PATIENT MONEY VS. FAST MONEY MOUNTAIN PASS, MOUNT WELD, AND THE DECADE THAT DECIDED THEM

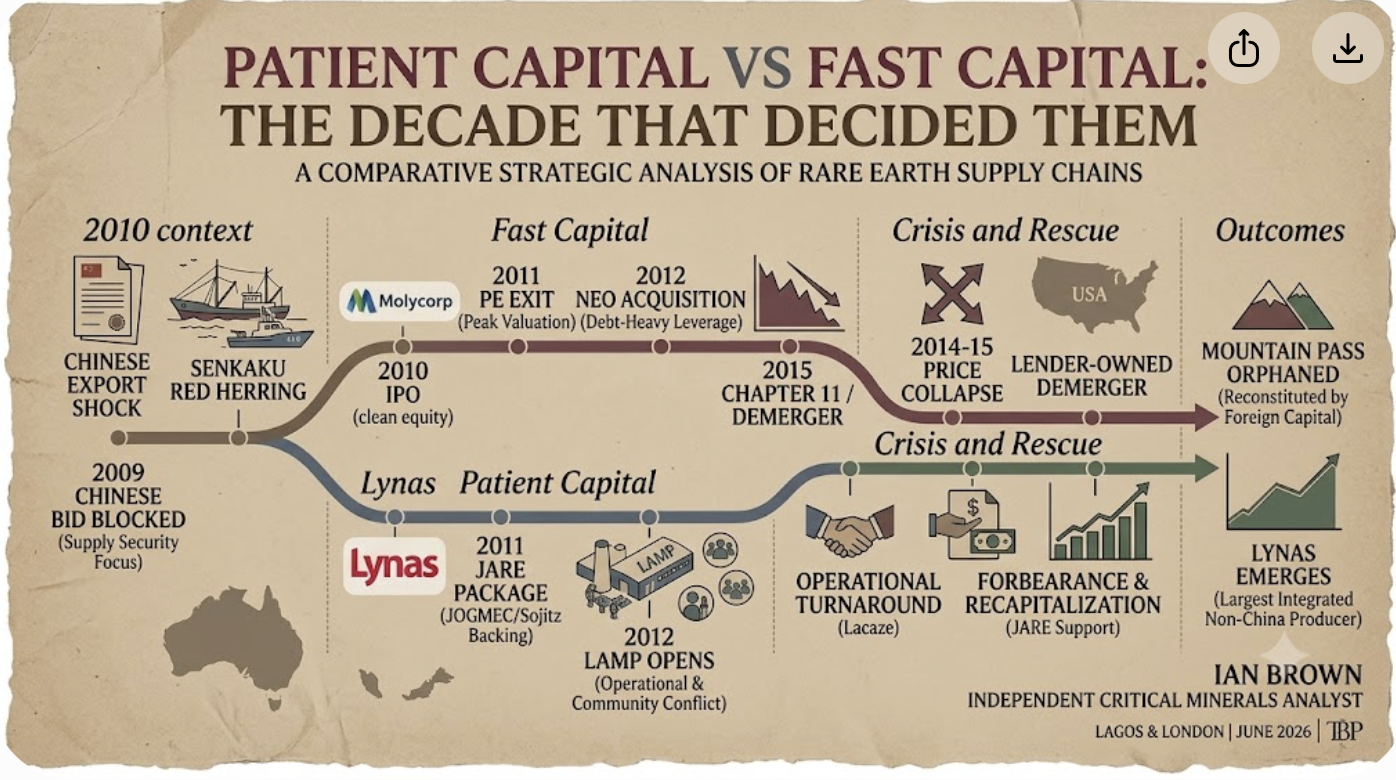

Mountain Pass and Mount Weld — the only two rare earth producers outside China operating at real scale today, and the only two that faced the identical 2010 shock and came out the other side.

One filed for bankruptcy. The other survived a worse collapse and is now the sector benchmark. The usual story blames China. The filings tell a more interesting one: a private equity windfall cashed out at the peak, a patient financing offer left to lapse, a $650 million bet placed against a WTO complaint that had already been filed — and, on the other side of the world, a lender holding the identical legal instrument who chose to extend a company's life rather than take it over.

As of today, there are only two rare earth producers outside China operating at meaningful integrated scale: MP Materials, which owns the Mountain Pass mine in California, and Lynas Rare Earths, which mines at Mount Weld in Western Australia and processes in Malaysia. Both companies trace their modern origins to the same trigger — the 2010 Chinese export shock — and both nearly didn't survive it. One did. One didn’t and had to be rebuilt from bankruptcy by the very kind of foreign capital its collapse is often blamed on.

This is the story of how two companies, facing an identical crisis in the same year, ended up as the last two standing — and why survival had almost nothing to do with the crisis itself, and everything to do with what each company did with the capital available to it, before, during, and after the shock. Nothing in what follows requires assuming any intent on anyone's part. It is an account of effects: what each capital structure did when tested, regardless of what anyone wanted or foresaw.

PART ONE: THE SHARED SHOCK

THE QUOTA CUT AND THE FISHING BOAT

In July 2010, China's Ministry of Commerce announced a 40% cut to global rare earth export quotas — a general, worldwide policy, not one aimed at any single country. Two months later, on September 7, 2010, a Chinese trawler — the Minjinyu 5179 — collided with two Japan Coast Guard vessels near the disputed Senkaku/Diaoyu Islands after ignoring orders to leave the area. Japan arrested the captain and held him under domestic law, a departure from its usual practice of simply expelling Chinese boats. China escalated diplomatically — summoning Japan's ambassador six times, suspending high-level exchanges, detaining four Japanese nationals — and, starting around September 21, rare earth exports to Japan slowed sharply for roughly two months.

Whether the export slowdown was a deliberate, targeted act of retaliation for the boat incident, or simply Japan being caught in an already-planned global quota cut that Chinese customs agents may have enforced with extra zeal during a live diplomatic row, is genuinely disputed rather than settled. Chinese industry publications show the Ministry of Commerce's quota decision predates the collision by two months, and Japanese officials and businesses were reportedly already aware of the planned global cut by mid-August 2010 — before the collision occurred. Analysis of Japanese customs data has also found no uniform, Japan-specific drop in imports consistent with a targeted embargo, as distinct from Japan being swept up in a worldwide reduction.

The point holds on the Japanese side as well as the Chinese one. Sojitz's talks with Lynas did not begin because of the Minjinyu 5179 — the two companies had already been in discussions before the collision, and signed a formal Strategic Alliance Agreement on November 24, 2010, two and a half months after the incident and building on contact that predated it. Japan's broader diversification push tells the same story: Japanese trading houses were already investing in non-Chinese rare earth sources — Sumitomo and Toshiba in Kazakhstan, Marubeni in South Africa, Sojitz and Toyota Tsusho in Vietnam — before the boat incident occurred, part of a "China risk" strategy already underway. The JARE package that would rescue Lynas in March 2011 was the acceleration of a diversification strategy already in motion, not a reaction invented over a single afternoon near the Senkakus.

This matters because the boat incident is, by a wide margin, the single most-cited piece of evidence for the claim that China "weaponized" rare earths against the West — invoked in the Wall Street Journal, the New York Times, and countless policy papers since. The more careful evidence suggests the causal story is at minimum overstated, and quite possibly backwards on both sides: a Chinese policy already in motion, and a Japanese response already under construction, both layered under a genuine but separate diplomatic crisis that intensified their visible effects at the margins without necessarily being their cause. The fishing boat incident, on this reading, appears to be a red herri

THE WTO COMPLAINT AND ITS OUTCOME

In March 2012, the United States, the European Union, and Japan jointly filed a complaint with the WTO's Dispute Settlement Body, arguing that China's export quotas on rare earths, tungsten, and molybdenum violated its trade obligations. China defended the restrictions as resource conservation and environmental protection measures. In 2014, the WTO ruled against China. China dropped the quota system entirely in 2015.

The complaint targeted the general export-restriction regime, not the 2010 Senkaku episode specifically — a useful distinction, since a great deal of popular writing conflates two separate claims: that China's rare earth policy violated international trade law (true, and formally adjudicated) and that the policy was a deliberate act of geopolitical coercion tied to a single incident (contested, and not what the WTO was ever asked to rule on). The West has a real, legally established grievance against China's export-restriction regime of that era. It is a narrower grievance than the one most retelling assumes.

The two companies at the center of this account made their defining capital decisions inside this five-year window — Molycorp's Neo acquisition financing in May 2012, two months after the WTO complaint was filed; Lynas's JARE package in March 2011, before it. What follows is the story of both.

PART TWO: MOLYCORP

I. THE 2008 BUYOUT: CORRECTLY SPOTTING THE ASSET

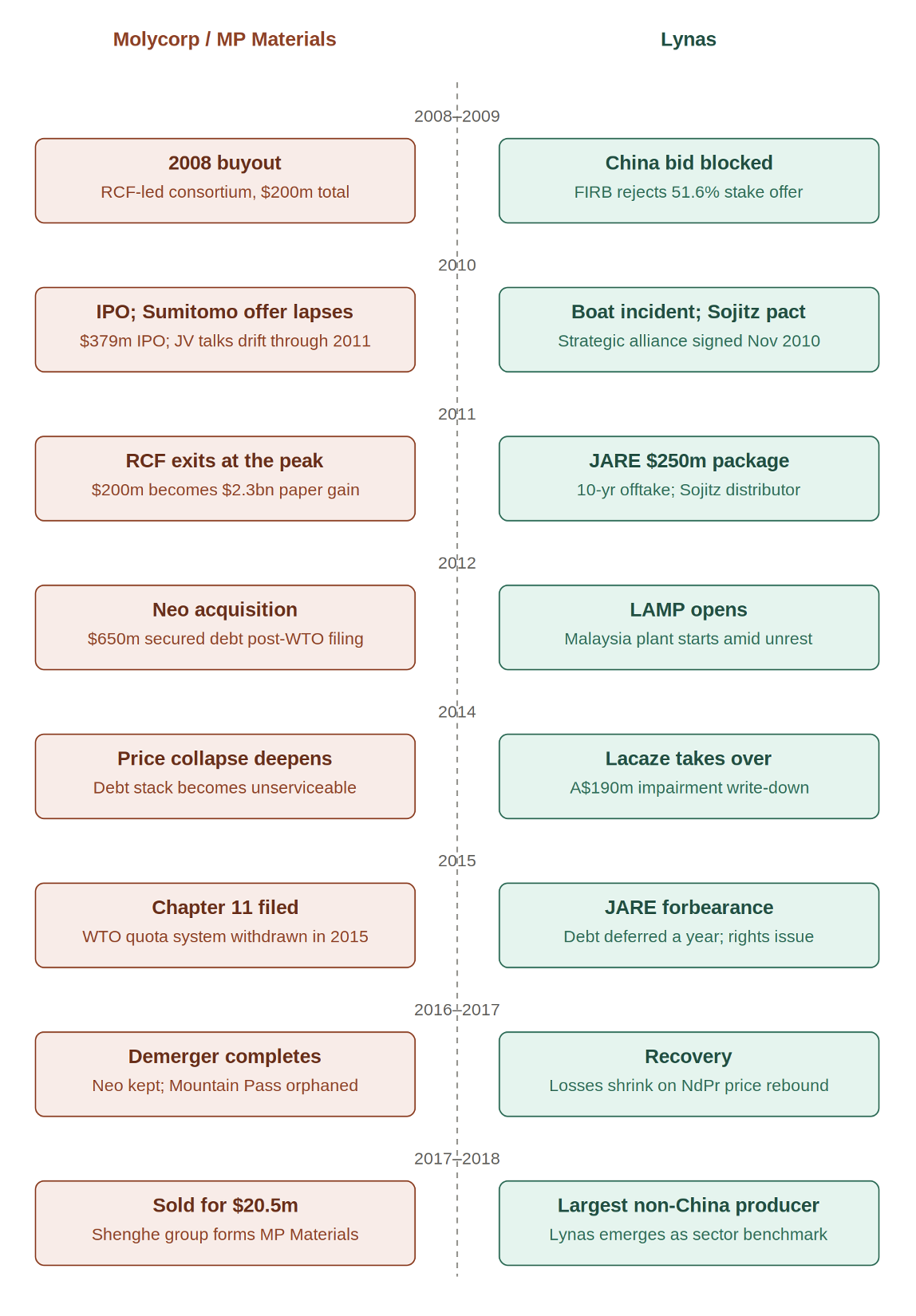

Mountain Pass did not begin its modern life as Molycorp — it began as a distressed, forgotten unit of Chevron. In September 2008, in the depths of the global financial crisis, a private consortium — Resource Capital Funds (RCF), led by mining investor Ross Bhappu; Pegasus Capital Advisors; The Goldman Sachs Group; Traxys North America; and Carint Group — bought the mine and the Molycorp name for $82 million, after an 18-month negotiation with Chevron, and contributed a further $110 million in development capital. Total investment: roughly $200 million.

The connection came through Traxys CEO Mark Kristoff, whose father had been a Molycorp marketing executive decades earlier. Bhappu's own diligence was straightforward and, in hindsight, prescient: he went directly to rare earth customers and asked about their China exposure and was told they were "100% dependent on the Chinese" and feared supply being cut off within years. This was a correct, well-researched read of a genuine strategic vulnerability, made while the asset was cheap and unfashionable.

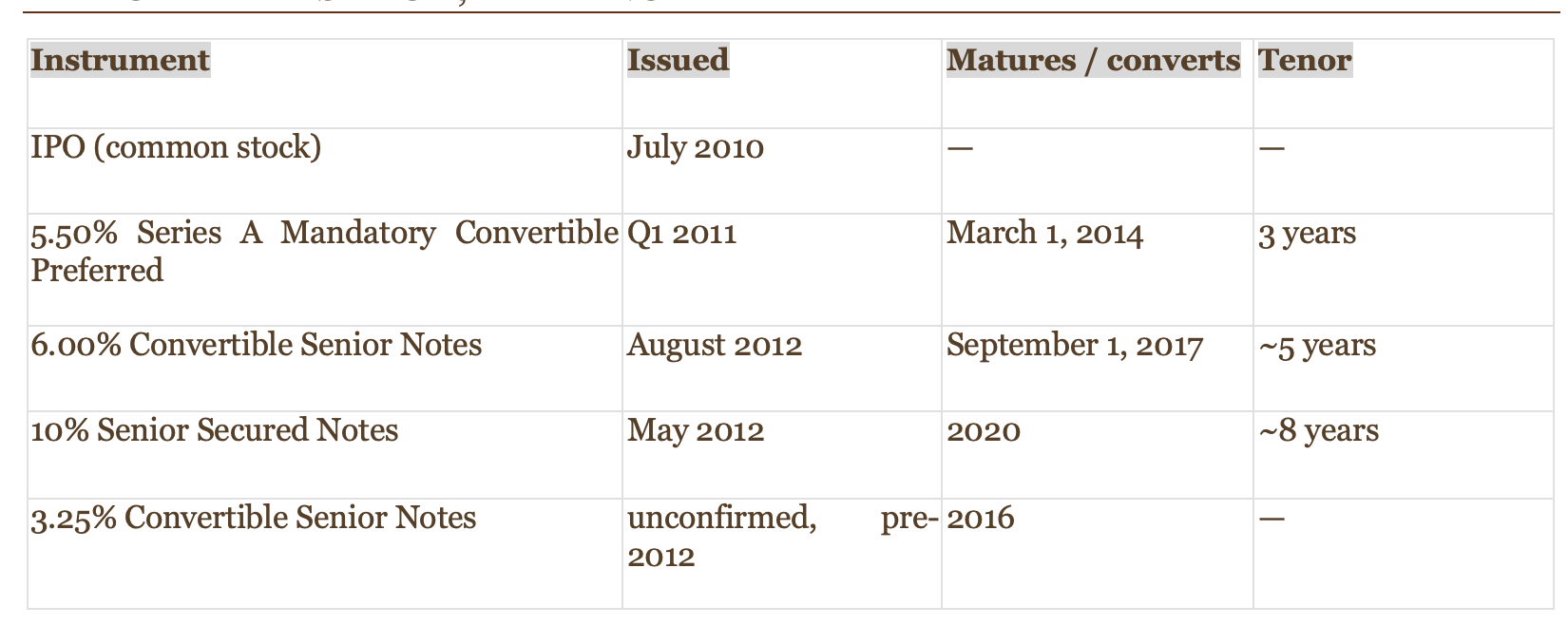

The trade paid off explosively. When Molycorp went public in July 2010 at $14 a share, RCF's 34% stake alone was worth roughly $880 million. By February 2011, with the stock above $74, the consortium's original $200 million had become paper profits of approximately $2.3 billion — one of the fastest windfalls in private equity history. The consortium began selling into that peak the same month, well before Phase 2 of Mountain Pass's expansion was even complete.

This matters for what follows because it establishes, clearly, that the failure to come was not a failure of insight. The 2008 buyers identified a genuine strategic asset, priced correctly by nobody else at the time, for exactly the reason later invoked to justify a decade of policy attention: American dependence on a single, contestable foreign supplier. What the 2008 consortium did not do — because it was never their job to do it — was stay in long enough, or structure their exit responsibly enough, to see that thesis through to a durable outcome. Their mandate was to return capital to their own investors, and by early 2011 they had already substantially done so.

II. THE PRE-NEO POSITION: A SURVIVABLE BET

Molycorp went public in July 2010, raising $378.6 million in a clean equity offering at $14 per share — no debt attached. What followed in the final months of that year is a more revealing story than it first appears, and it requires one piece of geology first. Any given rare earth ore body produces a fixed, naturally-determined mix of elements that has little to do with what the market wants — the industry calls this the balance problem. At Mountain Pass specifically, lanthanum and cerium make up more than 80% of the ore's total rare earth content, while neodymium and praseodymium — the scarce, magnet-grade elements everyone was racing to secure — make up only about 16%, yet account for roughly 80% of the ore's value. Lanthanum and cerium are so structurally oversupplied industry-wide that producers routinely must find a home for them almost as a disposal problem, separate from whatever strategic story is being told about the valuable fraction.

Molycorp's two late-2010 agreements split cleanly along this line and were complementary rather than competing. In November 2010, Molycorp signed a straightforward commercial supply agreement with US catalyst manufacturer W.R. Grace & Co. for lanthanum and cerium through 2015 — a resumption, in substance, of a decades-old relationship, since rare earths from Mountain Pass had been supplying the fluid catalytic cracking industry since the 1970s under the mine's earlier ownership. This was a simple, no-financing customer relationship for the abundant fraction of the ore. Then, at or around the same September–November 2010 window as China's export disruption to Japan — though the earliest document that can be confirmed is a memorandum of understanding signed December 10, 2010 — Molycorp was separately offered something structurally different for the scarce, valuable fraction: Sumitomo Corporation agreed to assemble a $130 million financing package — $100 million to purchase Molycorp common stock, plus $30 million in low-interest debt — in exchange for a seven-year supply commitment of NdPr oxide, the neodymium-praseodymium mix, alongside continuing cerium and lanthanum volumes. Sumitomo was seeking backing from a Japanese government entity for the deal, giving it substantially the same architecture as the JOGMEC/Sojitz package that would rescue Lynas four months later: patient, state-adjacent capital tied to guaranteed long-term offtake of the material that mattered strategically.

The Sumitomo relationship did not end quickly or cleanly. The deal, originally planned to close in February 2011, instead dragged for most of the year: Sumitomo had to split the $100 million equity commitment into two $50 million tranches and sought discounted pricing to help lock in its own downstream Japanese customers, and as late as June 2011 was still publicly saying it would close only "once it has secured Japanese customers." The deal was finally, mutually terminated around September 2011 — not a quick decision made in the flush aftermath of the IPO, but the slow expiry of a relationship over most of a year, ended once Molycorp judged the capital no longer necessary. A parallel December 2010 letter of intent with Hitachi Metals to jointly build a US NdFeB magnet manufacturing plant collapsed on a similar timeline, the parties unable to agree on the joint venture's valuation.

There is a direct contradiction buried in this sequence, worth stating plainly. Bhappu's 2008 diligence — the entire premise on which the RCF-led consortium had justified its investment — was built on going to rare earth customers and hearing that they were "100% dependent on the Chinese" and afraid of losing access within years. Sumitomo's 2010 approach was a Japanese customer showing up to solve precisely that fear, with patient capital attached, on a seven-year horizon. Letting that relationship lapse in 2011 did not just forgo a source of financing — it walked away from curing the exact vulnerability that had made Mountain Pass worth $200 million to RCF in the first place. The company that had been bought specifically because customers were desperate for a non-Chinese alternative let the customer offering to formalize that alternative wait a year and then leave.

The two ends of this fork are visible in the record, and both are covered in full below: Lynas took the equivalent Japanese offer and remained independent. Molycorp let its own lapse, and its founding asset later ended up partly under Chinese ownership. The choice made in this single, largely forgotten thread tracks the entire later divergence.

This was not a debt-free position — the Q1 2011 Series A Mandatory Convertible Preferred ($199.6 million) and the 3.25% Convertible Senior Notes due 2016 were both already outstanding — but it was a materially lighter, more liquid capital structure than what followed, built substantially from public equity markets rather than the patient, relationship-based capital that had been offered and allowed to lapse. Had Molycorp continued this base alone, a share-price collapse when rare earth prices corrected would have been likely — but not an existential threat. Equity holders can absorb a severe drawdown, and the company still exists the next day; secured creditors with a covenant breach or missed payment can end it. Mountain Pass standalone had the first kind of risk, not the second — and it had already been offered, and had let expire, exactly the kind of capital, for exactly the material that mattered, that would later prove the difference between survival and collapse at the company that accepted it.

III. THE NEO ACQUISITION: CONVERTING A SURVIVABLE RISK INTO AN EXISTENTIAL ONE

In March 2012, Molycorp announced a $1.3 billion acquisition of Neo Material Technologies — a Toronto-based rare earth processor with mine-to-magnets ambitions. The deal closed on June 11, 2012, approved by 99.9% of Neo shareholders, funded by a combination of cash, stock, and new debt: $650 million of 10% Senior Secured Notes due 2020, issued May 25, 2012, plus roughly $230 million of assumed Neo debentures and a concurrent $150 million of 6.00% Convertible Senior Notes due 2017 issued that August.

Critically, the secured notes were not a ring-fenced, non-recourse structure limited to a single asset. They were secured by a lien on Mountain Pass and guaranteed by "certain subsidiaries" of Molycorp — a guarantor pool that, once Neo closed, came to include Neo's own operating subsidiaries. The debt raised to acquire Neo was thus cross-collateralized against the whole combined enterprise, meaning a failure driven by Mountain Pass's price-dependent economics could — and eventually did — drag the more durable, diversified Neo processing and magnetics business into the same bankruptcy.

Four separate obligations — 2014, 2016, 2017, and 2020 — sat within a tight few years of each other, all priced on the assumption that 2011-level rare earth prices, or something close to them, would persist long enough to service them.

THE CAPITAL STACK, BY TENOR

IV. THE WTO TIMING

Molycorp priced its $650 million secured notes two months after the WTO complaint described in Part One was filed, and closed the Neo acquisition three months after. In 2014, the WTO ruled against China. In 2015, China withdrew the quota system — and Molycorp filed for Chapter 11 bankruptcy in the same year.

V. WHY THIS IS NOT SIMPLY HINDSIGHT BIAS

A caveat is due before proceeding. This account is built entirely from publicly available documentation — SEC filings, prospectuses, press releases, and contemporary reporting. The internal discussions, legal advice, and risk assessments that actually informed Molycorp's and its underwriters' decision to proceed with the raise are not known to this writer, and may have included considerations not reflected in the public record. What follows is a reconstruction from outside the room, not an account of what was discussed inside it.

With that said, the retrospective critique here does not rest on claiming the WTO outcome was obvious or highly probable in May 2012 — dispute settlement processes routinely take years and often fail. It rests on asymmetry. The two outcomes available to Molycorp's creditors were not symmetric: if the complaint failed, the pricing environment underpinning revenue forecasts stayed intact, preserving a status quo that was already priced in. If it succeeded — which is exactly what the complainants had set out to achieve — the mechanism sustaining elevated prices disappeared permanently, with no plausible path back. A capital structure exposed to a binary, irreversible downside arguably warranted more caution than one built on the assumption that 2011-level prices were the new baseline, regardless of the probability assigned to that downside at the time.

Put plainly: the WTO complainants did not need to be likely to succeed for the risk to be relevant — they needed only to be plausible, because the direction of their intent was never in question. The US, EU, and Japan were not filing a complaint hoping for an ambiguous outcome; the entire point of the action was to remove the scarcity premium. Molycorp's 2012 financing decision bet against the explicitly stated aim of a live legal process brought by three of the world's major economic powers.

VI. WHO BORE THE RISK

The parties who structured and approved the 2012 leverage were largely insulated from its ultimate failure. Underwriters — Morgan Stanley, Credit Suisse, J.P. Morgan — earned fees on each raise regardless of outcome. Secured noteholders, including QVT Financial and JHL Capital Group, converted their claims into majority ownership of the reorganized mine and, alongside Shenghe, ultimately profited from it. Holders of the mandatory convertible preferred stock — a security whose buyer base plausibly included convertible arbitrage funds hedging their equity exposure — likely captured the 5.5% cumulative yield largely indifferent to the underlying business outcome.

Common shareholders — including everyone who bought at the 2010 IPO, in the 2012–2013 follow-on offerings, or whose mandatory preferred converted to common stock in March 2014 — had no seniority, no collateral claim, and no seat at the table when the leverage decision was made. Molycorp's stock fell from an all-time high of $79.16 in May 2011 to $0.35 at the point of bankruptcy: a loss of more than 99.5%. This is the class of stakeholder that bore nearly the entire downside of a decision made by others.

VII. THE DEMERGER: ONE COLLATERAL POOL, TWO OUTCOMES

A note on method before this closing section: what follows is a description of effect, not intent. No claim is made here about what any party wanted or foresaw. The point is narrower and does not depend on anyone's state of mind: a particular capital structure, once distressed, sorts itself into predictable outcomes — and that is what happened.

Molycorp elected a contractual 30-day grace period on a $32.5 million interest payment due June 1, 2015, rather than default outright — its own right under the note indenture, not a creditor-initiated action. It used that window to negotiate a restructuring support agreement covering more than 70% of secured noteholders, then filed a voluntary Chapter 11 petition on June 25, 2015, with that agreement already in place.

The $650 million secured notes had been collateralized broadly across the combined enterprise — Mountain Pass plus the Neo subsidiaries pulled into the guarantor pool after the 2012 acquisition — giving the secured noteholders a claim on the whole business, not on either asset specifically. When that debt converted into a majority equity stake in the reorganized company, the entity that emerged from bankruptcy on August 31, 2016 — Neo Performance Materials, purchased by Oaktree Capital Management, the largest creditor — kept the internationally diversified processing and magnetics business built around the 2012 Neo acquisition. Mountain Pass, the asset actually named in the collateral and the one whose price collapse had caused the crisis, was carved out into a separate legal shell, Molycorp Minerals LLC, and put through its own, separate bankruptcy.

That second bankruptcy found no buyer at a March 2017 auction with a $40 million opening bid. Mountain Pass was mothballed from August 2015, at the insistence of Oaktree as a condition of its debtor-in-possession financing, and eventually sold for roughly $20.5 million in July 2017 to a consortium of JHL Capital Group, QVT Financial, and Shenghe Resources — becoming MP Materials, resuming operations in January 2018.

This is the standard mechanical shape of a loan-to-own restructuring: broad collateral plus a debt-for-equity conversion naturally separates a distressed combined enterprise into a keep pile and a discard pile, with the senior creditor class retaining the former. It requires no one to have planned it. It only requires the collateral structure to have been written the way it was written, and the discard pile, in this case, happened to be the company's own founding asset — the one the entire enterprise had originally been built to develop.

Nor did Neo's side of the split deliver the clean escape from Chinese dependency the surviving story is often assumed to represent. Neo Performance Materials continued to operate a heavy rare earth separator inside China after the demerger, and by 2023 derived roughly 30% of revenue and housed over 45% of its workforce there — including its only rare earth bonded magnet manufacturing facilities. It also depended on Russian feedstock for its Estonian operations. This was not a static position left unaddressed for a decade: Neo spent the years between the 2016 demerger and 2024 continuously managing shifting Chinese regulatory requirements and joint-venture structures, including a 2023 decision to relocate its NAMCO catalyst manufacturing operation to an upgraded industrial park in Zibo. What changed only in 2024 was the decision to begin actually divesting Chinese processing assets outright — in a transaction connected to the same Shenghe-linked capital that had by then already rebuilt Mountain Pass — rather than continuing to manage and invest in the China-based operations as an ongoing part of the business. Neither half of the demerged company emerged in 2016 as a non-China alternative. One was orphaned and had to be reconstituted by foreign capital; the other survived by remaining substantially embedded in, and actively managing rather than exiting, the dependency the original 2012 acquisition was supposed to help escape.

VIII. CLOSING: MOLYCORP

Molycorp's collapse is often told as a story of Chinese aggression — a scrappy Western challenger crushed by a hostile foreign monopoly. The record does not support that reading, and it does not need to, because a fuller and more precise account is available without it. China's 2010 export quota cut created the price environment that made Molycorp's rise possible. A private consortium correctly identified Mountain Pass as an undervalued strategic asset in 2008 and was proven right within thirty months, converting $200 million into $2.3 billion in paper gains — and largely exited at the top, its mandate to return capital to its own investors fulfilled. The management and underwriters who took over from there priced $650 million of secured debt in May 2012, two months after the United States, the European Union, and Japan had already filed a formal WTO complaint with the explicit, stated aim of eliminating the very scarcity premium the debt depended on. When the WTO ruled against China in 2014 and the quota system was withdrawn in 2015, the complainants got exactly the outcome they had set out to achieve — and Molycorp, whose capital structure had been built on the opposite assumption, ran out of cash in that same year.

What followed was not asset-stripping in the sense of anyone setting out to strip anything. It was the ordinary, foreseeable mechanics of a broadly collateralized capital structure sorting itself, under distress, into a valuable half that a senior creditor class retained, and a distressed half — the company's own founding asset — that was carved off and sold separately at a steep discount. A standalone Mountain Pass, financed by equity alone, would likely have absorbed the underlying price collapse the way Lynas did: a brutal drawdown, but a company that continued to exist. It is a further irony that Molycorp had already been offered, for over a year, exactly the kind of patient, government-adjacent capital that made that survival possible for Lynas — Sumitomo's 2010 financing package for the NdPr fraction of its production, structured with Japanese state backing against a seven-year offtake commitment — and had let it lapse through 2011, choosing instead the faster, more liquid capital of the public equity markets. What converted a survivable cyclical risk into an existential one, and then into a demerger that separated the enterprise along exactly the lines its own collateral had drawn, was the decision to lever the combined business so heavily to acquire Neo — at peak valuations, against a price mechanism already under formal legal challenge, in a structure that left nearly all of the eventual loss on common shareholders who had no part in making the decision.

Nobody needed to design this outcome. The capital structure did it on its own.

PART THREE: LYNAS

I. ORIGINS: A PUBLIC COMPANY FROM THE START

Lynas began in 1983 as a small Western Australian gold explorer listed on the ASX. In 2000, then-CEO Les Emery identified an opportunity in the Mount Weld rare earth deposit, which Ashton Mining was looking to offload; Lynas acquired it and renamed itself Lynas Corporation Limited in 2001. Nicholas Curtis took over as CEO the same year and ran the company through a feasibility study (completed March 2005, ~A$1 billion estimated capex) and into first production at Mount Weld in 2007.

Unlike Molycorp, which spent 2008–2010 as a private LLC before its IPO, Lynas had been raising capital in public equity markets continuously since 1983 — nearly three decades of public-company governance, disclosure, and shareholder scrutiny by the time the 2010 shock arrived.

II. THE BLOCKED CHINESE BID, 2009

In May 2009, China Non-Ferrous Metal Mining (Group) Co., a Chinese state-owned enterprise, offered Lynas $252 million in exchange for a 51.6% controlling stake. Australia's Foreign Investment Review Board scrapped the deal, explicitly on the grounds that it could threaten rare earth supply to non-Chinese buyers. Lynas raised $450 million through an Australian share sale instead.

This is worth stating plainly because it complicates any account in which no Western institution ever screened for this kind of exposure: a full year before the Senkaku boat incident, an Australian regulator did exactly that, and did it successfully.

III. THE 2011 JARE PACKAGE

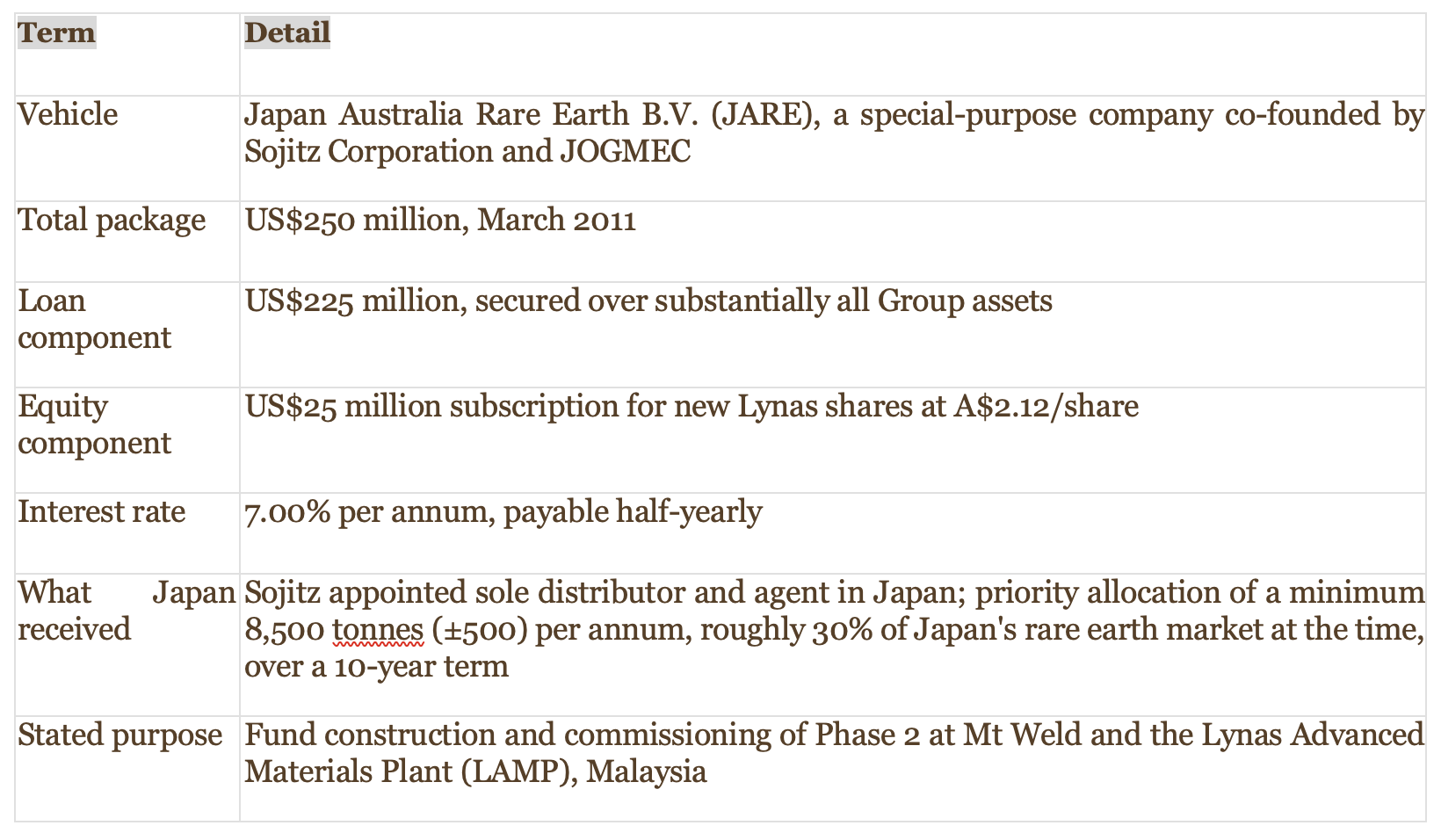

In November 2010, Sojitz and Lynas signed a Strategic Alliance Agreement — the forerunner to a binding package finalized on March 30, 2011, structured through a purpose-built vehicle, Japan Australia Rare Earth B.V. (JARE), co-founded by Sojitz and JOGMEC with support from Japan's Ministry of Economy, Trade and Industry.

The structural point worth isolating: Japan's exposure was to volume, not price. The offtake was denominated in tonnes per year over a ten-year term, not indexed to a price forecast. When rare earth prices later collapsed, JARE's return depended on Lynas continuing to produce and ship material — not on 2011-level pricing persisting. This is the structural feature that separates it from Molycorp's price-dependent secured debt.

FIGURE 2: LYNAS CAPITAL STRUCTURE

IV. THE CRISIS

Lynas's collapse was, in percentage terms, worse than Molycorp's. Market capitalization fell from roughly A$3 billion in 2011 to roughly A$3 million in 2015 — shares trading at 2.3 Australian cents, a decline of more than 99.9%, compared with Molycorp's 99.5% fall from $79.16 to $0.35.

Three pressures compounded simultaneously. First, the same 2011–2015 rare earth price collapse that sank Molycorp: the NdPr/heavy oxide price fell from roughly US$41.4/kg in July 2014 to US$37.3/kg in June 2015, continuing a multi-year decline from the 2011 peak. Second, the Lynas Advanced Materials Plant (LAMP) in Kuantan, Malaysia — an $800 million facility — faced sustained community opposition and regulatory uncertainty over radioactive waste disposal, dating to 2008 organizing and intensifying through a March 2011 New York Times story and litigation that ran into December 2012. Third, the Group recorded a A$190 million impairment writing down LAMP Phase 1 assets to fair value in the year to June 2014 — net assets fell from A$628.7 million to A$302.0 million in that single year, a decline of A$326.7 million.

Amanda Lacaze took over as CEO in June 2014, inheriting a company by every account fighting for survival.

V. THE RESCUE

The recapitalization was a coordinated package, not a single instrument. Four elements moved together:

1. Operational cost-cutting. Lacaze relocated herself and most remaining staff to Malaysia, closing the Sydney head office and consolidating Sydney/Kuala Lumpur functions — $16 million in annualized savings — alongside a separate $10 million in procurement renegotiation savings. Later reporting put total cost reductions above A$40 million per annum, well in excess of original targets.

2. A genuine rights issue. A 5-for-14 renounceable entitlement offer in September–October 2014 raised approximately A$71 million, alongside a A$12 million institutional placement — roughly A$83 million total, at A$0.08/share, fully underwritten by Patersons Securities. Unlike Molycorp's opportunistic follow-on offerings, this was a genuine pro-rata rights issue, asking existing shareholders to re-underwrite the business alongside new institutional capital.

3. An amended senior debt amortization schedule. Coordinated with the equity raise, the repayment timetable on the JARE facility (then US$215 million outstanding, at 7.00% per annum) was restructured — in Lacaze's words, to "align our debt repayment schedule more closely with the planned growth in profitability."

4. Forbearance at the point of maximum stress. Under a binding term sheet dated March 12, 2015, JARE agreed to defer the principal repayments due March 31 and June 30, 2015 to June 30, 2016 — a deferral of over a year — and agreed that every interest payment due in calendar 2015 would be deposited into a restricted account, available at JARE's own discretion for reuse in the Lynas business. The same term sheet shows Lynas's separate US$225 million unsecured convertible bondholders, led by Mt Kellett Capital Management, agreeing to comparable relief on their own facility in parallel.

Lynas's own FY2015 annual report records the moment plainly: "Both of the Company's debt providers, Japan Australia Rare Earths B.V. and the Mt Kellett led bondholder group, continued to demonstrate their support for the business by extending the term of their facilities and by agreeing to other amendments to the terms of their facilities."

The recovery, once the operational and pricing environment turned, was rapid: FY2016 revenue of $139 million and a $68.5 million loss became FY2017 revenue of $194 million and an $11.2 million loss, as NdPr prices rose from roughly $40/kg in September 2016 to over $90/kg within about a year, and September-quarter 2017 sales reached $88 million, up 108% year-on-year.

VI. FORBEARANCE VERSUS CONVERSION

JARE held the same kind of instrument Molycorp's secured noteholders held senior debt, secured over substantially all of the company's assets, with full legal power to enforce, accelerate, or convert into ownership on default. A purely return-maximizing holder of that position, facing a company that had just lost more than half its net asset value in a year, would ordinarily be assessing recovery value and positioning to take control — which is exactly what Molycorp's noteholders (QVT Financial, JHL Capital Group, JMB Capital Partners) did in 2015, converting their claim into a majority equity stake in the reorganized company.

JARE did the opposite. It deferred principal by more than a year and let contractual interest sit uncollected, at its own discretion, for reinvestment in the business it was owed money by. The difference is legible in the mandate behind the capital, not in the legal instrument itself, which was structurally similar in both cases. JOGMEC exists to secure Japanese industrial supply of rare earths, not to generate an investment return; for JARE, a Lynas that survived and kept producing in 2020 was worth more than a maximized recovery in 2015. Molycorp's noteholders were distressed-debt and arbitrage funds whose mandate was return-maximization, and default gave them the tool — conversion to equity — that best served that mandate.

One qualification is worth adding: JARE's forbearance was not purely a unilateral act of institutional patience. Its senior position sat alongside Lynas's separate US$225 million unsecured convertible bondholder group, led by Mt Kellett Capital Management, and the March 2015 relief was negotiated as a coordinated package between both creditor classes rather than by JARE acting alone. Inter-creditor dynamics of this kind typically mean each side's willingness to grant relief is at least partly conditioned on the other doing the same — a senior lender forcing default when a subordinated class is simultaneously being asked to extend can create its own complications. JARE's mandate likely explains why it was willing to be the anchor of that coordinated forbearance; the existence of the inter-creditor agreement likely explains part of why the relief took the specific, mutual shape it did.

Same instrument. Same enforcement rights. Two different mandates behind the capital, and two different outcomes for the company underneath it.

VII. CLOSING: LYNAS

Lynas's near collapse was, by the numbers, worse than Molycorp's. It faced the identical rare earth price cycle, carried real leverage, and was additionally burdened by a sustained regulatory and community fight over its Malaysian plant that Molycorp never had to contend with. It did not have a cleaner run than Molycorp — it had a different capital structure sitting behind an equally severe crisis, and specifically a lender whose institutional purpose gave it a reason to extend, not enforce, when the test came.

Lynas today is the largest producer of separated rare earth materials outside China. Mountain Pass had to die and be rebuilt under new ownership to reach a comparable position. The difference between those two outcomes was decided in a handful of specific choices — Sumitomo's declined 2010 offer, Molycorp's 2012 leverage decision, JARE's March 2015 forbearance — not in the underlying severity of the crisis both companies faced, which was, if anything, worse at Lynas.

PART FOUR: CONCLUSION

Lay the two companies’ side by side and a single thread runs under every layer: every actor who chose the shortest available time horizon eventually lost the asset; every actor who chose the longest available time horizon eventually kept it. This was true inside Molycorp alone — the 2008 buyout consortium correctly identified Mountain Pass as a generational strategic asset and still exited within thirty months, because that was what its own fund structure required. It was true again through 2011, when Molycorp held the same patient, state-backed architecture that later saved Lynas — Sumitomo's offer for the valuable NdPr fraction of its production — and let it lapse over the course of a year in favour of faster, more liquid public equity. And it was true a final time in 2012, when the company levered itself to the point of no return against a price mechanism three governments were already suing to dismantle.

Lynas was not spared this test. Its collapse was, in percentage terms, worse than Molycorp's, compounded by a regulatory fight Molycorp never had to face. What it had, at the one moment that mattered, was a lender whose reason for existing was never a return — and that lender used the leverage it held to extend the company's life rather than to convert it into ownership. Molycorp's noteholders held the identical instrument and used it for the opposite purpose, because that is what their own capital was for.

None of this required China to do anything beyond setting the table. The 2010 quota policy — whatever its true relationship to a fishing boat collision two months later — created a price environment that drew capital toward rare earths on both sides of the Pacific. What determined which companies were still standing by 2018 was not the severity of that shock, which Lynas absorbed worse than Molycorp did, but the mandate behind the money each company was standing on when the shock arrived.

The West had the same opportunities Japan had. Molycorp had, at different moments, the same opportunities Lynas had. The outcomes diverged anyway, and the reason is visible in the public record: it was decided by what each piece of capital was for.

SOURCES

PRIMARY AND REGULATORY FILINGS

Molycorp, Inc. — S-1, S-1/A, 8-K, and 10-K filings, 2010–2015, including prospectuses for the Series A Mandatory Convertible Preferred Stock, the 10% Senior Secured Notes due 2020, the 6.00% and 3.25% Convertible Senior Notes, and the Neo Materials acquisition. U.S. Securities and Exchange Commission, EDGAR (sec.gov/edgar).

MP Materials Corp. — 10-K (FY2023), Form 8-K filings on the U.S. Department of Defense partnership (2025) and the Saudi Arabia/Maaden joint venture. SEC EDGAR.

Lynas Corporation Limited — Financial Report for the year ended 30 June 2014; Interim Report for the half year ended 31 December 2014; Annual Report 2015; Renounceable Rights Issue Prospectus and Capital Raising ASX announcements, September–October 2014. lynasrareearths.com, Reporting Centre.

Japan Organization for Metals and Energy Security (JOGMEC) — news releases on the Sojitz/JOGMEC financing agreements with Lynas (2011), and subsequent JARE investments (2022, 2023). jogmec.go.jp.

Sojitz Corporation — news releases on the Lynas strategic alliance and offtake agreements (2011, 2022, 2023, 2026). sojitz.com.

NEWS AND WIRE REPORTING

Business Wire — Molycorp press releases on the Neo Materials acquisition, the Sumitomo memorandum of understanding, and related financings, 2010–2012.

Bloomberg — "Molycorp Bonds Surge as Peer Gets Equity Funding" (2014); "Qatar-Backed Mining Fund Said to Scrap Expansion Plans on Rout" and related QKR Corp. reporting (2014–2015).

Forbes — Nathan Vardi, "The Money Man Behind America's Rare Earth Minerals" (2010) and "The Rare Earths Stock Market Failure 60 Minutes Forgot" (2015); Tim Treadgold, "Down to Earth: Amanda Lacaze Turns Around Australia's Lynas Corp." (2017); Michael Kanellos, "Three Lessons From The Woeful Tale Of Molycorp" (2015).

Reuters, RTTNews, ProactiveInvestors, and CHEManager — reporting on the Molycorp–Sumitomo financing negotiations and termination, 2010–2011.

Mining.com, Mining Technology, Mining Journal, and The Northern Miner — reporting on Mountain Pass's operating history, the 2008 Resource Capital Funds-led buyout, and the 2015 shutdown.

High Country News — "The U.S.'s only rare-earth mine files for bankruptcy" and "Why rare-earth mining in the West is a bust" (2015).

InvestorNews — "From Survival to Strength: How Amanda Lacaze Transformed Lynas Rare Earths" (2025); coverage of Neo Performance Materials' European magnet plant and China operations.

POLICY, TRADE, AND ACADEMIC SOURCES

CEPR/VoxEU — "Revisiting the China–Japan Rare Earths dispute of 2010."

East Asia Forum — "Did China really ban rare earth metals exports to Japan?" (2013).

Asia Maritime Transparency Initiative (CSIS) — "Counter-Coercion Series: Senkaku Islands Trawler Collision."

World Economic Forum — "How Japan solved its rare earth minerals dependency issue" (2023).

The Diplomat — "Japan's Critical Minerals Resilience Didn't Start in 2010 – or 2026" (2026).

New Security Beat (Wilson Center) — "How to Diversify Mineral Supply Chains – A Japanese Agency has Lessons for All" (2024).

IEEE Spectrum — "The Magnet That Made the Modern World" (2023), on the invention of the NdFeB magnet by General Motors and Sumitomo Special Metals.

Binnemans, K. et al. — "Rare-Earth Economics: The Balance Problem," Journal of Sustainable Metallurgy / JOM (2013, 2018).

COMPANY AND INDUSTRY SOURCES

MP Materials Corp. — corporate history page, mpmaterials.com/history.

Neo Performance Materials — Annual Information Form (2024) and investor materials, neomaterials.com.

Rare Earth Exchanges and Rare Earth Mining — sector analysis on MP Materials, Lynas, and Neo Performance Materials competitive positioning (2026).

Preferred Stock Channel, Justia, and SEC EDGAR contract filings — terms of Molycorp's Series A Mandatory Convertible Preferred Stock and related Traxys sales/buy-back agreements.

Note: this list reflects the sources drawn on while preparing this paper. Figures and quotations have been cross-checked against primary filings where available; where only secondary reporting could be found that is noted in the text itself.

Rare Earths and the Dual-Price Market

A kilogram of neodymium and praseodymium costs $110 inside China. The same kilogram, loaded for export, costs $164. Landed in the United States, it costs $231.

That spread is not a pricing anomaly. It is the cost of dependency, and it is the subject of this paper.

Rare Earths and the Dual-Price Market traces how China's rare-earth market split in two: a domestic price reflecting its own industrial advantage, an export price reflecting everyone else's scarcity. It follows the evidence from the 2011 spike and collapse that killed Molycorp and spared Lynas, through the WTO ruling the West won and came to regret, to the export controls, arrests and cutoffs that show China has no intention of standing that architecture down.

It asks what a distressed acquisition in Tanzania and a tightening feedstock base suggest about how Beijing really sees the West, and the question every OEM sourcing NdPr has already answered, knowingly or not: what are you prepared to pay to avoid finding out the price of doing nothing?

How SMM's FOB Quote Illustrates the Cost of Western Dependency

Rare-earth pricing now matters to anyone who builds EVs, wind turbines, robots, motors, defence systems or industrial platforms, not only to metals traders. The reason is that material which cannot be delivered has no usable price at all.

A chokepoint material

Neodymium-iron-boron magnets are the strongest permanent magnets in commercial production, and their performance depends on two elements, neodymium and praseodymium, which are almost always sourced and traded together as a single alloy input known as NdPr oxide or NdPr metal. These magnets sit inside EV traction motors, wind turbine generators, robotic actuators and precision defence systems, wherever a large amount of magnetic force is required from a small, lightweight component. No substitute technology matches them at scale, which is why NdPr specifically, rather than rare earths as a broad category, is the material chokepoint for electrification.

NdPr, together with a smaller volume of heavy rare earths such as dysprosium and terbium, used to hold magnet performance at high temperatures, is what makes the wider electrification of the global economy possible. These magnets let an electric motor convert stored energy into mechanical force at an efficiency fossil-fuel drivetrains cannot match, and that efficiency gain, paired with continuing improvements in battery energy density, is the basis of the shift now under way across transport, power generation and industrial equipment. Electrification is a step change in energy conversion efficiency, and NdPr magnets are one of the two components, alongside the battery itself, that make it physically possible.

China's refining advantage

China's pricing power does not come from reserves. It comes from processing. China holds an estimated 40% of global rare-earth reserves and around 60% of mining output, but its share of separation and refining capacity, the step that turns raw ore into tradeable oxide, runs above 90%. Refining is the harder step to replicate, and that is where China's advantage sits. Whoever controls refining controls the price. China controls the refining.

A small market with outsized leverage

It is worth stating the size of this market directly. The global rare earth magnet market is worth somewhere in the region of US$15-20 billion a year, depending on which estimate you use. Global copper is worth roughly US$250-300 billion a year, so rare-earth magnets are perhaps one-fifteenth the size.

That comparison is the reason this material is worth writing about. A market smaller than most countries' agricultural exports determines whether EV motors, wind turbine generators, robotics actuators and a meaningful share of precision defence systems can be built at scale.

There is no substitute technology for what NdPr magnets do and no meaningful production base for them outside China. That mismatch between size and leverage is what asks the pricing questions in the rest of this piece worth taking seriously.

Two prices, one market

China's rare-earth market is priced in two ways: delivered-to-works, the price with material already delivered to the buyer's plant in China, and FOB (free-on-board), the price once material is loaded onto a vessel at a Chinese port, ready for export. FOB is the standard basis for international trade because it marks the point at which cost and risk pass from seller to buyer.

SMM as the benchmark

SMM, Shanghai Metals Market, is the industry-standard price-reporting agency for Chinese metals and the highest-liquidity benchmark in this sector. It is not the only price-reporting agency covering rare earths. Argus and a handful of other platforms publish periodic rare earth market insight, and Benchmark Mineral Intelligence introduced its own ex-China price assessments in mid-2025, but Benchmark's ex-China grades are published monthly.

SMM's advantage is frequency and depth: its domestic China spot prices are assessed daily, and its FOB China price points, added from late 2025 into early 2026, are updated weekly. That higher-frequency liquidity is what makes SMM's data usable for the kind of granular, near-real-time comparison this piece relies on, and it is why SMM, not a monthly assessment, is the reference point throughout.

SMM has faced criticism in some quarters for being politically influenced, given its location and proximity to the market it reports on. That criticism is largely unfair. SMM operates within the constraints of where it sits, as any price-reporting agency does, but the evidence suggests it tries to be as independent as the environment allows, and its methodology, specification details, and price-submitter process are more transparent than the criticism usually credits.

The limits of a domestic price

The more difficult problem lies one level up and is not about SMM. A domestic Chinese spot price, however, honestly reported, cannot be representative of a global market because it reflects only transactions within China. The issue is not that the quote is biased. It is that China is the market, to an extent that makes a purely domestic price look like the whole picture when it is only one side of it.

The FOB quote goes some way to addressing that by putting a number on the export side of the transaction for the first time. But going some way is not the same as solving it, and there is a real case that the industry needs an independent, high-liquidity, ex-China benchmark of its own rather than relying on a China-based quote, however well run, to stand in for a market it can only ever half describe.

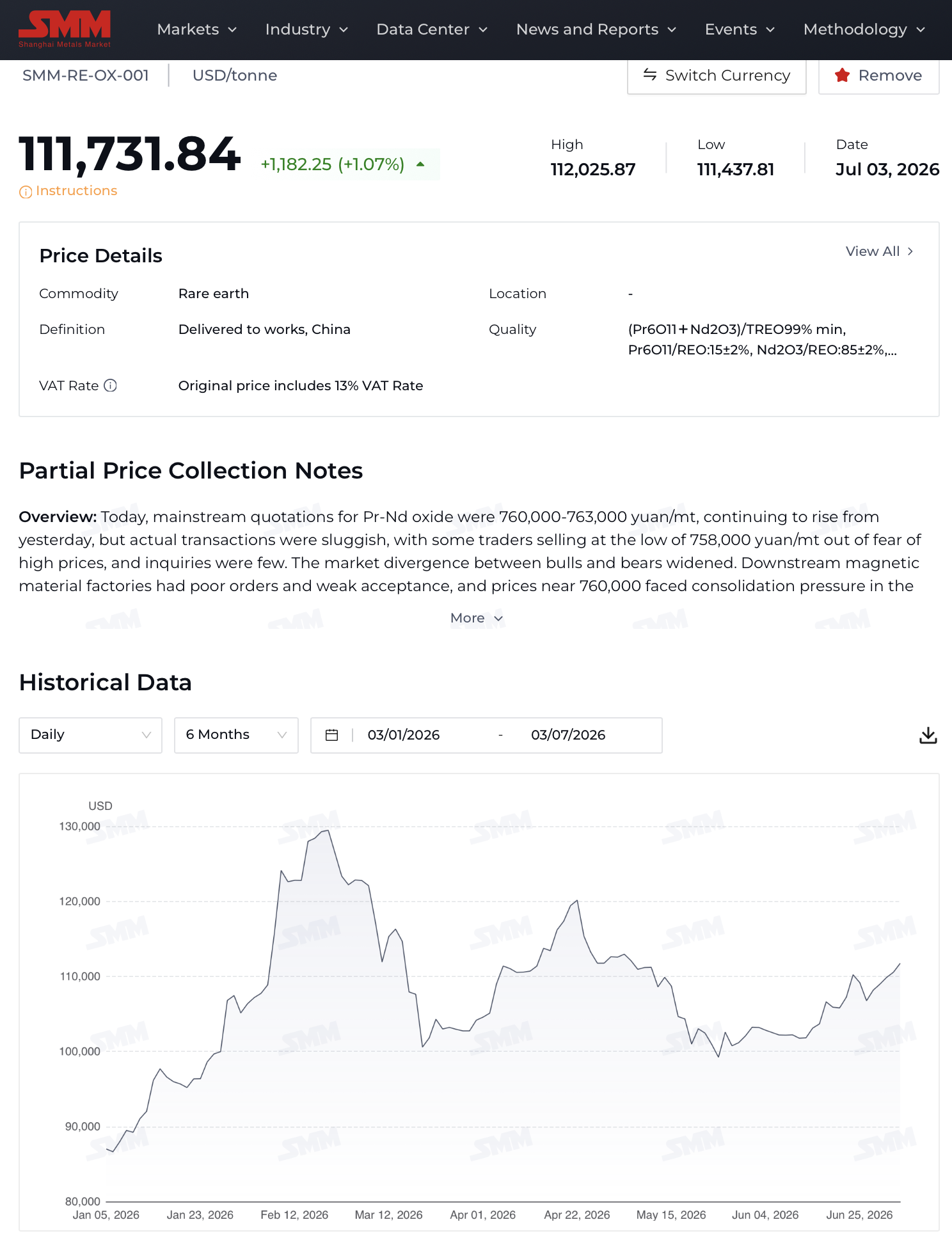

The domestic blend: SMM-RE-OX-001

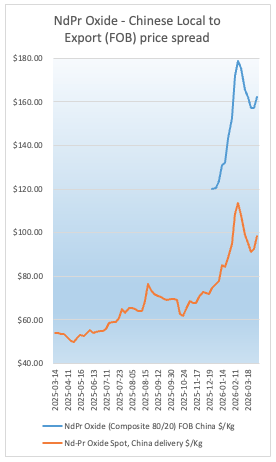

SMM publishes a dedicated Pr-Nd Oxide product, SMM-RE-OX-001, specified to GB/T 31965-2015 as Nd₂O₃/REO 85±2% and Pr₆O₁₁/REO 15±2%. As of 1 July 2026, this 85/15 internal blend traded at approximately US$109.87/kg (US$109,869.92/tonne), delivered to works inside China, VAT-inclusive, under China's standard 13% VAT. This is the cleanest internal China reference point because it is an actual traded basket rather than a synthetic blend built from standalone oxide quotes.

Adjusting for specification and VAT

Two adjustments matter before this figure can be compared to anything traded outside China. The first is specification. The 85/15 Nd/Pr ratio used domestically is not the basket the wider market usually references; most NdPr FOB and offtake pricing is quoted on a 75/25 basis. Inside China, this barely matters because standalone Nd₂O₃ and Pr₆O₁₁ are currently priced close to each other, so an 85/15 basket and a 75/25 basket built from the same internal quotes land in roughly the same place. FOB is different: neodymium carries a large premium over praseodymium there, so comparing an 85/15 domestic quote directly against a 75/25 FOB number is not like-for-like, and any resulting gap is a specification artefact rather than a market signal.

The second is VAT. The domestic 85/15 price is VAT-inclusive; the 13% is paid by the Chinese buyer and forms part of the domestic transaction price, and should not simply be stripped out to create an FOB-comparable number. Rare earths carry no export VAT rebate, so the VAT a domestic buyer pays and the VAT cost an exporter cannot recover sit on different sides of the transaction and are not interchangeable. The domestic price already includes VAT paid by the Chinese buyer, while FOB-side costs are pushed up, not down, because input VAT cannot be reclaimed against rare-earth exports as it can for rebate-eligible products. The build-out from FOB toward landed US cost reflects this second effect; it is not a reversal of the first.

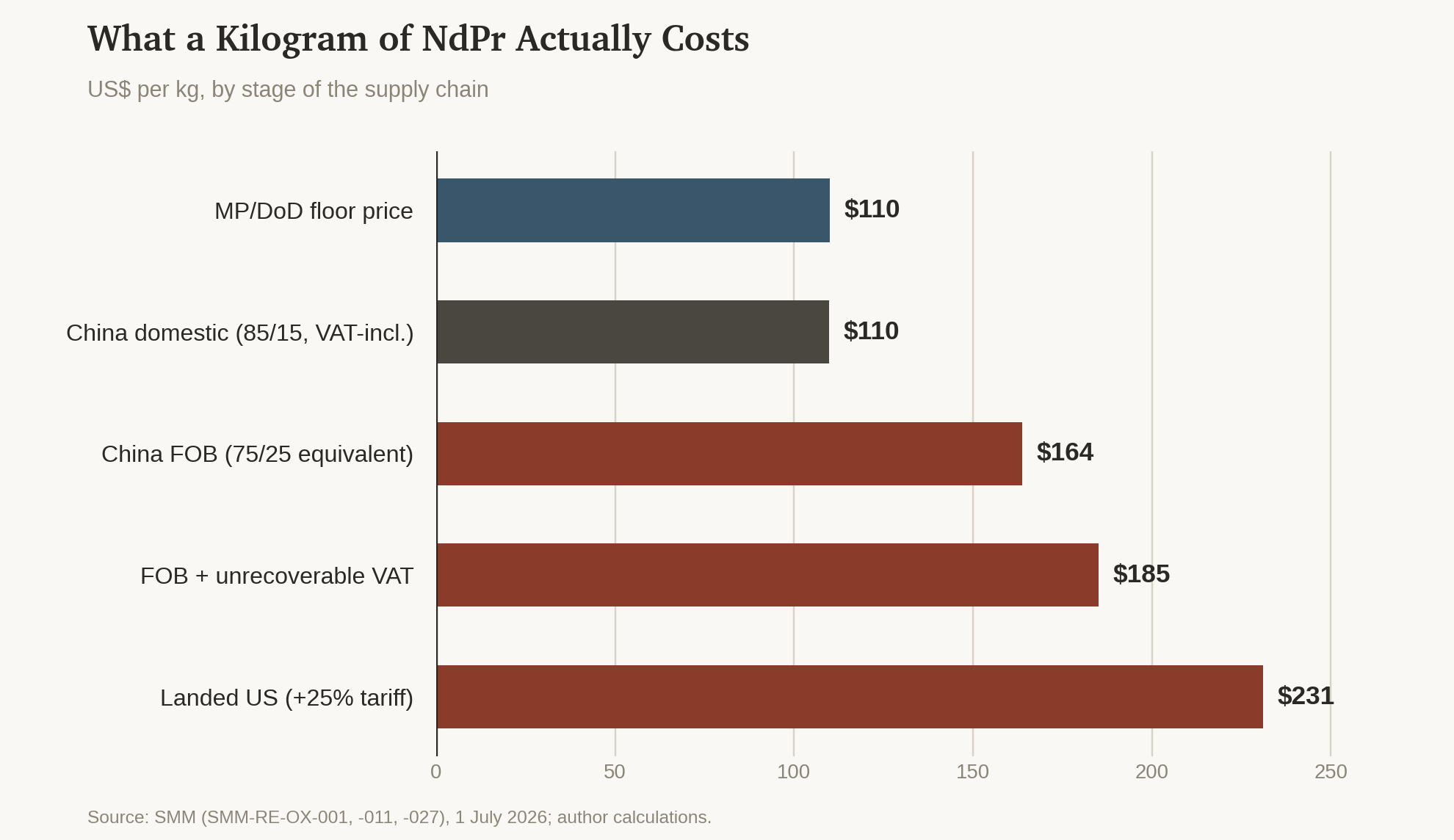

The FOB numbers

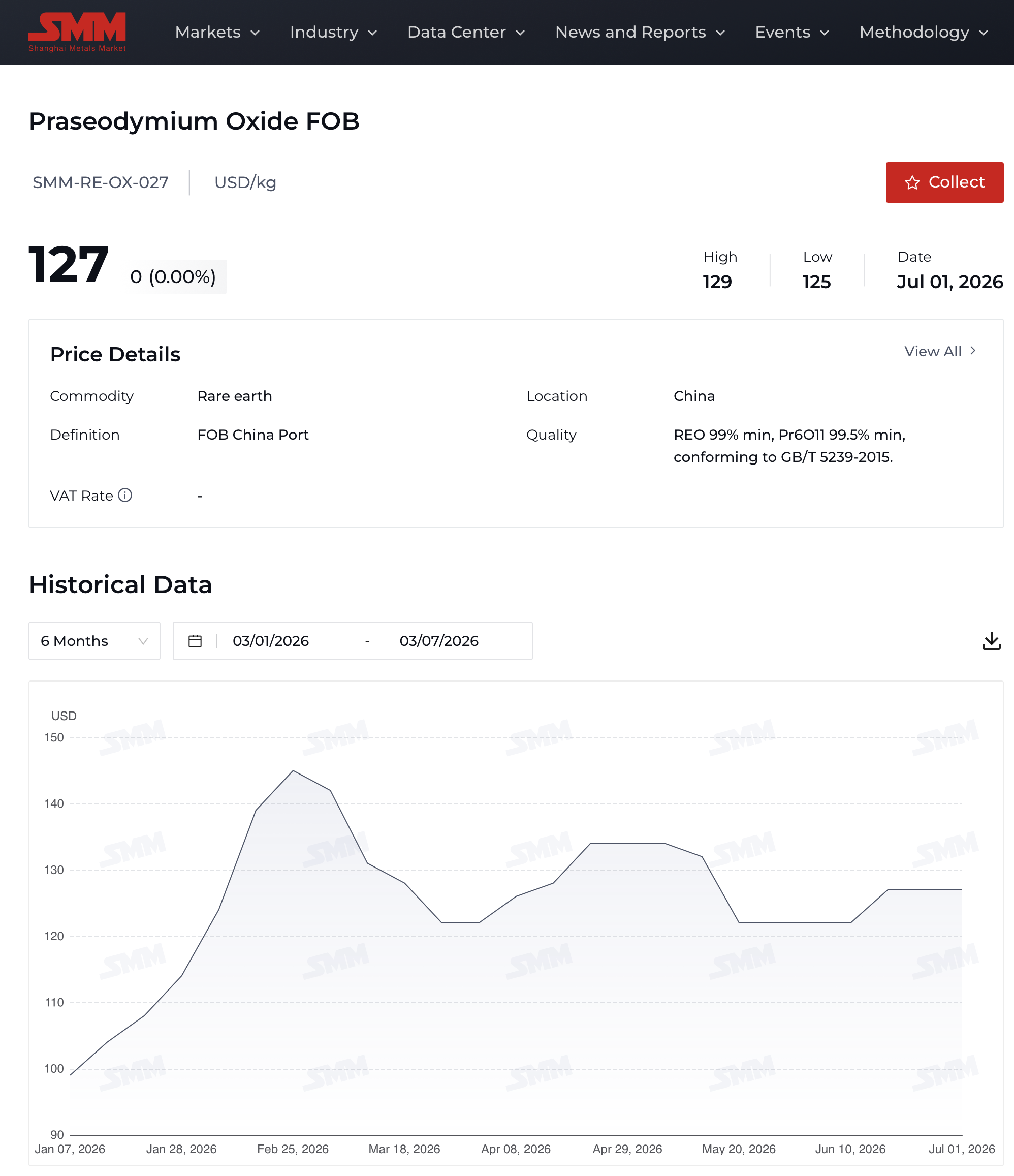

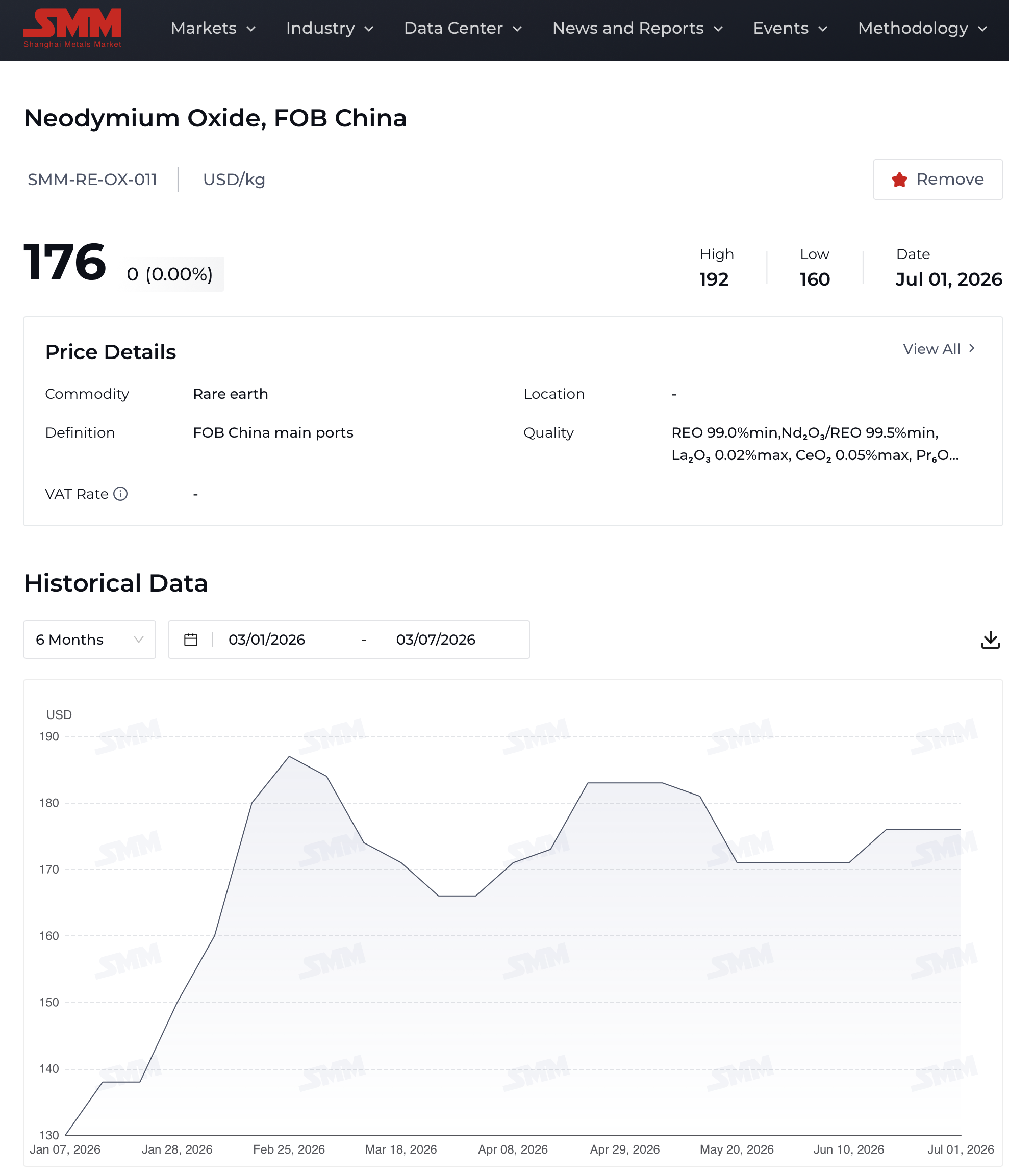

The China FOB market tells a different story. As of 1 July 2026, SMM quoted neodymium oxide (SMM-RE-OX-011, FOB China main ports) at US$176/kg and praseodymium oxide (SMM-RE-OX-027, FOB China Port) at US$127/kg. Recalculated as a 75/25 NdPr basket:

0.75 × US$176 + 0.25 × US$127 = US$132.00 + US$31.75 = US$163.75/kg

Add unrecoverable VAT exposure, and the cost basis moves toward US$185/kg. Into the United States, with a 25% tariff on top, the landed entry cost can move toward US$231/kg

That is not a typical pricing spread: roughly US$110/kg domestic against US$164/kg FOB-equivalent before VAT and tariff effects, and it shows two markets rather than one. China's internal spot reflects the price inside China's industrial system. China FOB reflects overseas demand competing for

restricted exportable supply. FOB is a real market price, but it is a price formed under restricted supply.

Feedstock under pressure

Until SMM began publishing FOB prices in earnest at the end of 2025, the only rare-earth price quotation available to the market was the Chinese domestic spot price. That price reflects what Chinese buyers are paying for spot tonnes inside China, and read on its own, over a long enough run, it is a reasonable proxy for China approaching the limits of its own capacity, whether that constraint sits in feedstock or in processing.

For most of the past decade, that constraint was rarely a feedstock. China could supply its own market from its own ore with little difficulty, so a domestic price spike more often signalled processing bottlenecks or a genuine demand surge than any shortage of raw material. That has started to change.

Feedstock has become a live issue over the past two years because a material share of China's heavy rare-earth ore, dysprosium and terbium in particular, is sourced from Kachin State in northern Myanmar, and the civil conflict there has repeatedly disrupted those flows, including the loss of the Pangwa and Chipwi mining hub to Kachin forces in October 2024 and further supply interruptions during the fighting around Bhamo since.

Feedstock has also narrowed from the other direction. MP Materials, which had shipped its Mountain Pass concentrate to Shenghe Resources in China for processing, ceased those sales in mid-2025 as part of its DoD-backed floor-price agreement, redirecting output toward its own US processing and magnet capacity instead.

In December 2025, Brazil's Serra Verde, whose Pela Ema deposit is one of the few scalable non-China, non-Myanmar sources of dysprosium and terbium, renegotiated its roughly decade-long Chinese offtake agreements down to expire at the end of 2026, roughly eight years early, clearing the way for Western buyers once its output is freed up; a US$565 million DFC loan and a subsequent US$2.8 billion acquisition by USA Rare Earth followed within months.

None of these three cuts, Myanmar, MP, and Serra Verde, is individually large next to China's total feedstock base, but all three point the same way, and all three are recent. A domestic price spike now carries a second possible reading it did not carry before: not only is China approaching its processing limits, but its own feedstock security is being tested from more than one direction at once, on a border it does not fully control and from suppliers that have chosen to walk away.

The Ngualla exception

There is one acquisition running the other way, and it is worth being precise about what it does and does not change. In September 2025, China's Shenghe Resources completed a takeover of Peak Rare Earths, the owner of the Ngualla deposit in Tanzania, one of the largest NdPr-weighted deposits outside China, for roughly A$158-200 million. Against the Ore Reserve's contained NdPr, which values the resource in the ground at somewhere around US$0.55 to 0.70 per kilogram, a distressed price by any measure, made possible by Peak's collapsed share price, down from over A$1 in 2021 to around A$0.12 before the deal.

But this is not really a counterexample to the feedstock argument, for two reasons. First, Shenghe already held roughly 20% of Peak and 100% of its offtake before the takeover, so this consolidated a position it effectively already controlled rather than opening a new one; Ngualla's concentrate was always contracted to flow into Chinese processing regardless of who owned the equity.

Second, Ngualla is unlikely to be developed soon. Tanzania's government holds only a 16% free-carried interest, but its 2017 mining law tightened equity requirements and restricted the export of unprocessed concentrate, and the in-country processing terms Shenghe would need to finalise before a final investment decision have remained under negotiation into 2026 rather than resolved.

Some recent reporting suggests Shenghe may be content to leave the project mothballed rather than rush to meet Tanzanian in-country processing demands, particularly if China's own restrictions on exporting mining equipment, technology and personnel for critical-minerals projects abroad make that harder to justify. Tanzania has little practical leverage to force the pace: a free-carried minority stake gives it a seat at the table, not control over the timeline, and that will not change unless Tanzania rewrites the terms it negotiated with a different counterparty in mind.

The result is not additional supply for anyone. Ngualla is not adding tonnes to China's own processing pipeline, and it is not adding tonnes to the rest-of-world supply chain either; one of the world's largest NdPr-weighted deposits sits denied to both, which adds to the supply and price pressure described in this piece.

It also leaves Tanzania holding a free-carried stake in a mine that produces nothing, no royalties, no jobs, no processed value, for as long as the standoff over in-country processing terms continues. Read alongside Myanmar, MP and Serra Verde, Ngualla looks less like China building a new pillar of supply and more like China banking a cheap option against a future it is in no hurry to bring forward, at a cost being paid, for now, by Tanzania as much as by anyone else.

None of this is necessarily permanent. The standoff would break if a Western or Tanzanian-aligned party were willing to fund in-country processing on Tanzania's terms rather than wait for Shenghe to do so on its own. But that is not where investor capital is currently going in Africa, at least on paper.

Rest-of-world projects in the queue

Angola's Longonjo project is already at the construction stage with a 2027 commissioning target, backed by financing secured in December 2025 and an offtake agreement with the German magnet maker Vacuumschmelze. Malawi's Kangankunde project reached a final investment decision in August 2025, with Lindian Resources reporting construction progress through its own announcements toward a targeted Q4 2026 first production.

Both projects are further along the development curve and further along the queue for capital and offtake attention than Ngualla currently is. Ngualla sits behind them not because it is a worse deposit, but because it is a better deposit tied up in a worse negotiation.

Export controls as domestic supply security

That tightening feedstock picture points to an easy-to-miss reading of the export controls themselves. The controls are usually discussed as a form of leverage in the US-China trade relationship, and they clearly function that way. But leverage is not the only thing they do, and possibly not even the main thing. With a US$50-US$90 spread between the domestic price and the FOB-equivalent price for the same tonne of NdPr, a Chinese producer facing no export restrictions has every commercial incentive to sell into the export market rather than supply Chinese magnet and EV manufacturers at the lower domestic price.

Export controls, licensing and quotas do not only ration what the West receives; they also cap how much of a tightening domestic supply Chinese producers are permitted to divert abroad in pursuit of that spread. Read that way, the controls look less like a tool built for foreign policy that happens to also secure domestic supply, and more like a domestic supply-security mechanism that China is willing to use for foreign policy when convenient. Without them, and with feedstock now genuinely constrained, there is little reason to think China's own producers would prioritise the domestic market over the export price they can command.

SMM's FOB quote in context

The emergence of SMM's China FOB quote should be read in that context. Western buyers were increasingly finding the daily Chinese domestic spot quote irrelevant as a procurement benchmark: it still reflected China's internal industrial cost base but no longer reflected the price, availability, or permission risk faced by overseas buyers. A delivered-to-works in China price is not the same as an exportable, licensable, deliverable Western supply price, and SMM's FOB quote did not create that split; it acknowledged it. The quote begins to monetise the scarcity component of Western dependency. It is not the full Western cost, since tariffs, protectionism, rules of origin, compliance, financing and strategic inventory can all sit on top of it, but it is the first visible price marker showing that the West is no longer dealing with the same market as China's domestic manufacturers. China's domestic spot shows China's internal industrial advantage, SMM FOB shows the scarcity premium faced by the West, and Western protectionism adds a further layer on top. That is the cost of dependency, and it is why China's rare-earth market now must be read as two markets rather than one.

Why China FOB is both useful and risky

China FOB is useful because it gives OEMs, investors and governments a financial measure of dependency, showing what overseas buyers may have to pay when they rely on Chinese exports of materials that China can restrict, license, delay or refuse. It gives OEMs a way to quantify the cost of failing to secure independent supply.

But China FOB is risky if it becomes the benchmark for building the rest-of-world supply chain. Chinese OEMs compete on China's internal pricing, now anchored to the actual traded blend at roughly US$110/kg. Western, Japanese and Korean OEMs cannot build competitive EVs, wind turbines, robots, motors, defence systems or industrial platforms if their input costs are permanently set by China FOB. China FOB prices the risk; it should not become the target. The target is a rest-of-world supply chain that can eventually compete more closely on pricing with China's domestic market, while still offering sufficient returns to attract investment.

Where the floor sits

History has already tested this. Of the two major non-China NdPr producers that scaled up around the 2011 price spike, only one survived the collapse that followed. Molycorp's Mountain Pass operation restarted into the spike, expanded aggressively, and was funded heavily by debt, with no long-term offtake or price-support structure behind it; when prices fell back, Molycorp collapsed into Chapter 11 bankruptcy. Lynas survived. The difference was not geology or grade, since both were credible deposits; it was structure. Lynas had Japan behind it through JOGMEC and Sojitz, with loan-and-equity support, offtake and a route into Japan's industrial supply chain. Japan was not simply backing a mine; it was backing supply continuity, and that is why Lynas survived the trough: it had more than a resource and a processing plant; it had a buyer-backed structure tied to strategic demand. That is the lesson now being rediscovered in the United States.

The collapse itself deserves a closer look than it usually gets, and here I will give my own reading rather than the more common one. The standard account treats 2011 as straightforward: China restricted exports, prices spiked, competitors entered, China eased off, prices fell, competitors failed. I think the mechanism was more specific than that, and the timing supports it. The US, EU and Japan took China to the WTO over its export quotas in 2012; the WTO ruled against China in March 2014; and China, having exhausted its appeal, dismantled the quota system in stages between January and May 2015. Molycorp filed for Chapter 11 in June 2015, within weeks of China's compliance deadline. That sequence is not proof of intent, but it is more specific than "prices normalised."

My own view is that China had built out mining and processing capacity through the quota years to hedge against exactly the outcome the West was pursuing at the WTO: a ruling that would force the taps back open. When that ruling landed and the quotas came off, the capacity was already there, and it flowed. Whether that was foresight or simply the ordinary lumpiness of Chinese capacity build-out meeting a sudden change in export rules, the effect was the same either way, and the timing is hard to read as coincidence. The West fought for, and won, the legal right to unrestricted Chinese rare-earth exports. What it got, within months, was a price collapse that killed the one meaningful non-China competitor the 2011 crisis had produced, and left China's market position stronger than before the case was filed.

I do not think that lesson was lost on Beijing, and I do not think it has been revised since. In the decade since, China has not, as far as I can tell, treated the West as a market to be cultivated or a supply chain to be shared. It has treated it as a sink: somewhere to place excess capacity when convenient, and somewhere to withdraw supply from when it is not. That reading fits the pattern better than the alternative, and the April 2025 controls, discussed below, support it.

OEM behaviour after 2011 was straightforward. Chinese supply remained available, and once prices normalised, OEMs went back to it. They did not maintain the offtake and pricing support needed to keep non-China alternatives alive, and there was no commercial penalty for ignoring the warning.

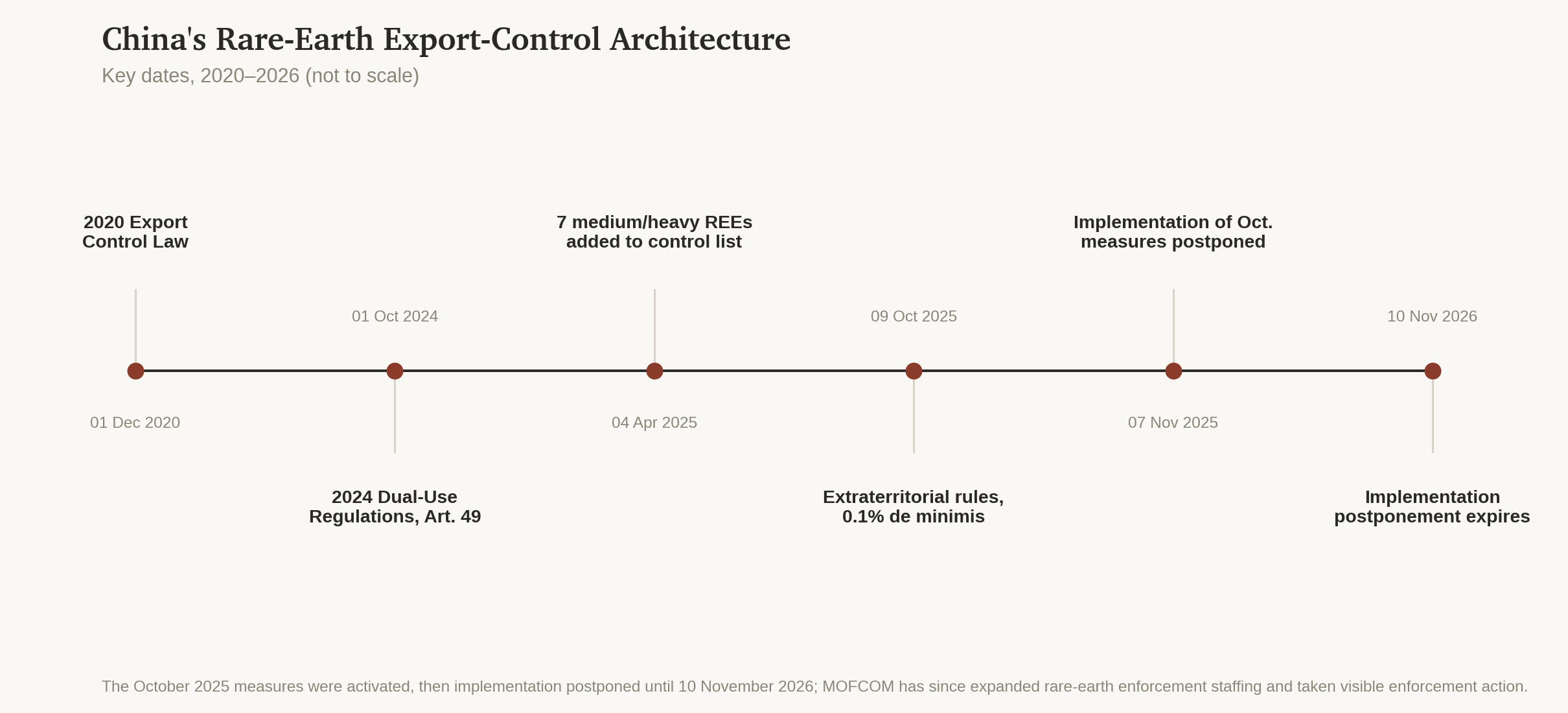

This time is different. China's modern export-control architecture rests on the 2020 Export Control Law and the 2024 Regulations on Export Control of Dual-Use Items; Article 49 of the 2024 regulation provides the legal basis for extraterritorial reach. On 4 April 2025, MOFCOM added seven medium- and heavy-rare earths, including terbium, dysprosium, samarium, gadolinium, lutetium, scandium and yttrium, to the control list, and exports now require case-by-case licences with a stipulated 45-working-day review period. On 9 October 2025, MOFCOM went further: it activated extraterritorial jurisdiction, requiring licences even for transfers of controlled rare earths between two countries outside China, and introduced a 0.1% de minimis rule for foreign-made products containing Chinese-origin rare earths alongside a 50% affiliates rule for related entities. Following US-China talks, China postponed implementation of the October measures on 7 November 2025 until 10 November 2026. That is a postponement of implementation, not a suspension of the measures themselves, and expiry of the postponement is not a review.

Why the postponement is not a wind-down

A postponement invites comparison to 2011: pressure, then relief, then a drift back to normal. Nothing in the record since 7 November 2025 supports that reading. The legal architecture, licensing bureaucracy and April 2025 controls remain in force throughout the postponement, and MOFCOM has been staffing up, not standing down, while it runs. Reporting in late 2025 indicated that its Bureau of Industry Security, Import and Export Control was launching its largest recruitment drive in nearly a decade, with the rare-earth control division a specific focus even as the truce with Washington held. Enforcement has followed the hiring. By mid-2026, a Chinese optics company chairman had been placed under compulsory measures over mis declared export documentation, MOFCOM had introduced a public reporting mechanism for strategic-mineral violations effective 1 July 2026, and China had added 10 US entities, including MP Materials and USA Rare Earth, to its export control list.

The clearest signal is Japan. Chinese customs data show that exports of dysprosium oxide to Japan stopped after October 2025, and of terbium oxide a month later, with no shipments of either recorded since. Beijing formalised the restriction through MOFCOM Announcement No. 1 of 2026, tightening licensing for medium- and heavy-rare-earth exports to Japan against the backdrop of remarks by the Japanese government on Taiwan. Two Japanese nationals, both Fuji Electric group employees, were detained in Dalian in May 2026 on suspicion of smuggling goods banned from export, and Japanese officials confirmed on 1 July 2026 that both had since been formally arrested, in mid- and late June respectively, over an alleged breach of China's rare-earth export-control law: one of the first known cases of a foreign national facing formal arrest in China over an alleged rare-earth export violation.

Read together, the Japan case shows China is willing to use this architecture with precision against a specific country and is prepared to do so again. A return to business-as-usual looks unlikely. An OEM that assumes it can wait out this cycle and return to Chinese supply is assuming an option that China is building the machinery, and now demonstrating the willingness, to switch off.

The floor mechanism

That is why OEM-backed offtake and floor structures are no longer discretionary. A floor around US$110/kg looks reasonable: it sits almost exactly on the actual traded 85/15 internal NdPr price of around US$110/kg, and well below the US$164/kg FOB-equivalent.

It is worth being clear about what this floor is and is not. It is not a subsidy intended to run indefinitely, and it is not protectionism dressed up as industrial policy; it is a temporary underwrite, priced close to where China's own domestic market already clears, that exists to get capital-intensive projects financed during the years before they have volume behind them.

It does not institutionalise a permanent scarcity premium; it creates bankability during the capital-intensive build-out phase. The mechanism gives projects the revenue visibility needed to finance assets, amortise capital expenditure and improve metallurgical performance, and as rest-of-world mining, separation and processing scale up, unit costs should compress toward industrial parity.

The floor is a bridge, not a destination: over time it should matter less as volume-driven price discovery takes over, and a floor still in place once that volume exists would be the clearest sign the model had failed.

The Lynas/Japan structure shows the principle in practice. The revised JARE agreement commits to 5,000 tonnes per annum of NdPr through 2038, with a US$110/kg floor price, while preserving Japanese access to long-term non-China supply. Mines and separators need throughput, offtake and scale; a small high-priced market may support a few assets, but it will not create a competitive industrial base. The rest of the world does not need a high-price rare-earth market. It needs a high-volume rare-earth supply chain.

The central tension

Investors need an acceptable risk-adjusted return. OEMs need secure supply at prices that allow them to compete with Chinese finished goods. Governments need resilience, but public money alone cannot create a market, and price reporting agencies can publish indices but cannot create price discovery without physical transactions. OEMs have to pick up the baton. They cannot expect China internal pricing before the non-China supply chain exists, but they also cannot accept China FOB indefinitely and expect to compete with Chinese OEMs.

Europe shows what happens when they do not. Solvay's La Rochelle plant is one of the few operating rare-earth separation facilities outside China, and CEO Philippe Kehren has been explicit that it is running at deliberately low output while it waits for exactly the kind of offtake commitment this section is describing: full-scale expansion, on the order of €100 million, is being held back for orders from automakers that have not yet arrived.

Kehren has separately described the support on offer in Europe as limited compared with what is available in North America, to the point that Solvay is now weighing a US facility alongside, or instead of, further French expansion. He is not an outlier. Other European rare-earth executives have told Reuters they cannot commit to raising output by 2030, and one industry analyst summarised the problem directly: at current price levels, most projects are not profitable without support from governments and automakers together.

That is the central tension in miniature, playing out at the one facility Europe has.

The question is not which material is cheapest today. It is what a manufacturer is prepared to pay during the build-out phase to secure supply that eventually allows it to compete. The China FOB spread helps answer that question: it gives OEMs a number to weigh against the cost of supporting independent supply through offtake, floors, prepayments, equity, inventory, or supply-chain partnerships.

The requirement of physical availability

Price is now secondary to physical availability. China FOB only matters if China is prepared to export. For a modern manufacturer, material that cannot be delivered has no price at all, and once export controls become industrial policy, procurement is no longer just cost optimisation; it becomes operational continuity. The buyer has to ask whether material will be supplied, whether a licence will be granted, whether the end use will be accepted, and whether the customer will be approved. The rest-of-world supply chain is not just competing with China FOB; it is competing with the possibility of no supply at all. OEMs need ex-China material because secure physical access to volume is now a prerequisite for manufacturing continuity.

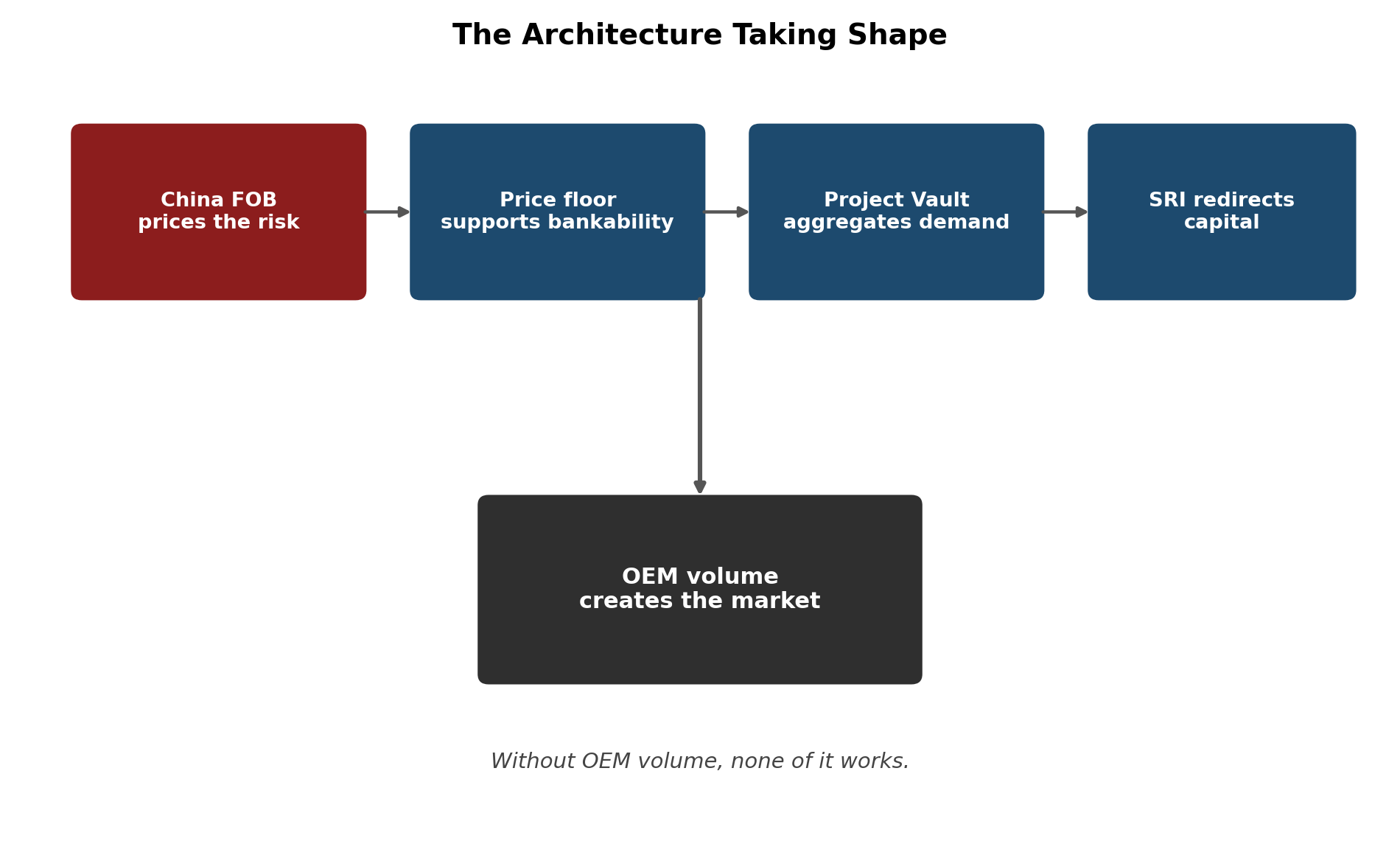

The architecture is taking shape.

This is where the US approach is more developed than others. Project Vault is intended to aggregate demand and create a physical security buffer; EXIM describes it as a US strategic critical minerals reserve structure, backed by a US$10 billion EXIM loan and nearly US$2 billion in private-sector investment. SRI-type initiatives redirect capital: JPMorgan describes its Security and Resiliency Initiative as a US$1.5 trillion, 10-year plan to finance

and invest in industries critical to economic security and resiliency, including an initial US$10 billion for direct investment in selected companies. The pieces fit together: China FOB prices the risk, a price floor supports bankability, Project Vault aggregates demand and inventory, SRI redirects capital, and OEMs create the volume. Without OEM volume, none of it works.

Japan understood the vulnerability earliest, and its approach worked. Its support for Lynas through JOGMEC and Sojitz was not just support for a mine; it combined finance, offtake, and industrial access, with the objective of ensuring continuity for Japanese manufacturers rather than simple ownership of a mineral resource. The United States is now belatedly trying to replicate that lesson on a larger scale. The contrast with MP Materials is instructive: MP did not restart as a complete Western rare-earth supply chain; it restarted primarily as a miner and concentrate producer, with its output tied to Chinese processing and offtake through Shenghe Resources. That got Mountain Pass operating again, but it did not solve the strategic problem: it gave the United States a mine, not a complete supply chain, and Western geology still depended on Chinese processing, Chinese offtake and Chinese market access.

The current US approach is an attempt to close that gap. The MP/DoD partnership creates a 10-year US$110/kg price-floor commitment for NdPr products and links price support, processing, magnet production and end-user demand. In effect, the United States is now trying to replicate the Japanese lesson: mines do not create supply-chain resilience unless finance, offtake, processing, conversion and end-user demand are tied together. Japan backed a supply chain, MP restarted as a mine, and the US is now trying to close that gap. Europe is waking up, but still leans too heavily on restrictions, targets and compliance rather than incentives, bankable demand and capital formation; restrictions can force demand away from China, but incentives are what pull supply into existence. For now, the direction of flow favours the United States because it is assembling more of the required pieces: demand aggregation, physical reserves, capital redirection, price floors and OEM participation.

Building a benchmark

Price discovery does not require every tonne to trade through an exchange, but it does require enough representative volume to create a credible reference price, which means a defined product, specification and delivery point. A ROW benchmark might be built on NdPr oxide at a clearly stated ratio, most likely 75/25 to align with market convention rather than China's domestic 85/15 norm, with defined purity, compliant origin, standard packaging and delivery to a recognised bonded warehouse, processing hub or industrial cluster. From that anchor, the market can price premiums and discounts for specification, Nd/Pr ratio, purity, origin, qualification, logistics, credit, delivery location and contract duration. The benchmark creates the anchor; the differential prices the real world.

Once that exists, the market can do its real job: deciding which resources are economic. Not every rare-earth resource should become a mine. Some deposits are geologically interesting but commercially irrelevant; others are lower grade but commercially attractive because of mineralogy, scale, infrastructure, jurisdiction, processing route, logistics, or downstream demand. Geology identifies resources. Price discovery determines which resources matter.

Conclusion

China FOB is useful because it shows what dependency costs, but it is not the price at which the rest of the world can build a competitive industrial base. The objective is not to replace Chinese dependency with a permanently high-priced Western market, but to build sufficient physical supply, processing capacity, inventory, OEM demand, and traded volume to create genuine ROW price discovery. That market must reward investment, but it must also produce material at prices that allow Western, Japanese and Korean manufacturers to compete with Chinese finished goods.

None of this happens in a vacuum, and it is worth being direct about what the evidence in this piece points to. The 2011 spike and collapse was not a one-off market correction; the timing around the WTO ruling suggests China had built the capacity to answer a forced reopening before that reopening arrived, and the West's legal victory delivered, within months, the collapse that killed its own nascent competitor. Nothing since has suggested that the lesson was forgotten. Feedstock has tightened from three independent directions at once: Myanmar, MP, and Serra Verde. Rather than easing its export controls in response, China has tightened them, enforced them against a Japanese company's own employees, and cut Japan off from dysprosium and terbium outright. Even where China has bought into the rest-of-world supply chain directly, at Ngualla, the effect has been to freeze the asset rather than develop it, denying supply to both sides rather than adding it to either. Read together, this is not the behaviour of a country treating the West as a market to be cultivated. It is the behaviour of a country that has learned to treat the West as a sink and sees no reason yet to change the lesson it drew in 2015.