THE CONSTRAINT IS NOT COST. IT’S AVAILABILITY.

Pricing, capital allocation and the emerging structure of the rare earth market

TWO MARKETS, TWO PRICES

There is no longer ambiguity in the rare earth market. The signals, the economics, and the strategic implications are clear. What is not clear is why the response remains slow. The market is not waiting, and yet policy and capital continue to behave as if they have time.

The starting point is simple. There is not one rare earth market, but two. Inside China, rare earths are priced within a domestic system designed to support downstream industry. NdPr at approximately $98/kg, with 13% VAT applied, results in an input cost of around $110/kg. Outside China, the rest of the world operates in a different reality. It pays export prices of roughly $175/kg, to which logistics, tariffs or VAT are added, resulting in a cost closer to $210–230/kg. This represents a cost difference approaching 100% more than Chinese manufacturers pay.

The mechanism by which these costs are applied differs, but the outcome does not. VAT systems in China and Europe apply tax to the full value of the finished product. In the United States, tariffs are applied once at import, embedded into the raw material cost, and carried through the value chain before sales tax is applied at the final sale. In each case, the end price reflects the accumulated structure. The distinction lies in the underlying cost base.

COST PARITY AND COMPETITIVENESS

Manufacturing competitiveness is determined by input cost. A system operating with input costs of approximately $110/kg is advantaged, over one operating at $220/kg, or twice the price for a comparable input.

There is no scenario where efficiency and engineering can offset that difference. Competing with Chinese production requires closer alignment with Chinese input cost.

The assumption that supplies outside China are inherently uneconomic does not align with observed pricing. The market is already paying ex-China prices of $175/kg and above.

Many projects indicate economic viability at $110–125/kg. Existing producers such as Lynas Rare Earths and MP Materials demonstrate that economic production outside China is achievable. The issue is not economic viability, but capital allocation.

MAKING THE BIFURCATION VISIBLE

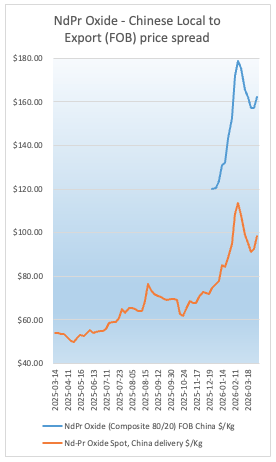

The pricing bifurcation between domestic Chinese supply and export markets was understood prior to being directly observable. It became transparent when SMM began publishing FOB prices for neodymium and praseodymium separately in December 2025.

The comparison shown is between FOB China export pricing and Chinese domestic spot pricing on a VAT-exclusive basis. The NdPr price is constructed as an 80/20 composite, consistent with the Chinese domestic specification. SMM reports domestic prices in RMB inclusive of VAT, and USD equivalents on a VAT-exclusive basis. The comparison uses the VAT-adjusted USD series to ensure consistency with FOB pricing. The data is there but requires handling to allow a direct comparison.

This establishes two distinct markets with two different pricing structures.

PRICE FLOORS AND THE COST CURVE

This distinction is relevant to the price floors now being agreed in rest-of-world production.

Several projects have indicated that NdPr prices below approximately $110–125/kg are not economic. This has often been benchmarked against Chinese domestic pricing. However, export pricing indicates that customers outside China are already paying $150–180/kg on an FOB basis, before freight, tariffs or VAT.

The $110–125/kg range is not a uniform threshold. Projects with favourable geology, low strip ratios and simplified processing flowsheets can operate below this level. The Longonjo Project being developed by Pensana in Angola is one such example, with a cost structure supported by low strip ratio, minimal overburden and existing infrastructure. This illustrates that the cost curve is not uniform and that a portion of supply can be competitive at lower levels.

Price floors in rest-of-world supply chains reflect observed market pricing rather than creating a premium. They are based on the price at which material is available outside China on a tax- and tariff-free basis. Their function is to provide revenue visibility sufficient to support capital investment.

CAPITAL ALLOCATION AND SCALE

The rare earth market is relatively small compared to bulk commodities. Returns can be attractive and sufficient in absolute terms, but the sector cannot absorb capital at comparable scale. As a result, projects compete for funding against opportunities that are larger and simpler. They are often rejected not because they are uneconomic, but because they do not offer sufficient scale.

A 20% return on $100 million is not equivalent to a 10% return on $1 billion, particularly where the effort and execution risk are similar. Capital allocation reflects absolute return relative to effort and scale. Incentives are aligned accordingly. In a smaller, more complex and higher perceived risk sector, acceptable returns may not attract capital without either higher margins or reduced risk.

This results in a delay in supply development. Projects are assessed against benchmarks that do not reflect their actual market and against competing opportunities that are not comparable. The outcome reflects capital allocation behaviour rather than project economics.

POLICY AS A SUPPLY CONSTRAINT

China’s control of supply extends beyond production. It especially includes the regulatory framework governing exports.

MOFCOM Order No. 18, introduced in April 2025, established the legal basis for export controls on strategic materials, including rare earth elements. MOFCOM Order No. 63, implemented in November 2025, amends the administrative and enforcement structure of the order with transitional arrangements extended to November 2026, after which the system moves into full effect.

This framework allows China to manage export availability independently of production. Supply to external markets is determined by both capacity and policy.

This introduces an additional constraint. Increased demand does not imply increased availability. Supply available to the rest of the world remains constrained or tightens further if Chinese domestic retention increases.

AVAILABILITY, NOT DEMAND

Rare earths are not a dominant cost component across most manufacturing in which they are a component, but they are a gating input in electric vehicles, offshore wind, robotics and defence. In these sectors, production is constrained by availability rather than demand.

If materials are available only for ten units, production is limited to ten units. Regardless of the price.

In the Defence Sector, the constraint is absolute. System availability is determined by material availability. Substitution is limited and delays are not acceptable.

SYSTEM EXPANSION REQUIREMENTS

Demand for permanent magnets outside China is forecast to increase dramatically with one recent estimate from SP Global, suggesting

“Demand for permanent magnets outside China will rise 50% by 2030. The consumption surge will require a 2-fold increase in rare earth mining, a 4-fold increase in refining, and a 6-fold increase in magnet production.”

Requiring expansion across mining, refining and magnet production. The constraint lies in the rate at which capacity can be developed across each stage and the alignment between them.

A shortfall at any stage constrains the system.

Apart from the strategic case, a strong commercial case for new supply exists. Pricing supports development. The strategic requirement for supply is also clear. The constraint is the rate of capital deployment and project execution

CONCLUSION

If supply does not expand at the required pace, production in dependent sectors will be constrained. This will affect electric vehicles, wind, robotics and defence systems.

The outcome is determined by structure. China currently operates at lower cost and controls export availability. The rest of the world operates at higher cost and depends on external supply. Demand is increasing, but availability is being constrained.

The question is not whether supply can be developed outside China. It must, the question is whether it can be developed in time.