oxide, runs above 90%. Refining is the harder step to replicate, and that is where China's advantage sits. Whoever controls refining controls the price. China controls the refining.

A small market with outsized leverage

It is worth stating the size of this market directly. The global rare earth magnet market is worth somewhere in the region of US$15-20 billion a year, depending on which estimate you use. Global copper is worth roughly US$250-300 billion a year, so rare-earth magnets are perhaps one-fifteenth the size.

That comparison is the reason this material is worth writing about. A market smaller than most countries' agricultural exports determines whether EV motors, wind turbine generators, robotics actuators and a meaningful share of precision defence systems can be built at scale.

There is no substitute technology for what NdPr magnets do and no meaningful production base for them outside China. That mismatch between size and leverage is what asks the pricing questions in the rest of this piece worth taking seriously.

Two prices, one market

China's rare-earth market is priced in two ways: delivered-to-works, the price with material already delivered to the buyer's plant in China, and FOB (free-on-board), the price once material is loaded onto a vessel at a Chinese port, ready for export. FOB is the standard basis for international trade because it marks the point at which cost and risk pass from seller to buyer.

SMM as the benchmark

SMM, Shanghai Metals Market, is the industry-standard price-reporting agency for Chinese metals and the highest-liquidity benchmark in this sector. It is not the only price-reporting agency covering rare earths. Argus and a handful of other platforms publish periodic rare earth market insight, and Benchmark Mineral Intelligence introduced its own ex-China price assessments in mid-2025, but Benchmark's ex-China grades are published monthly.

SMM's advantage is frequency and depth: its domestic China spot prices are assessed daily, and its FOB China price points, added from late 2025 into early 2026, are updated weekly. That higher-frequency liquidity is what makes SMM's data usable for the kind of granular, near-real-time comparison this piece relies on, and it is why SMM, not a monthly assessment, is the reference point throughout.

SMM has faced criticism in some quarters for being politically influenced, given its location and proximity to the market it reports on. That criticism is largely unfair. SMM operates within the constraints of where it sits, as any price-reporting agency does, but the evidence suggests it tries to be as independent as the environment allows, and its methodology, specification details, and price-submitter process are more transparent than the criticism usually credits.

The limits of a domestic price

The more difficult problem lies one level up and is not about SMM. A domestic Chinese spot price, however, honestly reported, cannot be representative of a global market because it reflects only transactions within China. The issue is not that the quote is biased. It is that China is the market, to an extent that makes a purely domestic price look like the whole picture when it is only one side of it.

The FOB quote goes some way to addressing that by putting a number on the export side of the transaction for the first time. But going some way is not the same as solving it, and there is a real case that the industry needs an independent, high-liquidity, ex-China benchmark of its own rather than relying on a China-based quote, however well run, to stand in for a market it can only ever half describe.

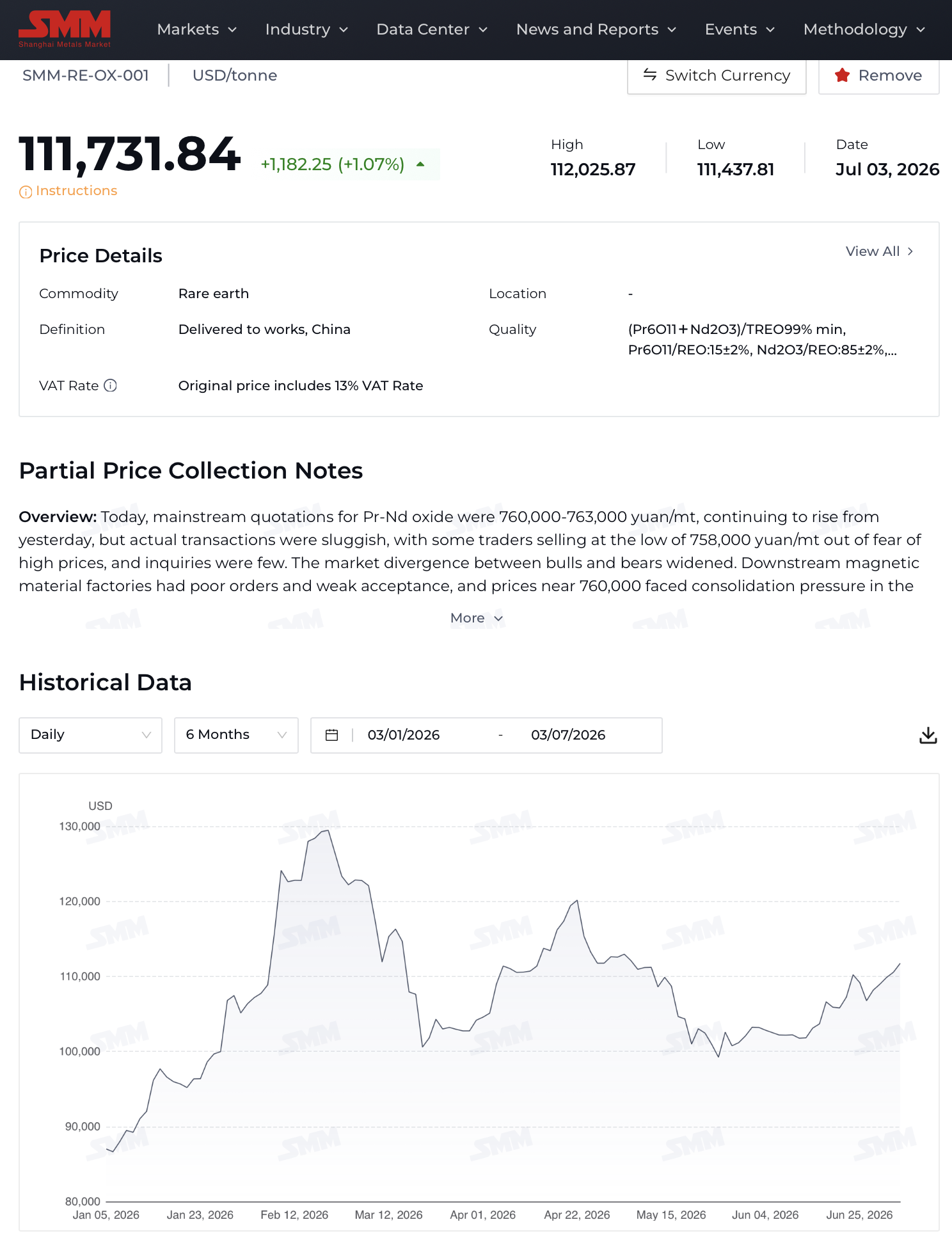

The domestic blend: SMM-RE-OX-001

SMM publishes a dedicated Pr-Nd Oxide product, SMM-RE-OX-001, specified to GB/T 31965-2015 as Nd₂O₃/REO 85±2% and Pr₆O₁₁/REO 15±2%. As of 1 July 2026, this 85/15 internal blend traded at approximately US$109.87/kg (US$109,869.92/tonne), delivered to works inside China, VAT-inclusive, under China's standard 13% VAT. This is the cleanest internal China reference point because it is an actual traded basket rather than a synthetic blend built from standalone oxide quotes.

Adjusting for specification and VAT

Two adjustments matter before this figure can be compared to anything traded outside China. The first is specification. The 85/15 Nd/Pr ratio used domestically is not the basket the wider market usually references; most NdPr FOB and offtake pricing is quoted on a 75/25 basis. Inside China, this barely matters because standalone Nd₂O₃ and Pr₆O₁₁ are currently priced close to each other, so an 85/15 basket and a 75/25 basket built from the same internal quotes land in roughly the same place. FOB is different: neodymium carries a large premium over praseodymium there, so comparing an 85/15 domestic quote directly against a 75/25 FOB number is not like-for-like, and any resulting gap is a specification artefact rather than a market signal.

The second is VAT. The domestic 85/15 price is VAT-inclusive; the 13% is paid by the Chinese buyer and forms part of the domestic transaction price, and should not simply be stripped out to create an FOB-comparable number. Rare earths carry no export VAT rebate, so the VAT a domestic buyer pays and the VAT cost an exporter cannot recover sit on different sides of the transaction and are not interchangeable. The domestic price already includes VAT paid by the Chinese buyer, while FOB-side costs are pushed up, not down, because input VAT cannot be reclaimed against rare-earth exports as it can for rebate-eligible products. The build-out from FOB toward landed US cost reflects this second effect; it is not a reversal of the first.

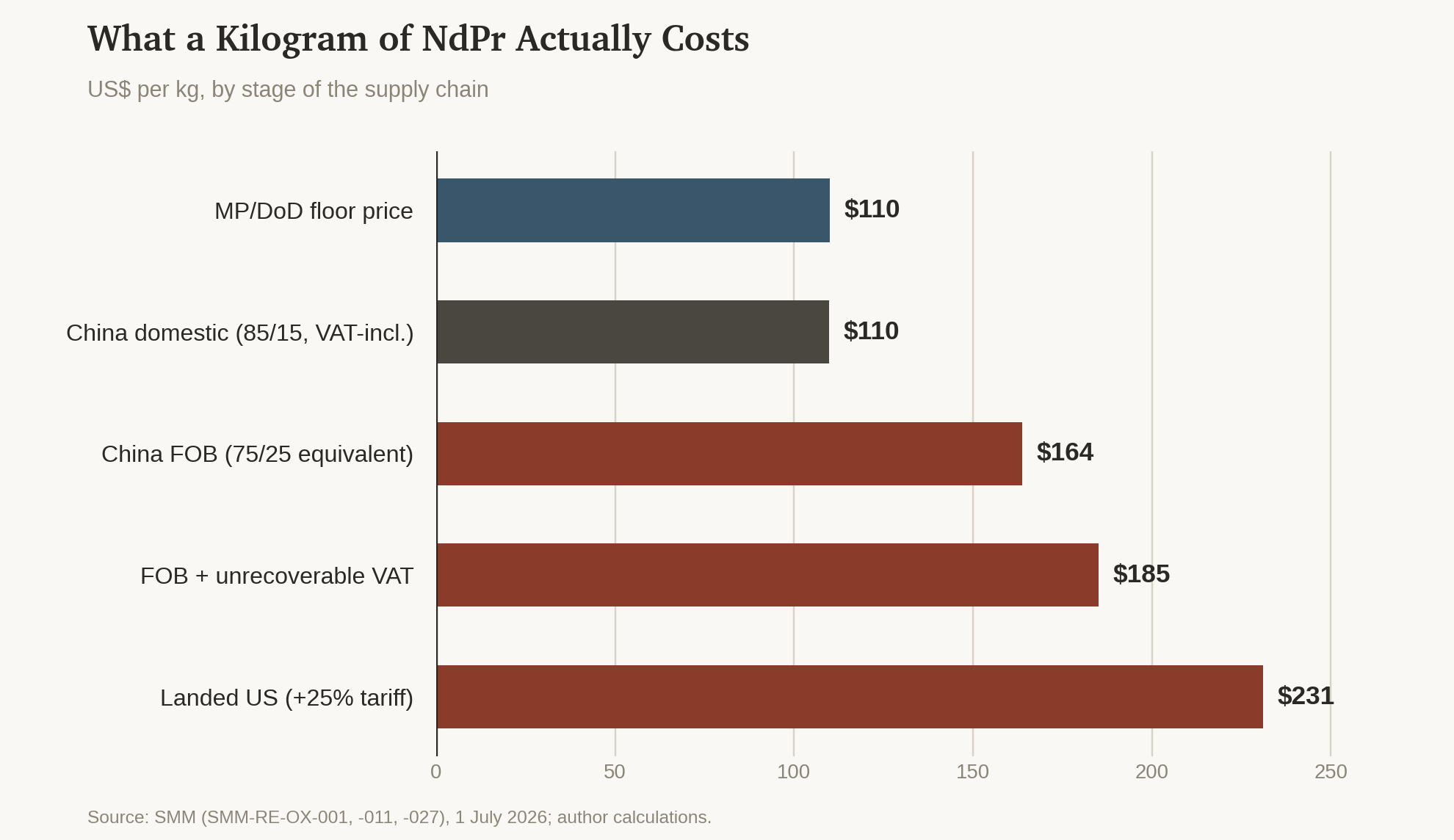

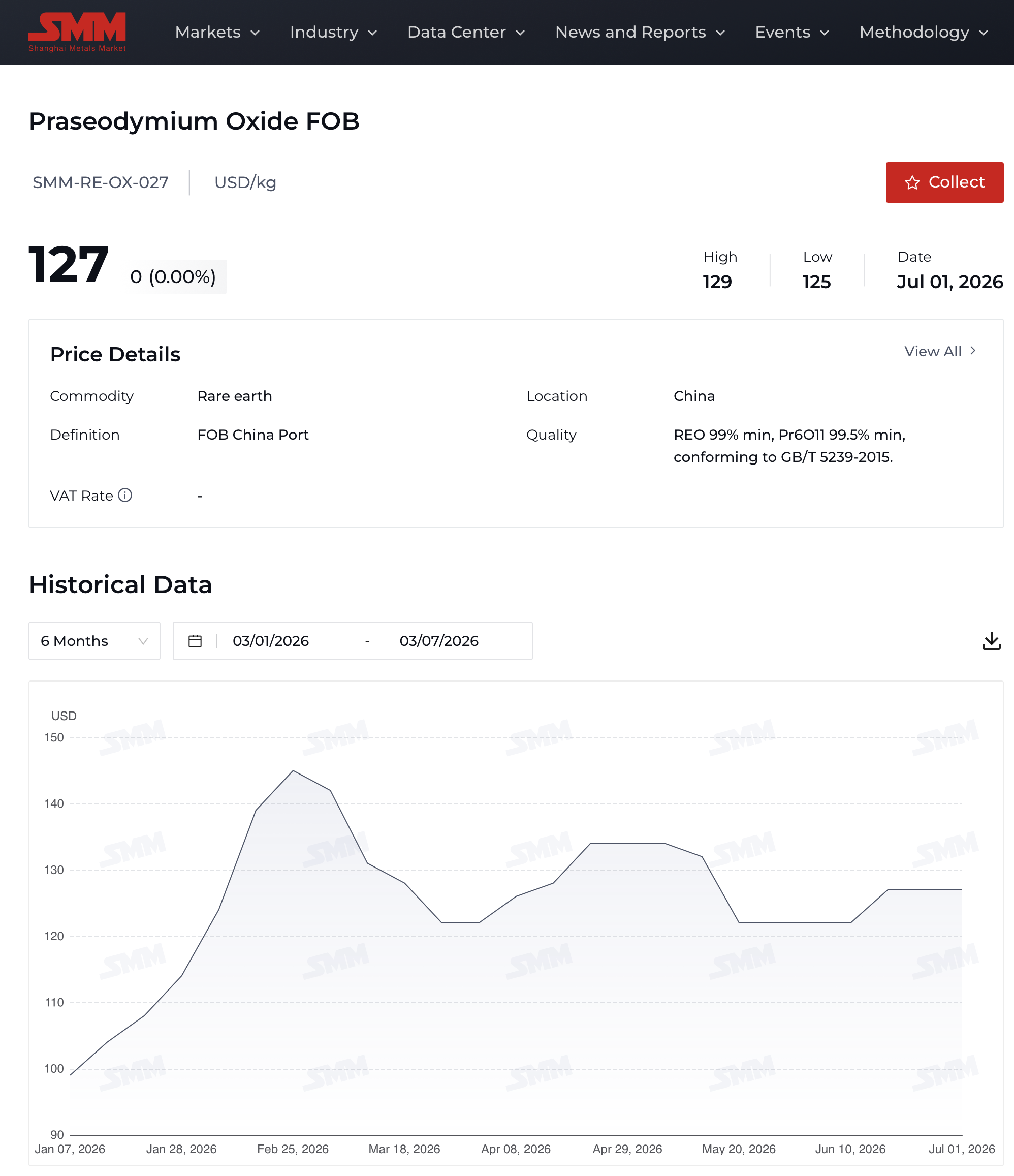

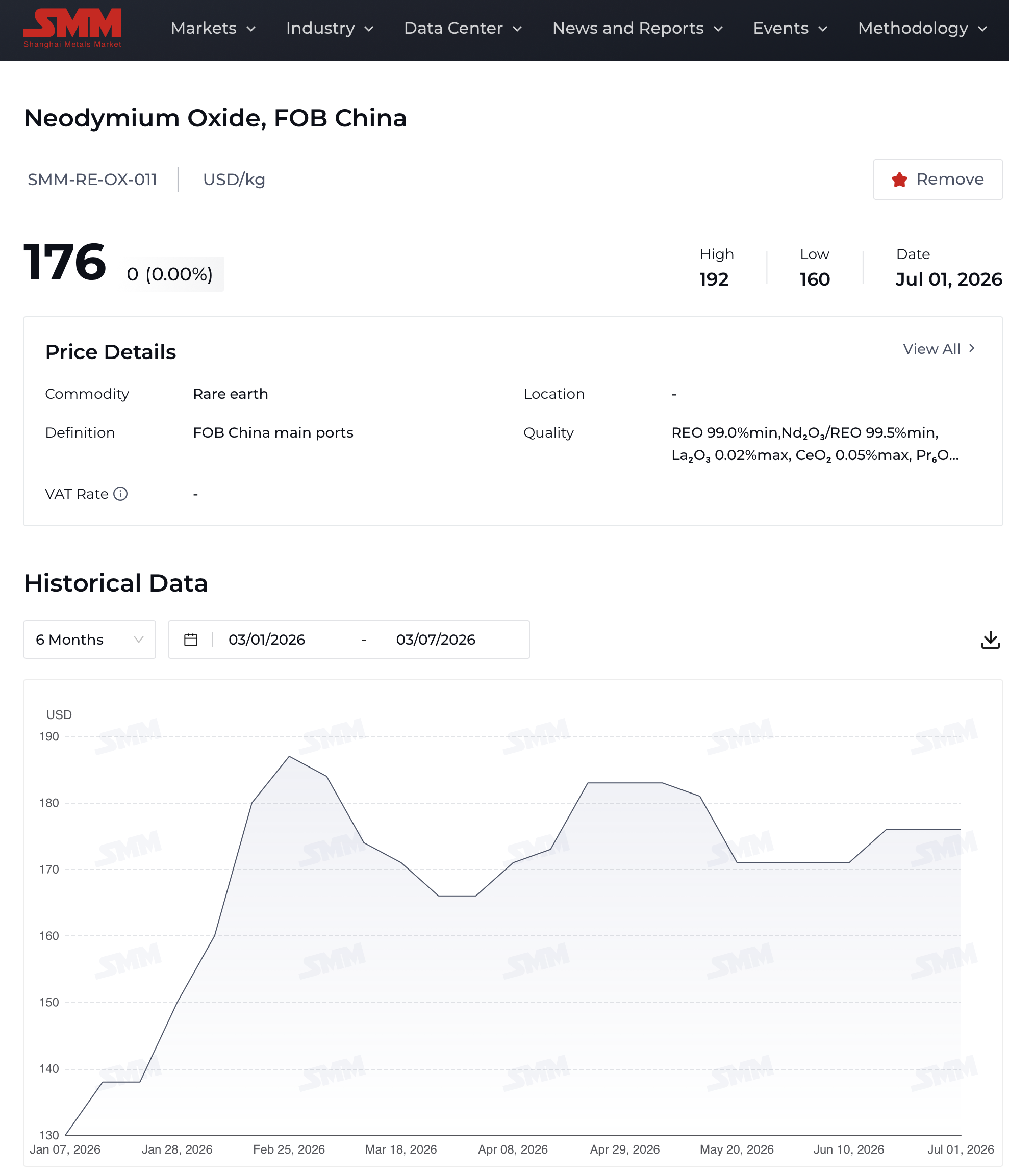

The FOB numbers

The China FOB market tells a different story. As of 1 July 2026, SMM quoted neodymium oxide (SMM-RE-OX-011, FOB China main ports) at US$176/kg and praseodymium oxide (SMM-RE-OX-027, FOB China Port) at US$127/kg. Recalculated as a 75/25 NdPr basket:

0.75 × US$176 + 0.25 × US$127 = US$132.00 + US$31.75 = US$163.75/kg

Add unrecoverable VAT exposure, and the cost basis moves toward US$185/kg. Into the United States, with a 25% tariff on top, the landed entry cost can move toward US$231/kg

That is not a typical pricing spread: roughly US$110/kg domestic against US$164/kg FOB-equivalent before VAT and tariff effects, and it shows two markets rather than one. China's internal spot reflects the price inside China's industrial system. China FOB reflects overseas demand competing for

restricted exportable supply. FOB is a real market price, but it is a price formed under restricted supply.

Feedstock under pressure

Until SMM began publishing FOB prices in earnest at the end of 2025, the only rare-earth price quotation available to the market was the Chinese domestic spot price. That price reflects what Chinese buyers are paying for spot tonnes inside China, and read on its own, over a long enough run, it is a reasonable proxy for China approaching the limits of its own capacity, whether that constraint sits in feedstock or in processing.

For most of the past decade, that constraint was rarely a feedstock. China could supply its own market from its own ore with little difficulty, so a domestic price spike more often signalled processing bottlenecks or a genuine demand surge than any shortage of raw material. That has started to change.

Feedstock has become a live issue over the past two years because a material share of China's heavy rare-earth ore, dysprosium and terbium in particular, is sourced from Kachin State in northern Myanmar, and the civil conflict there has repeatedly disrupted those flows, including the loss of the Pangwa and Chipwi mining hub to Kachin forces in October 2024 and further supply interruptions during the fighting around Bhamo since.

Feedstock has also narrowed from the other direction. MP Materials, which had shipped its Mountain Pass concentrate to Shenghe Resources in China for processing, ceased those sales in mid-2025 as part of its DoD-backed floor-price agreement, redirecting output toward its own US processing and magnet capacity instead.

In December 2025, Brazil's Serra Verde, whose Pela Ema deposit is one of the few scalable non-China, non-Myanmar sources of dysprosium and terbium, renegotiated its roughly decade-long Chinese offtake agreements down to expire at the end of 2026, roughly eight years early, clearing the way for Western buyers once its output is freed up; a US$565 million DFC loan and a subsequent US$2.8 billion acquisition by USA Rare Earth followed within months.

None of these three cuts, Myanmar, MP, and Serra Verde, is individually large next to China's total feedstock base, but all three point the same way, and all three are recent. A domestic price spike now carries a second possible reading it did not carry before: not only is China approaching its processing limits, but its own feedstock security is being tested from more than one direction at once, on a border it does not fully control and from suppliers that have chosen to walk away.

The Ngualla exception

There is one acquisition running the other way, and it is worth being precise about what it does and does not change. In September 2025, China's Shenghe Resources completed a takeover of Peak Rare Earths, the owner of the Ngualla deposit in Tanzania, one of the largest NdPr-weighted deposits outside China, for roughly A$158-200 million. Against the Ore Reserve's contained NdPr, which values the resource in the ground at somewhere around US$0.55 to 0.70 per kilogram, a distressed price by any measure, made possible by Peak's collapsed share price, down from over A$1 in 2021 to around A$0.12 before the deal.

But this is not really a counterexample to the feedstock argument, for two reasons. First, Shenghe already held roughly 20% of Peak and 100% of its offtake before the takeover, so this consolidated a position it effectively already controlled rather than opening a new one; Ngualla's concentrate was always contracted to flow into Chinese processing regardless of who owned the equity.

Second, Ngualla is unlikely to be developed soon. Tanzania's government holds only a 16% free-carried interest, but its 2017 mining law tightened equity requirements and restricted the export of unprocessed concentrate, and the in-country processing terms Shenghe would need to finalise before a final investment decision have remained under negotiation into 2026 rather than resolved.

Some recent reporting suggests Shenghe may be content to leave the project mothballed rather than rush to meet Tanzanian in-country processing demands, particularly if China's own restrictions on exporting mining equipment, technology and personnel for critical-minerals projects abroad make that harder to justify. Tanzania has little practical leverage to force the pace: a free-carried minority stake gives it a seat at the table, not control over the timeline, and that will not change unless Tanzania rewrites the terms it negotiated with a different counterparty in mind.

The result is not additional supply for anyone. Ngualla is not adding tonnes to China's own processing pipeline, and it is not adding tonnes to the rest-of-world supply chain either; one of the world's largest NdPr-weighted deposits sits denied to both, which adds to the supply and price pressure described in this piece.

It also leaves Tanzania holding a free-carried stake in a mine that produces nothing, no royalties, no jobs, no processed value, for as long as the standoff over in-country processing terms continues. Read alongside Myanmar, MP and Serra Verde, Ngualla looks less like China building a new pillar of supply and more like China banking a cheap option against a future it is in no hurry to bring forward, at a cost being paid, for now, by Tanzania as much as by anyone else.

None of this is necessarily permanent. The standoff would break if a Western or Tanzanian-aligned party were willing to fund in-country processing on Tanzania's terms rather than wait for Shenghe to do so on its own. But that is not where investor capital is currently going in Africa, at least on paper.

Rest-of-world projects in the queue

Angola's Longonjo project is already at the construction stage with a 2027 commissioning target, backed by financing secured in December 2025 and an offtake agreement with the German magnet maker Vacuumschmelze. Malawi's Kangankunde project reached a final investment decision in August 2025, with Lindian Resources reporting construction progress through its own announcements toward a targeted Q4 2026 first production.

Both projects are further along the development curve and further along the queue for capital and offtake attention than Ngualla currently is. Ngualla sits behind them not because it is a worse deposit, but because it is a better deposit tied up in a worse negotiation.

Export controls as domestic supply security

That tightening feedstock picture points to an easy-to-miss reading of the export controls themselves. The controls are usually discussed as a form of leverage in the US-China trade relationship, and they clearly function that way. But leverage is not the only thing they do, and possibly not even the main thing. With a US$50-US$90 spread between the domestic price and the FOB-equivalent price for the same tonne of NdPr, a Chinese producer facing no export restrictions has every commercial incentive to sell into the export market rather than supply Chinese magnet and EV manufacturers at the lower domestic price.

Export controls, licensing and quotas do not only ration what the West receives; they also cap how much of a tightening domestic supply Chinese producers are permitted to divert abroad in pursuit of that spread. Read that way, the controls look less like a tool built for foreign policy that happens to also secure domestic supply, and more like a domestic supply-security mechanism that China is willing to use for foreign policy when convenient. Without them, and with feedstock now genuinely constrained, there is little reason to think China's own producers would prioritise the domestic market over the export price they can command.

SMM's FOB quote in context

The emergence of SMM's China FOB quote should be read in that context. Western buyers were increasingly finding the daily Chinese domestic spot quote irrelevant as a procurement benchmark: it still reflected China's internal industrial cost base but no longer reflected the price, availability, or permission risk faced by overseas buyers. A delivered-to-works in China price is not the same as an exportable, licensable, deliverable Western supply price, and SMM's FOB quote did not create that split; it acknowledged it. The quote begins to monetise the scarcity component of Western dependency. It is not the full Western cost, since tariffs, protectionism, rules of origin, compliance, financing and strategic inventory can all sit on top of it, but it is the first visible price marker showing that the West is no longer dealing with the same market as China's domestic manufacturers. China's domestic spot shows China's internal industrial advantage, SMM FOB shows the scarcity premium faced by the West, and Western protectionism adds a further layer on top. That is the cost of dependency, and it is why China's rare-earth market now must be read as two markets rather than one.

Why China FOB is both useful and risky

China FOB is useful because it gives OEMs, investors and governments a financial measure of dependency, showing what overseas buyers may have to pay when they rely on Chinese exports of materials that China can restrict, license, delay or refuse. It gives OEMs a way to quantify the cost of failing to secure independent supply.

But China FOB is risky if it becomes the benchmark for building the rest-of-world supply chain. Chinese OEMs compete on China's internal pricing, now anchored to the actual traded blend at roughly US$110/kg. Western, Japanese and Korean OEMs cannot build competitive EVs, wind turbines, robots, motors, defence systems or industrial platforms if their input costs are permanently set by China FOB. China FOB prices the risk; it should not become the target. The target is a rest-of-world supply chain that can eventually compete more closely on pricing with China's domestic market, while still offering sufficient returns to attract investment.

Where the floor sits

History has already tested this. Of the two major non-China NdPr producers that scaled up around the 2011 price spike, only one survived the collapse that followed. Molycorp's Mountain Pass operation restarted into the spike, expanded aggressively, and was funded heavily by debt, with no long-term offtake or price-support structure behind it; when prices fell back, Molycorp collapsed into Chapter 11 bankruptcy. Lynas survived. The difference was not geology or grade, since both were credible deposits; it was structure. Lynas had Japan behind it through JOGMEC and Sojitz, with loan-and-equity support, offtake and a route into Japan's industrial supply chain. Japan was not simply backing a mine; it was backing supply continuity, and that is why Lynas survived the trough: it had more than a resource and a processing plant; it had a buyer-backed structure tied to strategic demand. That is the lesson now being rediscovered in the United States.

The collapse itself deserves a closer look than it usually gets, and here I will give my own reading rather than the more common one. The standard account treats 2011 as straightforward: China restricted exports, prices spiked, competitors entered, China eased off, prices fell, competitors failed. I think the mechanism was more specific than that, and the timing supports it. The US, EU and Japan took China to the WTO over its export quotas in 2012; the WTO ruled against China in March 2014; and China, having exhausted its appeal, dismantled the quota system in stages between January and May 2015. Molycorp filed for Chapter 11 in June 2015, within weeks of China's compliance deadline. That sequence is not proof of intent, but it is more specific than "prices normalised."

My own view is that China had built out mining and processing capacity through the quota years to hedge against exactly the outcome the West was pursuing at the WTO: a ruling that would force the taps back open. When that ruling landed and the quotas came off, the capacity was already there, and it flowed. Whether that was foresight or simply the ordinary lumpiness of Chinese capacity build-out meeting a sudden change in export rules, the effect was the same either way, and the timing is hard to read as coincidence. The West fought for, and won, the legal right to unrestricted Chinese rare-earth exports. What it got, within months, was a price collapse that killed the one meaningful non-China competitor the 2011 crisis had produced, and left China's market position stronger than before the case was filed.

I do not think that lesson was lost on Beijing, and I do not think it has been revised since. In the decade since, China has not, as far as I can tell, treated the West as a market to be cultivated or a supply chain to be shared. It has treated it as a sink: somewhere to place excess capacity when convenient, and somewhere to withdraw supply from when it is not. That reading fits the pattern better than the alternative, and the April 2025 controls, discussed below, support it.

OEM behaviour after 2011 was straightforward. Chinese supply remained available, and once prices normalised, OEMs went back to it. They did not maintain the offtake and pricing support needed to keep non-China alternatives alive, and there was no commercial penalty for ignoring the warning.

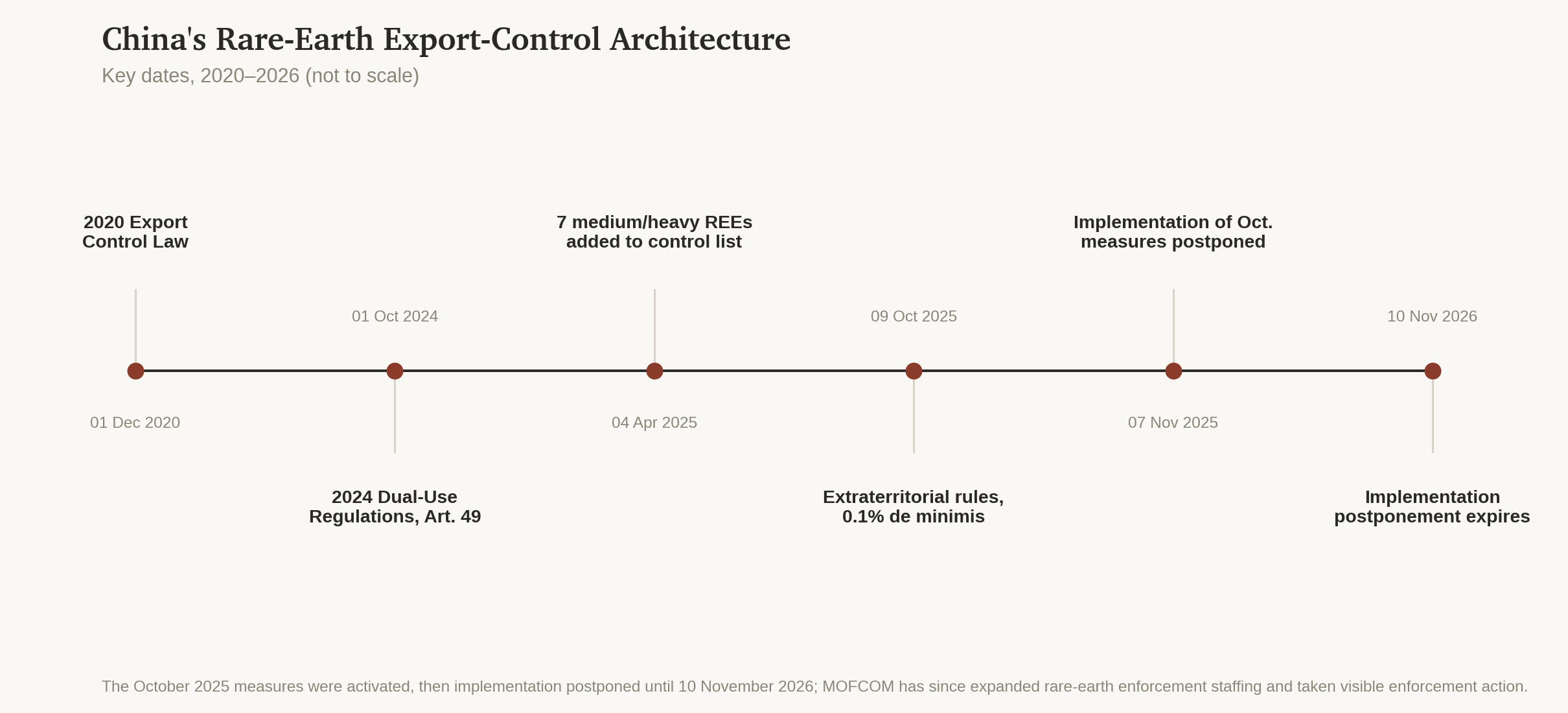

This time is different. China's modern export-control architecture rests on the 2020 Export Control Law and the 2024 Regulations on Export Control of Dual-Use Items; Article 49 of the 2024 regulation provides the legal basis for extraterritorial reach. On 4 April 2025, MOFCOM added seven medium- and heavy-rare earths, including terbium, dysprosium, samarium, gadolinium, lutetium, scandium and yttrium, to the control list, and exports now require case-by-case licences with a stipulated 45-working-day review period. On 9 October 2025, MOFCOM went further: it activated extraterritorial jurisdiction, requiring licences even for transfers of controlled rare earths between two countries outside China, and introduced a 0.1% de minimis rule for foreign-made products containing Chinese-origin rare earths alongside a 50% affiliates rule for related entities. Following US-China talks, China postponed implementation of the October measures on 7 November 2025 until 10 November 2026. That is a postponement of implementation, not a suspension of the measures themselves, and expiry of the postponement is not a review.

Why the postponement is not a wind-down

A postponement invites comparison to 2011: pressure, then relief, then a drift back to normal. Nothing in the record since 7 November 2025 supports that reading. The legal architecture, licensing bureaucracy and April 2025 controls remain in force throughout the postponement, and MOFCOM has been staffing up, not standing down, while it runs. Reporting in late 2025 indicated that its Bureau of Industry Security, Import and Export Control was launching its largest recruitment drive in nearly a decade, with the rare-earth control division a specific focus even as the truce with Washington held. Enforcement has followed the hiring. By mid-2026, a Chinese optics company chairman had been placed under compulsory measures over mis declared export documentation, MOFCOM had introduced a public reporting mechanism for strategic-mineral violations effective 1 July 2026, and China had added 10 US entities, including MP Materials and USA Rare Earth, to its export control list.

The clearest signal is Japan. Chinese customs data show that exports of dysprosium oxide to Japan stopped after October 2025, and of terbium oxide a month later, with no shipments of either recorded since. Beijing formalised the restriction through MOFCOM Announcement No. 1 of 2026, tightening licensing for medium- and heavy-rare-earth exports to Japan against the backdrop of remarks by the Japanese government on Taiwan. Two Japanese nationals, both Fuji Electric group employees, were detained in Dalian in May 2026 on suspicion of smuggling goods banned from export, and Japanese officials confirmed on 1 July 2026 that both had since been formally arrested, in mid- and late June respectively, over an alleged breach of China's rare-earth export-control law: one of the first known cases of a foreign national facing formal arrest in China over an alleged rare-earth export violation.

Read together, the Japan case shows China is willing to use this architecture with precision against a specific country and is prepared to do so again. A return to business-as-usual looks unlikely. An OEM that assumes it can wait out this cycle and return to Chinese supply is assuming an option that China is building the machinery, and now demonstrating the willingness, to switch off.

The floor mechanism

That is why OEM-backed offtake and floor structures are no longer discretionary. A floor around US$110/kg looks reasonable: it sits almost exactly on the actual traded 85/15 internal NdPr price of around US$110/kg, and well below the US$164/kg FOB-equivalent.

It is worth being clear about what this floor is and is not. It is not a subsidy intended to run indefinitely, and it is not protectionism dressed up as industrial policy; it is a temporary underwrite, priced close to where China's own domestic market already clears, that exists to get capital-intensive projects financed during the years before they have volume behind them.

It does not institutionalise a permanent scarcity premium; it creates bankability during the capital-intensive build-out phase. The mechanism gives projects the revenue visibility needed to finance assets, amortise capital expenditure and improve metallurgical performance, and as rest-of-world mining, separation and processing scale up, unit costs should compress toward industrial parity.

The floor is a bridge, not a destination: over time it should matter less as volume-driven price discovery takes over, and a floor still in place once that volume exists would be the clearest sign the model had failed.

The Lynas/Japan structure shows the principle in practice. The revised JARE agreement commits to 5,000 tonnes per annum of NdPr through 2038, with a US$110/kg floor price, while preserving Japanese access to long-term non-China supply. Mines and separators need throughput, offtake and scale; a small high-priced market may support a few assets, but it will not create a competitive industrial base. The rest of the world does not need a high-price rare-earth market. It needs a high-volume rare-earth supply chain.

The central tension

Investors need an acceptable risk-adjusted return. OEMs need secure supply at prices that allow them to compete with Chinese finished goods. Governments need resilience, but public money alone cannot create a market, and price reporting agencies can publish indices but cannot create price discovery without physical transactions. OEMs have to pick up the baton. They cannot expect China internal pricing before the non-China supply chain exists, but they also cannot accept China FOB indefinitely and expect to compete with Chinese OEMs.

Europe shows what happens when they do not. Solvay's La Rochelle plant is one of the few operating rare-earth separation facilities outside China, and CEO Philippe Kehren has been explicit that it is running at deliberately low output while it waits for exactly the kind of offtake commitment this section is describing: full-scale expansion, on the order of €100 million, is being held back for orders from automakers that have not yet arrived.

Kehren has separately described the support on offer in Europe as limited compared with what is available in North America, to the point that Solvay is now weighing a US facility alongside, or instead of, further French expansion. He is not an outlier. Other European rare-earth executives have told Reuters they cannot commit to raising output by 2030, and one industry analyst summarised the problem directly: at current price levels, most projects are not profitable without support from governments and automakers together.

That is the central tension in miniature, playing out at the one facility Europe has.

The question is not which material is cheapest today. It is what a manufacturer is prepared to pay during the build-out phase to secure supply that eventually allows it to compete. The China FOB spread helps answer that question: it gives OEMs a number to weigh against the cost of supporting independent supply through offtake, floors, prepayments, equity, inventory, or supply-chain partnerships.

The requirement of physical availability

Price is now secondary to physical availability. China FOB only matters if China is prepared to export. For a modern manufacturer, material that cannot be delivered has no price at all, and once export controls become industrial policy, procurement is no longer just cost optimisation; it becomes operational continuity. The buyer has to ask whether material will be supplied, whether a licence will be granted, whether the end use will be accepted, and whether the customer will be approved. The rest-of-world supply chain is not just competing with China FOB; it is competing with the possibility of no supply at all. OEMs need ex-China material because secure physical access to volume is now a prerequisite for manufacturing continuity.

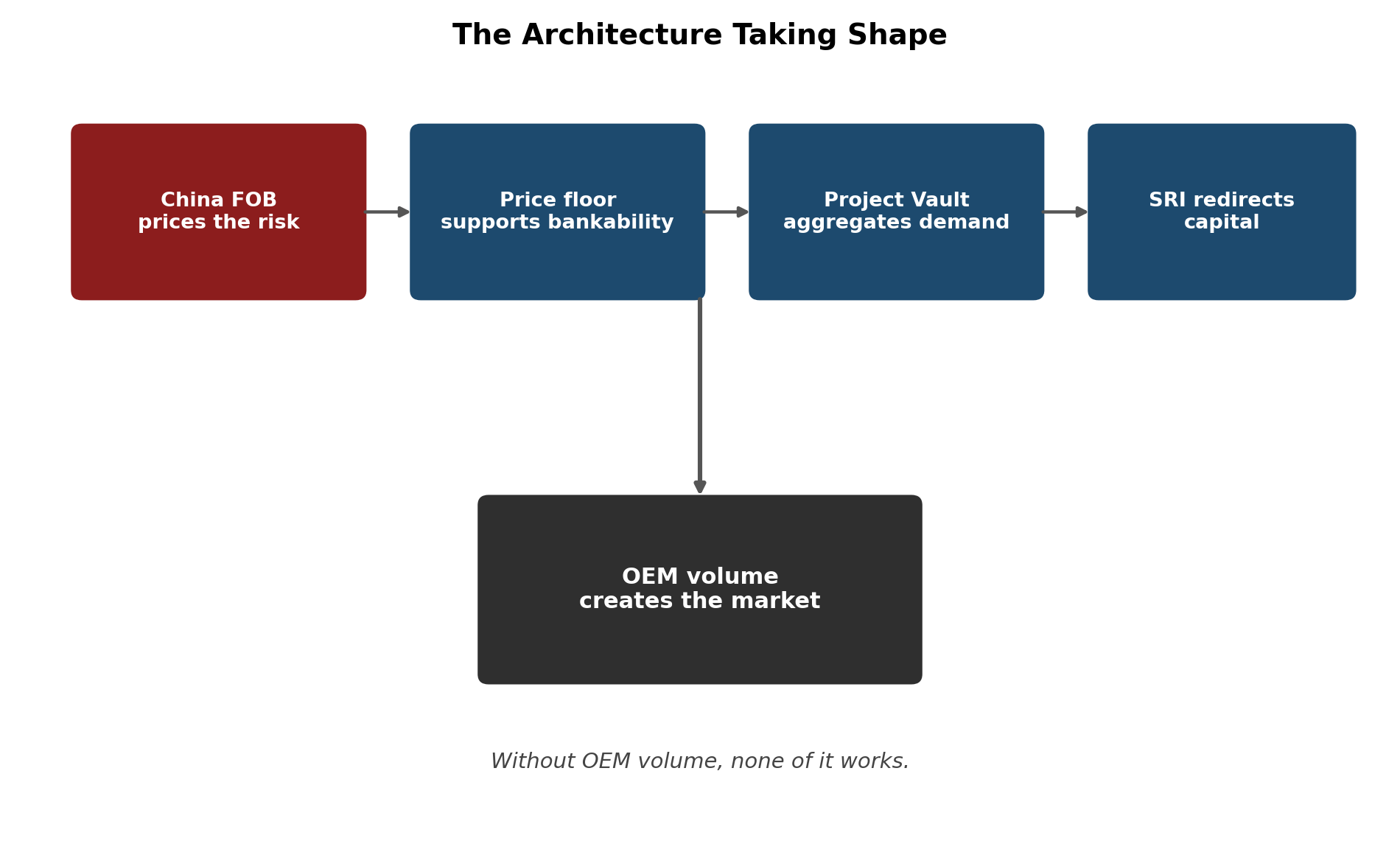

The architecture is taking shape.

This is where the US approach is more developed than others. Project Vault is intended to aggregate demand and create a physical security buffer; EXIM describes it as a US strategic critical minerals reserve structure, backed by a US$10 billion EXIM loan and nearly US$2 billion in private-sector investment. SRI-type initiatives redirect capital: JPMorgan describes its Security and Resiliency Initiative as a US$1.5 trillion, 10-year plan to finance

and invest in industries critical to economic security and resiliency, including an initial US$10 billion for direct investment in selected companies. The pieces fit together: China FOB prices the risk, a price floor supports bankability, Project Vault aggregates demand and inventory, SRI redirects capital, and OEMs create the volume. Without OEM volume, none of it works.

Japan understood the vulnerability earliest, and its approach worked. Its support for Lynas through JOGMEC and Sojitz was not just support for a mine; it combined finance, offtake, and industrial access, with the objective of ensuring continuity for Japanese manufacturers rather than simple ownership of a mineral resource. The United States is now belatedly trying to replicate that lesson on a larger scale. The contrast with MP Materials is instructive: MP did not restart as a complete Western rare-earth supply chain; it restarted primarily as a miner and concentrate producer, with its output tied to Chinese processing and offtake through Shenghe Resources. That got Mountain Pass operating again, but it did not solve the strategic problem: it gave the United States a mine, not a complete supply chain, and Western geology still depended on Chinese processing, Chinese offtake and Chinese market access.

The current US approach is an attempt to close that gap. The MP/DoD partnership creates a 10-year US$110/kg price-floor commitment for NdPr products and links price support, processing, magnet production and end-user demand. In effect, the United States is now trying to replicate the Japanese lesson: mines do not create supply-chain resilience unless finance, offtake, processing, conversion and end-user demand are tied together. Japan backed a supply chain, MP restarted as a mine, and the US is now trying to close that gap. Europe is waking up, but still leans too heavily on restrictions, targets and compliance rather than incentives, bankable demand and capital formation; restrictions can force demand away from China, but incentives are what pull supply into existence. For now, the direction of flow favours the United States because it is assembling more of the required pieces: demand aggregation, physical reserves, capital redirection, price floors and OEM participation.

Building a benchmark

Price discovery does not require every tonne to trade through an exchange, but it does require enough representative volume to create a credible reference price, which means a defined product, specification and delivery point. A ROW benchmark might be built on NdPr oxide at a clearly stated ratio, most likely 75/25 to align with market convention rather than China's domestic 85/15 norm, with defined purity, compliant origin, standard packaging and delivery to a recognised bonded warehouse, processing hub or industrial cluster. From that anchor, the market can price premiums and discounts for specification, Nd/Pr ratio, purity, origin, qualification, logistics, credit, delivery location and contract duration. The benchmark creates the anchor; the differential prices the real world.

Once that exists, the market can do its real job: deciding which resources are economic. Not every rare-earth resource should become a mine. Some deposits are geologically interesting but commercially irrelevant; others are lower grade but commercially attractive because of mineralogy, scale, infrastructure, jurisdiction, processing route, logistics, or downstream demand. Geology identifies resources. Price discovery determines which resources matter.

Conclusion

China FOB is useful because it shows what dependency costs, but it is not the price at which the rest of the world can build a competitive industrial base. The objective is not to replace Chinese dependency with a permanently high-priced Western market, but to build sufficient physical supply, processing capacity, inventory, OEM demand, and traded volume to create genuine ROW price discovery. That market must reward investment, but it must also produce material at prices that allow Western, Japanese and Korean manufacturers to compete with Chinese finished goods.

None of this happens in a vacuum, and it is worth being direct about what the evidence in this piece points to. The 2011 spike and collapse was not a one-off market correction; the timing around the WTO ruling suggests China had built the capacity to answer a forced reopening before that reopening arrived, and the West's legal victory delivered, within months, the collapse that killed its own nascent competitor. Nothing since has suggested that the lesson was forgotten. Feedstock has tightened from three independent directions at once: Myanmar, MP, and Serra Verde. Rather than easing its export controls in response, China has tightened them, enforced them against a Japanese company's own employees, and cut Japan off from dysprosium and terbium outright. Even where China has bought into the rest-of-world supply chain directly, at Ngualla, the effect has been to freeze the asset rather than develop it, denying supply to both sides rather than adding it to either. Read together, this is not the behaviour of a country treating the West as a market to be cultivated. It is the behaviour of a country that has learned to treat the West as a sink and sees no reason yet to change the lesson it drew in 2015.

Against that, the rest-of-world response so far is uneven. The United States is assembling real architecture, Project Vault, the SRI, the MP/DoD floor, but even there, the floor only works if OEM volume shows up behind it, and it has not fully shown up yet. Europe is further behind still. Solvay is running its one meaningful non-China separation facility below capacity because the automakers it is built to supply have not placed the orders that would justify expanding it, which is the central tension of this entire piece playing out at a single address in France. A floor price, a strategic reserve and a recruitment drive at MOFCOM will all matter less than whether OEMs sign the contracts. That is the one variable in this piece that is not about China at all.

China FOB prices the risk. A bankable ROW floor prices the solution. OEM volume makes the solution real. Material that cannot be delivered has no price, and every OEM still waiting to secure supply has already made that bet; they just haven't priced it yet. Until the rest of the world builds that volume, the dual-price market will keep setting the cost of dependency on its own terms.