Thoughts on resources, human capital, power and investment

(And some other stuff……)

Latest Blogs

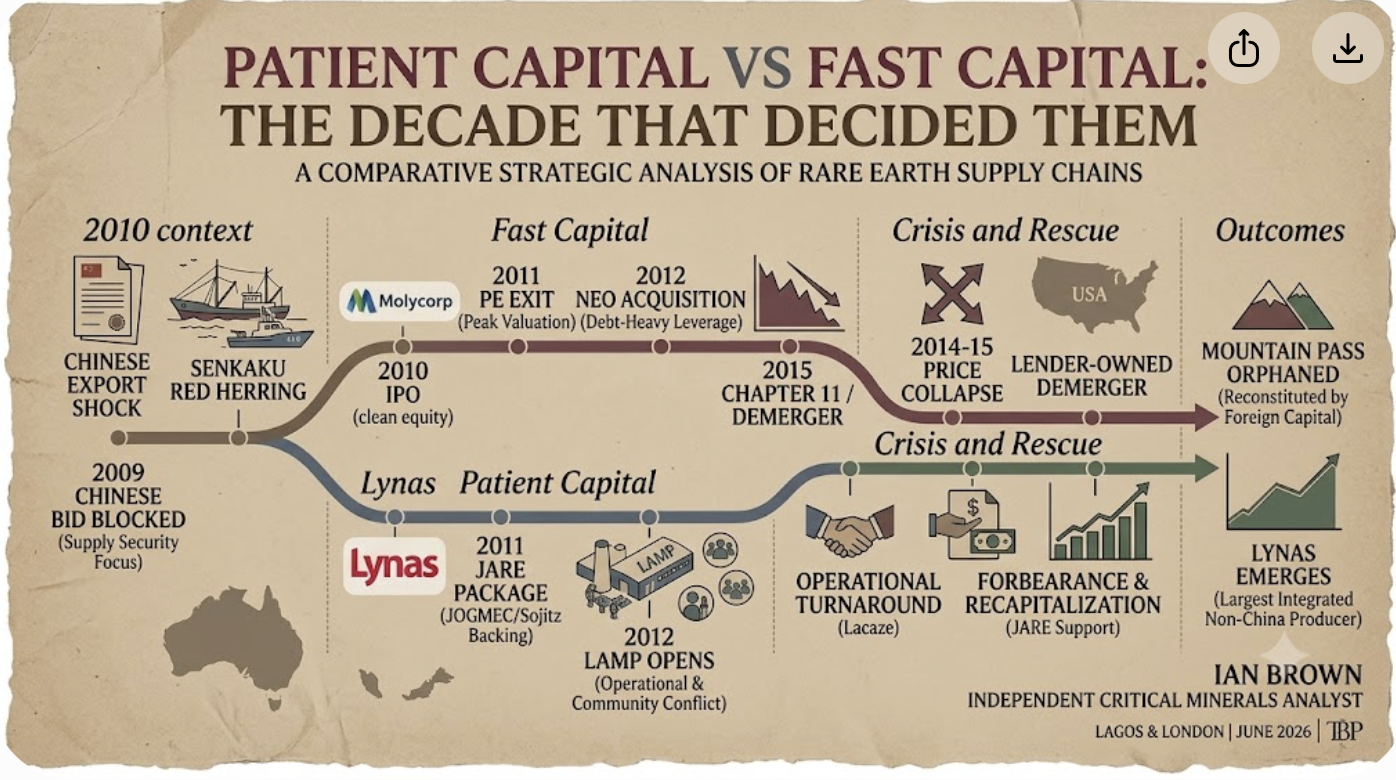

Mountain Pass and Mount Weld — the only two rare earth producers outside China operating at real scale today, and the only two that faced the identical 2010 shock and came out the other side.

One filed for bankruptcy. The other survived a worse collapse and is now the sector benchmark. The usual story blames China. The filings tell a more interesting one: a private equity windfall cashed out at the peak, a patient financing offer left to lapse, a $650 million bet placed against a WTO complaint that had already been filed — and, on the other side of the world, a lender holding the identical legal instrument who chose to extend a company's life rather than take it over.

A kilogram of neodymium and praseodymium costs $110 inside China. The same kilogram, loaded for export, costs $164. Landed in the United States, it costs $231.

That spread is not a pricing anomaly. It is the cost of dependency, and it is the subject of this paper.

Rare Earths and the Dual-Price Market traces how China's rare-earth market split in two: a domestic price reflecting its own industrial advantage, an export price reflecting everyone else's scarcity. It follows the evidence from the 2011 spike and collapse that killed Molycorp and spared Lynas, through the WTO ruling the West won and came to regret, to the export controls, arrests and cutoffs that show China has no intention of standing that architecture down.

It asks what a distressed acquisition in Tanzania and a tightening feedstock base suggest about how Beijing really sees the West, and the question every OEM sourcing NdPr has already answered, knowingly or not: what are you prepared to pay to avoid finding out the price of doing nothing?

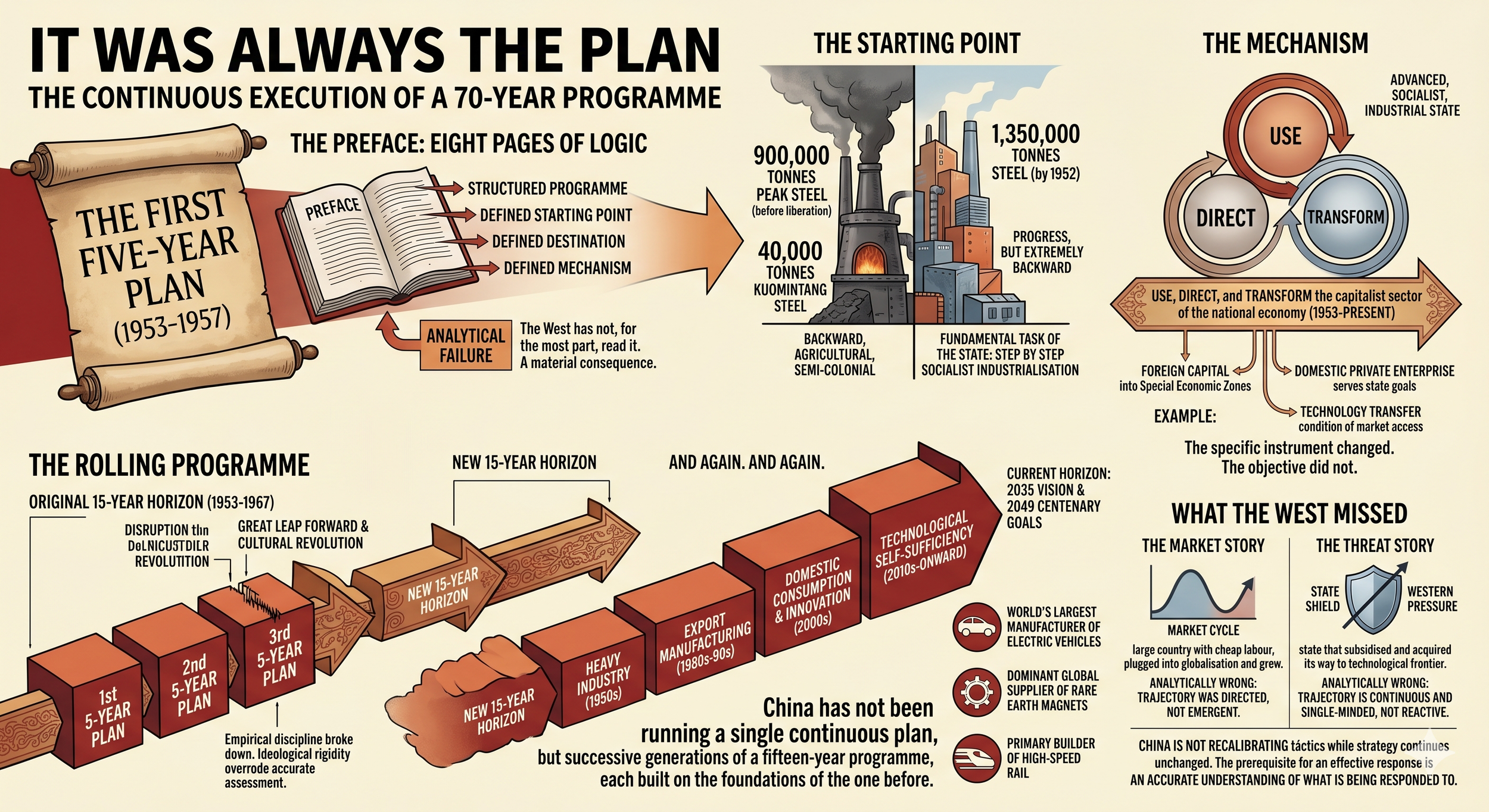

The provided text and the infographic argue that China’s global supply chain dominance is the deliberate execution of a continuous, 70-year strategic framework established in its 1953 First Five-Year Plan.

The core argument rests on three points:

The Generational Mechanism: In 1953, China diagnosed its "backward" economy and designed a repeating 15-year/three-plan rolling architecture to "use, direct, and transform" private and foreign capital toward becoming an advanced industrial state. The current 2035 Vision and 2049 goals are the direct continuation of this structure.

The Compounding Effect: By maintaining institutional memory across decades rather than disrupting policy for short-term political cycles, China systematically advanced from heavy industry to export manufacturing, and finally to technological self-sufficiency in critical minerals, magnets, and electric vehicles.

The Western Analytical Failure: The West misreads China’s rise as either an accidental market story of cheap labor or a reactive threat story responding to Western pressure. Because Western policy mistakes tactical adjustments for strategic shifts, it continuously deploys capital against symptoms rather than the root cause: a 70-year plan executed with absolute continuity.

In September 1942, the Liberty ship Robert E. Peary was launched four days and fifteen hours after her keel was laid. At peak production, American shipyards were delivering a completed oceangoing cargo vessel approximately every two days. At Willow Run in Michigan, a factory that did not exist in 1940 was producing B-24 Liberator bombers on a moving assembly line before the war was two years old.

These are not figures invoked for nostalgia. They are invoked because they represent the last time the Western industrial world faced a civilisational-scale mobilisation requirement and met it. The question that now demands an honest answer is whether that capacity still exists — and the evidence from the critical minerals sector suggests it does not.

There is a structural paradox at the heart of Western critical mineral strategy. Governments in Washington and Brussels now classify rare earths as essential to defence, electrification, industrial resilience, and national security. Multiple countries have written strategies, held summits, and announced funding initiatives. Yet when the time comes to finance the mines, separation plants, and downstream capacity needed to reduce dependency, the financial framework applied remains largely conventional commodity finance.

That matters because rare earths have not behaved like ordinary commodities for some time, yet Western financial markets still treat them as if they do.

The rare earth market is no longer defined by uncertainty, but by structure. Pricing, supply and demand dynamics are now sufficiently visible to allow a clear assessment of how the system operates — and where it is constrained.

A separation has emerged between China’s domestic market and the export market that serves the rest of the world. This divergence is not marginal. It reflects a structural difference in cost, availability and access to material, with implications for manufacturing competitiveness, capital allocation and supply security.

At the same time, the economics of new supply outside China are increasingly supported by prevailing market prices. The issue is no longer whether projects can be developed, but whether capital will be deployed at the scale and speed required to deliver them.

This paper examines the pricing structure of the rare earth market, the factors influencing investment decisions, and the role of policy in shaping supply. It sets out the case that the primary constraint facing the sector is not cost, but availability — and that this constraint is already influencing the pace at which dependent industries can develop.

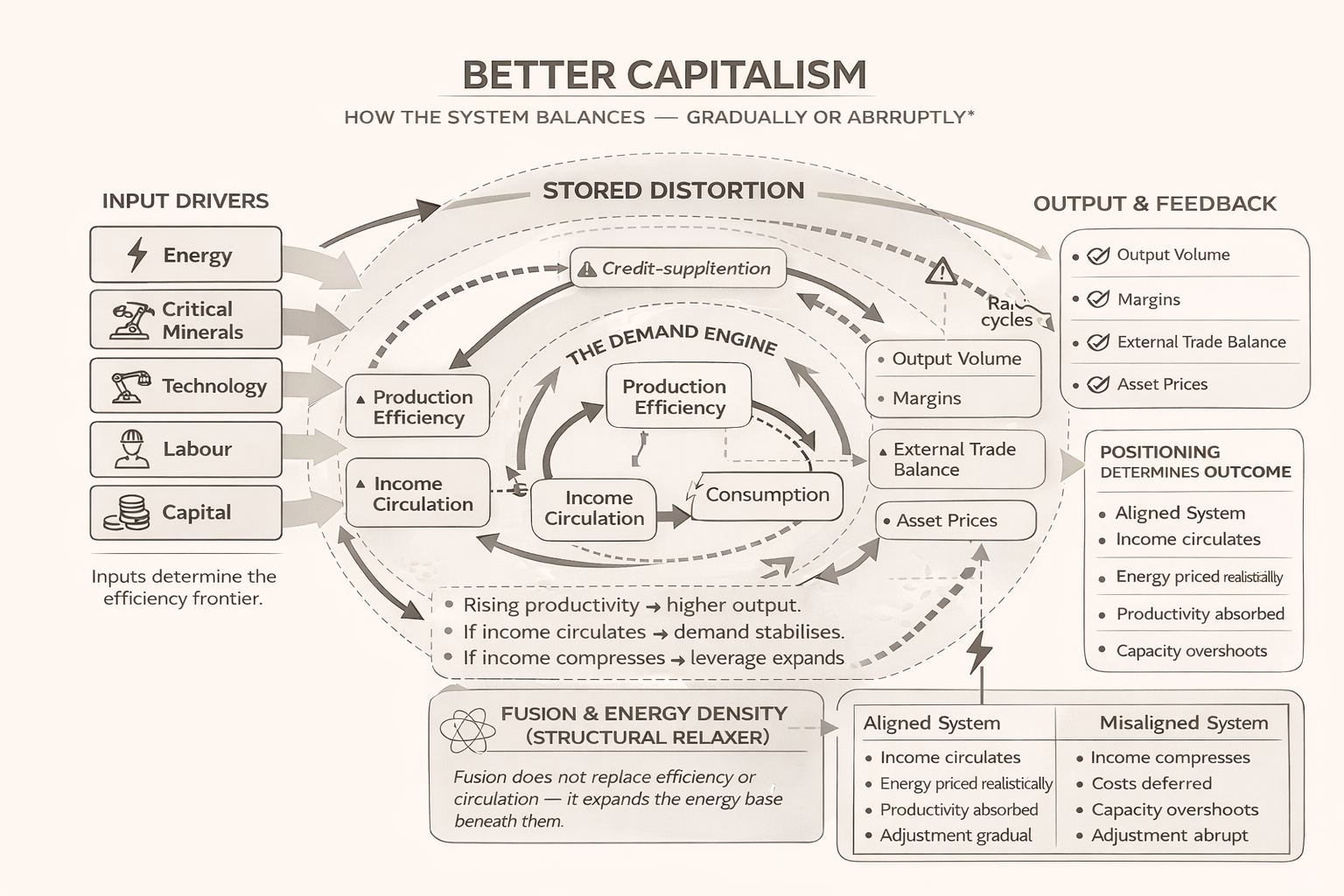

This paper considers the transition economy as a system. It examines how efficiency, scale, and capital allocation interact to shape outcomes, and why the shift toward electrification is better understood as a practical inevitability rather than the policy choice it is currently framed as. It focuses on underlying drivers — system design, resource constraints, and the movement of capital — rather than the political framing that often dominates the discussion.

It traces how differences in efficiency and system design have shaped the relative positions of China and the West, and how those differences influenced the allocation of capital and the development of supply chains. It also examines the role of distortion — where capital is either over-deployed or misallocated — and how this affects the pace and structure of the transition. Despite these distortions, the direction of travel remains consistent, with capital continuing to move toward systems that are more efficient and less constrained.

The intention is not to present a policy argument, but to set out a framework for understanding how the transition is unfolding. The analysis is grounded in observable patterns of behaviour across energy systems, industrial development, and capital allocation, and considers how these elements interact over time to produce outcomes that are structural rather than discretionary.

This paper begins with a simple observation: markets balance, but not always gently. Distortions in leverage, energy pricing, resource use, or income distribution can persist for years before adjustment occurs. When it does, it is rarely neutral.

Automation and electrification are reshaping production. Electricity is becoming the dominant form of usable energy across transport, manufacturing, robotics, and digital infrastructure. Critical minerals — small in monetary value but central in function — determine how efficiently that shift can proceed. Rare earths sit at key technical choke points. The possibility of fusion raises the question of whether the energy base itself could change.

Efficiency alone does not ensure stability. Margin depends on volume, and volume depends on broad and solvent demand. If gains concentrate faster than they circulate, leverage fills the gap. If costs are deferred, constraint eventually returns.

Markets will clear. The question is whether balance arrives gradually — or through correction.

Advanced economies are entering a phase of electrification driven not only by decarbonisation, but by efficiency and productivity. Electricity converts energy into work more effectively than combustion, and rising demand from electrified transport, heating and artificial intelligence is reshaping power systems. Meeting this demand requires sustained, long-term investment in generation and grid infrastructure.

At the same time, windfall taxation and price caps have re-emerged as politically attractive responses to periods of elevated profitability or tight supply in energy markets. This essay examines the tension between short electoral cycles and multi-decade infrastructure investment horizons. It argues that retrospective intervention alters capital expectations and raises required returns — with consequences already visible in energy markets.

The central issue is not the fairness of taxation, but the alignment of political time with capital time in an economy increasingly dependent on long-lived physical infrastructure. When recovery periods shorten and required returns rise, amortisation mathematics translates directly into higher electricity costs for households and industry.

For years, rare-earth markets appeared to function around Chinese benchmark prices. Production concentration inside China, declining liquidity elsewhere, and the migration of transactions into opaque contract channels had steadily eroded external price discovery. When structured pricing arrangements emerged in mid-2025 — most visibly through MP Materials and the United States Department of Defence — they did not cause the breakdown; they revealed it. Capital markets were left without credible benchmarks on which to finance new non-Chinese supply. A paper circulated in July 2025 reframed the problem as one of market structure rather than price levels, arguing that restoring liquidity, demand anchoring, and continuous transaction flow was essential to rebuilding price formation outside China. This paper traces how that market-reconstruction logic has since moved from analysis to policy, culminating in Project Vault — structured through the Export-Import Bank of the United States — which targets market infrastructure rather than price support. Rather than raising prices, the new framework rebuilds the market itself