Nigeria’s Future Is No Longer a Theory. It Is a Test of Consistency.

Nigeria has already absorbed the political and economic pain of long-avoided macroeconomic reform. Exchange-rate unification, subsidy removal, and fiscal adjustment have restored a measure of coherence to the economy, but these steps alone cannot determine the country’s trajectory. The central risk now is not reform failure, but reversal.

This paper argues that once a population has endured the costs of adjustment, continuity ceases to be optional. The binding constraint on Nigeria’s long-term growth is no longer price distortion or capital scarcity, but a deep and widening skills deficit driven by the erosion of educational credibility. Without reinvestment in education and primary healthcare, the gains from reform will dissipate rather than compound.

Nigeria’s future is no longer pre-ordained. Whether recent sacrifices translate into sustained growth or are squandered through policy reversal will depend on consistency, institutional repair, and the intelligent redeployment of reform dividends into productivity-enhancing public goods.

Why reform cannot be optional once pain has been paid for

Goldman Sachs has suggested that Nigeria could become the world’s sixth-largest economy, largely on the basis of its population size and land mass. In purely theoretical terms, that projection is defensible. Scale matters. Demographics matter. Geography matters.

But Nigeria also sits at the opposite end of the distribution. It is equally plausible that it could drift toward chronic underperformance—or even state failure. Two years ago, that latter outcome was clearly more likely than it is today. The balance has shifted, but it remains far from assured.

Recent policy choices have been necessary and overdue. Exchange-rate unification, the removal of fuel and electricity subsidies, and a more realistic fiscal stance have begun to restore macro coherence. The naira has stabilised, price distortions are being reduced, and capital allocation is slowly becoming more rational.

Crucially, the pain of adjustment was endured and is still being endured. For more than a year now, households and businesses have absorbed higher costs, inflationary pressure, and a sustained squeeze on disposable income. These reforms were not theoretical—they were lived through, and they continue to weigh on daily economic life. That matters, because it fundamentally changes what must come next.

Macroeconomic reform alone, however, is not enough.

Nigeria’s most binding long-term constraint is not capital, natural resources, or even governance in the narrow sense. It is the skills gap. Basic literacy has deteriorated over the past three decades, while the credibility of tertiary and postgraduate education has been deeply compromised. In many institutions, grades themselves have been sold—regardless of whether a student had passed or failed—destroying the signalling function of qualifications altogether.

The labour market has adapted, but imperfectly. Prospective employers increasingly assess potential directly—through interviews, testing, probationary periods, and on-the-job evaluation—rather than relying on domestic qualifications. At the same time, major employers show a clear preference for foreign degrees, particularly from well-known overseas institutions.

This preference does not imply that candidates educated abroad are inherently superior. It reflects risk management. In an environment where domestic credentials no longer reliably signal competence, foreign qualifications offer a lower-risk proxy for cognitive capability and academic rigour. The result, however, is that preference is disproportionately given to the children of the elite—those able to afford overseas education—regardless of whether they are the best candidates.

Exceptional individuals will always emerge. Some of the most capable professionals Nigeria has produced were educated abroad, and often at the very best institutions. One of the most capable engineers I have worked with held a doctorate from Cambridge. He was outstanding—but he was also, by definition, not representative.

At the top end of the distribution, such individuals still break through. At the bottom end, the struggle is fundamentally different. For those educated locally, without elite networks or the means to study abroad, the system is close to impassable. Many capable individuals are screened out before they are ever assessed.

This is not a moral critique of individuals operating within broken systems. Many academics are supporting families on incomes that fall below subsistence levels, often with limited alternatives. That context matters. But it does not justify the selling of grades or the erosion of academic standards. The behaviour and the conditions that enable it are separate issues—and both must be addressed. The outcome has been severe: credential inflation without capability, distorted hiring signals, rising inequality, and wasted human potential.

The good news is that this is not irreversible.

More importantly, the hardest part has already been done. Prices have been corrected, subsidies removed, and distortions confronted. These are the decisions governments usually avoid. Nigeria has not avoided them. That means the country is no longer fighting gravity. The question now is not whether reform is possible, but whether its gains are reinvested intelligently to generate multiplier effects across the economy.

As the government’s financial position improves, the central policy question shifts from reform itself to resource allocation. Power generation and distribution no longer need to dominate public spending. With electricity tariffs now closer to economic reality—and improving further as the naira strengthens—the sector can increasingly be left to private capital. Where price signals work, the state should step back.

That creates fiscal space—and obligation.

Public resources should now be redeployed toward education and primary healthcare, where market mechanisms alone cannot repair the damage. These are not soft social priorities; they are productivity multipliers. Without credible basic education and functional primary healthcare, the returns on infrastructure, industrial policy, and foreign investment are structurally capped.

The populace has already endured real hardship—and continues to do so. That reality changes the nature of political responsibility. Once a population has been asked to endure pain in the service of reform, continuity ceases to be a policy preference and becomes a moral obligation.

The single greatest risk to the gains now being made is political reversal. The danger is not technical failure, but the temptation to promise relief by undoing reform—reintroducing subsidies, distorting prices, and politicising the exchange rate once again. Such a reversal would not merely slow progress; it would waste sacrifice and make future reform far harder.

If continuity holds, however, the upside is powerful. Reinvesting reform gains into education and primary healthcare would deliver multiplier effects that compound over time: higher productivity, broader participation, lower inequality, and a labour force capable of absorbing capital rather than repelling it. This is how reform becomes growth rather than austerity.

Nigeria’s future is no longer pre-ordained in either direction. It is now a conditional outcome. But for the first time in a long while, the conditions for success exist. The difference between becoming a global economic heavyweight and remaining perpetually “next decade’s story” will be decided not by ambition, but by consistency—by whether the gains already secured are protected, reinvested, and allowed to compound.

Recalibrating Risk:Financing Critical Supply Chains In a Changed World

For more than two decades, Western economies accepted supply-chain concentration as an efficiency trade-off. That assumption is now breaking down. What has followed is no shortage of policy papers, task forces, and declarations of intent — but far less clarity on how resilience is financed and delivered at scale.

This paper focuses on that missing link. Using the recent U.S. capital-mobilisation response as context, it explores how risk is being recalibrated, how demand certainty is being rebuilt, and how financial architecture — rather than strategy alone — determines whether alternative supply chains become viable.

Beyond China is not about disengagement. It is about understanding what must change if critical supply chains are to be rebuilt in practice, rather than simply restated in theory.

Turning Strategy Into Action

There is a material difference between articulating strategy and executing it. In the UK and across Europe, supply-chain vulnerability and industrial dependency have been extensively analysed and documented in successive strategy papers. What has remained largely absent is a mechanism capable of translating those strategies into sustained capital deployment at scale.

By contrast, the United States moved beyond diagnosis toward execution. Events over the past year underscored the cost of delay, as supply disruptions demonstrated how quickly theoretical vulnerabilities become operational risks. Against this backdrop, the U.S. response focused less on further articulation of intent and more on constructing the financial architecture required to deliver outcomes.

In October 2025, Jamie Dimon, speaking as CEO of JPMorgan Chase, announced a Security and Resiliency Initiative intended to mobilise up to $1.5 trillion of financing capacity over the coming decade. The figure was not presented as a fund, nor as an annual spending commitment, but as aggregate deployable capacity across banks, institutional investors, and capital markets. Properly understood, it did not imply $1.5 trillion of new capital being raised or committed upfront, but rather the cumulative deployment of capital over time.

Based on what is publicly available, this paper interprets the initiative as an attempt to convert long-standing strategic intent into executable financial architecture. The ambition may appear bold at first glance but becomes more plausible when viewed through the mechanics of capital markets: recycled financing, risk-adjusted guarantees, revolving facilities, and capital-markets refinancing. The capital already exists; the challenge lies in creating the conditions under which it can be deployed repeatedly and at scale into sectors that markets have historically avoided.

The significance of the initiative therefore lies less in the headline number than in what it represents: a recognition that resilience is not achieved through strategy alone, but through execution. Where others continue to debate the problem, the U.S. has begun to build the machinery required to address it.

Strategic Context

For much of the past three decades, the United States and its allies accepted increasing supply-chain dependency because it delivered clear short-term benefits. Lower input costs, improved margins, and consumer price stability were treated as evidence of economic efficiency. China, by contrast, pursued a longer-term industrial objective: accelerating its transition from a developing economy to an advanced industrial power. By building scale across mining, processing, and manufacturing — and by accepting periods of oversupply and loss — China achieved in roughly thirty years what earlier industrial economies took a century or more to accomplish.

The strategic consequences of this asymmetry became evident as the United States began to pivot its trade and industrial policy, prompting a measured but deliberate response from China that underscored the extent of its leverage across critical upstream supply chains. For Western markets, outsourcing this risk once appeared rational; for China, accepting it was strategic. This reflects the recognition that China’s willingness to accept this risk early was a deliberate strategic choice — and one the United States now accepts it must also make

Supervisory board and the nature of the risk

When a capital mobilisation of this magnitude is contemplated to mitigate the industrial and supply-chain vulnerabilities identified above, the challenge extends beyond financing individual projects. Decisions around sequencing, priority, and acceptable risk inevitably carry systemic consequences across industrial policy, national security, and private capital markets. It is this requirement — to ensure strategic risk is carried with discipline and coordination — that makes an intended independent supervisory framework necessary.

Against this backdrop, JPMorgan indicated that the initiative would be guided by a supervisory advisory group drawn from senior figures in industry, technology, and national security. Publicly named participants include Jeff Bezos, Michael Dell, Ford CEO Jim Farley, and former U.S. Secretaries of State and Defence Condoleezza Rice and Robert Gates. Their role was not to allocate capital, but to help define strategic priorities — reflecting a shared assessment that the erosion of upstream processing, refining, and component supply posed a material risk to the U.S. industrial base. In stable conditions this dependency is largely invisible; under stress, it threatens production continuity across defence, energy, transport, and advanced manufacturing.

Why Risk Needs To Be Recalibrated In Critical Minerals

Risk needs to be recalibrated because it has been assessed against assumptions that no longer hold. For much of the past three decades, critical minerals and processed components could be sourced cheaply and reliably from external suppliers, allowing capital to favour projects with shorter timelines, lower capital intensity, and more predictable returns. In that environment, domestic critical mineral projects appeared disproportionately risky — not because capital was unavailable, but because it could find safer homes elsewhere.

That capital did not disappear. It was deployed into sectors and assets that were optimised for financial efficiency under prevailing market conditions, while strategic industrial capacity was allowed to erode. As long as external supply remained dependable, this allocation appeared rational. As supply chains have become increasingly exposed to geopolitical pressure and policy intervention, the true risk has shifted from investment to inaction.

Recalibrating risk does not mean lowering standards or insulating projects from failure. It means aligning risk assessment with current strategic reality — recognising that dependency carries cost, resilience has value, and that avoiding risk entirely in critical mineral projects represents a greater long-term danger than accepting it deliberately and managing it within clear limits.

How Recalibrated Risk Is Managed Without Undermining Capital Discipline

What has changed is not a willingness to ignore risk, but an effort to reduce and reshape it. Market capital was previously unwilling to engage with critical mineral projects because the risks were poorly matched to conventional financing structures. The current approach recognises that those risks must be mitigated — through partnership with government and through financing structures long used in infrastructure development — before private capital can participate at scale.

At the heart of this is a basic requirement of project finance: predictable cash flow. Lenders and long-term investors do not finance projects based on strategic importance alone. They require visibility on revenues, typically secured through long-term offtake agreements with creditworthy counterparties. In critical minerals, this requirement has historically been undermined by Chinese dominance. When a single supplier controls much of the processing, refining, or downstream manufacturing, alternative producers face the constant risk that demand can be withdrawn, undercut, or destabilised at short notice. As a result, demand risk — rather than geological or technical risk — became the binding constraint on financing.

What is now changing is the security and credibility of that demand. Chinese restrictions on exports, licensing, and processing — alongside the demonstrated willingness to weaponise supply — have made disruption no longer theoretical. For U.S. and allied manufacturers, reliance on Chinese supply now carries an operational risk that cannot be hedged in spot markets. Securing alternative sources has therefore become a commercial necessity rather than a strategic preference. That shift, driven as much by supply disruption as by policy, is what creates the durable demand required to support long-term offtake and, by extension, project finance.

Government policy reinforces this transition by shaping where demand can and cannot reside. In civilian markets, trade measures and incentives increasingly discourage reliance on Chinese-sourced products, while encouraging domestic and allied supply. In defence markets, procurement rules go further, effectively excluding Chinese-sourced inputs altogether. These measures do not create demand artificially; they prevent demand from collapsing back into Chinese supply during periods of price pressure or market stress. In project-finance terms, they stabilise the demand side long enough for alternative supply chains to be built.

Importantly, this demand is not unconditional. U.S. manufacturers must still produce affordable vehicles and compete in price-sensitive markets. Offtake mitigates volume and continuity risk, not cost discipline. Projects that cannot move down the cost curve, improve efficiency, or deliver at competitive prices will not sustain demand, regardless of policy support. In this way, affordability acts as a constraint that preserves capital discipline rather than undermining it.

Pricing and market risk are where government involvement is most directly felt. In markets subject to deliberate supply restriction or price suppression, conventional market signals break down. Policy intervention does not seek to fix prices or guarantee margins, but to prevent prices — or supply — from being manipulated to levels that render alternative producers unviable before they reach scale. By limiting extreme downside risk and supply disruption, government action allows pricing assumptions to be assessed commercially rather than existentially.

Execution and financing risks remain firmly with project sponsors and investors. Projects must still be built on time and on budget, comply with environmental and regulatory standards, and perform as expected. Capital remains exposed to loss, and failure remains possible. What has changed is that strategically necessary projects are no longer excluded simply because demand could be undermined by supply concentration beyond their control.

Taken together, this approach does not weaken markets. It restores financeability by aligning demand certainty, pricing stability, and capital discipline in a sector where all three were previously distorted. By addressing supply disruption as well as market structure, recalibrated risk can be carried by private capital without abandoning the principles on which project finance depends.

Against this backdrop, JPMorgan, working alongside the U.S. government, appear to have taken the view that by providing the appropriate enabling environment — including demand certainty, pricing stability, and risk mitigation of the kind described above — capital can be mobilised at scale to meet China head-on.

Closing Reflections

This paper has argued that the U.S. response to strategic supply-chain vulnerability is notable not for its scale, but for its execution. The mechanisms being deployed are familiar, the capital already exists, and the financial tools involved are orthodox. What differentiates the approach is the deliberate construction of architecture and an enabling environment in which private capital can engage with risks that markets had previously avoided.

That distinction matters because it reframes the debate elsewhere. The contrast with the UK and Europe is not primarily one of ambition or intent, but of comfort. Capital markets in the UK remain reluctant to engage with coordinated risk mitigation, policy-linked demand, and patient capital — even where those features are prerequisites for rebuilding strategically important capacity. The result is not a shortage of capital, but a persistent gap between strategy and deployment.

Crucially, this does not imply that others must replicate the U.S. response at scale. Smaller economies do not need trillion-dollar mobilisation to achieve resilience. They need proportionate architecture: clear demand signals, credible risk-sharing mechanisms, and coordination that enables markets rather than displaces them. Without these elements, strategy remains aspirational and capital remains sidelined.

The broader lesson is therefore a practical one. Strategic intent alone does not build supply chains. Capital alone does not deliver resilience. What matters is the framework that allows the two to connect. Where that framework exists, execution becomes possible. Where it does not, vulnerability persists — regardless of how often the strategy is restated.

The point is not to catalogue failure or assign blame, but to demonstrate that a solution is already visible. The U.S. experience shows that the challenge is not a lack of capital or imagination, but the absence of architecture that allows execution to occur. Where that architecture exists, markets respond. Where it does not, strategy remains theoretical.

From Market Cap to Cash:

Critical minerals sit at the intersection of geology, geopolitics and capital allocation. They are indispensable to the transition economy, yet notoriously difficult for conventional markets to value correctly. Investors accustomed to fast-moving sectors often misunderstand the economic structure of these assets, particularly the relationship between capital raised and value created. Nowhere is this clearer than in the rare earth sector, where a project’s potential is often considerable but its ability to realise that potential depends entirely on its access to funding.

This essay sets out the core economic principles behind critical mineral investing, and uses Pensana’s recent funding announcement as a case study in how value is created not by avoiding dilution, but by deploying capital where it has the greatest multiplier effect.

What Pensana Demonstrates About Value Creation

Critical minerals sit at the intersection of geology, geopolitics and capital allocation. They are indispensable to the transition economy, yet notoriously difficult for conventional markets to value correctly. Investors accustomed to fast-moving sectors often misunderstand the economic structure of these assets, particularly the relationship between capital raised and value created. Nowhere is this clearer than in the rare earth sector, where a project’s potential is often considerable but its ability to realise that potential depends entirely on its access to funding.

This essay sets out the core economic principles behind critical mineral investing, and uses Pensana’s recent funding announcement as a case study in how value is created not by avoiding dilution, but by deploying capital where it has the greatest multiplier effect.

1. The Market Assigns Value; Capital Unlocks It

Publicly listed Critical mineral projects often carry substantial implied valuations. These numbers come from resource size, recoveries, cost structures, engineering studies and projected demand. Yet these valuations remain intangible until converted into capital that advances development.

Pensana is a timely illustration. Prior to its recently announced $100 million strategic investment, the company carried a market-implied valuation of roughly $400 million based on 300 million shares and a prevailing share price around the £1 level. This valuation reflected market sentiment and project fundamentals, but it could not be used to build circuits, drill, expand resources or complete enabling infrastructure.

To progress a project, a company eventually must convert a portion of its market valuation into actual funding. This is not value destruction. It is the only way value becomes real.

2. Equity Is the Mechanism for Value Conversion

Pensana exchanged 25% of its equity for $100 million.

The mathematics were straightforward: 25% of a $400m company is $100m.

The buyer paid full market value — no discount, no repricing.

After the transaction, the company’s total economic value remained $400 million.

The difference was simply structural:

Before: the entire $400m valuation was intangible.

After: roughly $300m remained intangible and $100m became deployable capital.

This is the fundamental point:

shareholders did not lose value — the company merely changed the form in which that value is held.

3. Value Accretion Comes From Use of Proceeds, Not the Act of Raising Money

In critical minerals, capital only matters if it is deployed in areas that have a disproportionate economic impact. Pensana’s recent announcement illustrates this principle effectively.

According to the company’s published plan, approximately 30% of the proceeds are allocated to the heavy rare earth (HREO) recovery circuit. This circuit is associated — in the company’s own technical and economic assessments — with an uplift in project NPV of around $500 million.

This is where the economics become unmistakable:

A portion of the $100 million raised

Funds a circuit expected to add $500 million to project value

Generating an economic effect that far exceeds any dilution from equity issuance

This is not hypothetical. It is the direct output of the company’s published engineering and financial analysis.

In this sense, Pensana’s funding structure is not a story about dilution; it is a demonstration of value amplification: converting intangible valuation into cash, and that cash into an asset with materially enhanced economics.

4. Why This Matters for Investors

Many investors instinctively view dilution as negative. However, dilution without context is meaningless. The relevant question is:

Does the capital raised create more value than the percentage surrendered?

In Pensana’s case, exchanging 25% of the company for $100 million enables a development step associated with an uplift five times greater than the capital allocated. This is precisely how economically rational capital deployment works in critical minerals.

Moreover, because the remaining 75% of the company now sits atop a stronger, more valuable project, long-term shareholders participate in the enlarged economic base, even with additional shares in issue.

This is the principal economic misunderstanding in the sector:

equity dilution and economic dilution are not the same thing.

5. The Broader Lesson for the Sector

Critical mineral investing is fundamentally about resource transformation — the conversion of geological potential into industrial and strategic value. That transformation requires capital, and the economics of that capital determine whether a project becomes a national asset or remains a stranded deposit.

Pensana’s recent funding announcement is an instructive case study. It demonstrates that when valued at full market price and deployed into components of a project that materially shift the economic outcome, capital raising is not a dilution of value but a reinforcement of it.

Investors who understand this dynamic — who track the utilisation of proceeds rather than the existence of dilution — will recognise value creation long before the wider market does.

Conclusion

Critical mineral investing rewards clarity of thought, not reaction to noise.

Projects do not come to life because the market assigns them a high valuation; they come to life when that valuation is converted into capital, and that capital is deployed in ways that reshape the economics of the entire supply chain.

Pensana’s recent transaction is a clear example of this process.

It shows that strategic capital, judiciously applied, can turn a resource into an industry, and an implied valuation into actual value.

From Monopoly to Duopoly

Europe’s Strategic Blind Spot

Over the past few years, Western governments have spoken often about reducing dependence on China. But when you look at the actions being taken, a different picture appears.

In July, the U.S. Office of Strategic Capital received authority to deploy up to $100 billion. That single step makes the current situation clear:

Europe is not moving from dependency to independence.

It is moving from a Chinese monopoly to a US–China duopoly.

Europe’s Strategic Blind Spot

Over the past few years, Western governments have spoken often about reducing dependence on China. But when you look at the actions being taken, a different picture appears.

In July, the U.S. Office of Strategic Capital received authority to deploy up to $100 billion. That single step makes the current situation clear:

Europe is not moving from dependency to independence.

It is moving from a Chinese monopoly to a US–China duopoly.

With no major European or UK critical-minerals projects being funded, no matching urgency, and no equivalent capital support, the realistic choice will not be “China or self-sufficiency.”

It will be China or the United States.

Unless Europe begins backing real projects — not only strategies and policy papers, but actual mines, refineries, and magnet facilities — it will remain outside the most important industrial build-out in decades.

This raises a straightforward question:

Do European policymakers believe that breaking the Chinese monopoly is enough, even though relying on a “peace dividend” last time left them strategically exposed?

Strategy Isn’t Policy

Why Europe’s Critical Mineral Projects Cannot Attract Capital

Europe and the UK continue to release critical-minerals strategies. These documents outline familiar aims: increasing domestic processing, reducing dependence on China, and building more resilient supply chains. On paper, the direction looks positive. In practice, almost no major project in this area has secured bankable financing.

The reason is simple. Strategy and policy are not the same. A strategy states what a government wants to achieve. A policy creates the conditions that make it possible. Europe and the UK have produced many strategies but have introduced very little policy that shifts risk in a way that attracts capital.

Why Europe’s Critical Mineral Projects Cannot Attract Capital

Europe and the UK continue to release critical-minerals strategies. These documents outline familiar aims: increasing domestic processing, reducing dependence on China, and building more resilient supply chains. On paper, the direction looks positive. In practice, almost no major project in this area has secured bankable financing.

The reason is simple. Strategy and policy are not the same. A strategy states what a government wants to achieve. A policy creates the conditions that make it possible. Europe and the UK have produced many strategies but have introduced very little policy that shifts risk in a way that attracts capital.

Critical-minerals projects face long development timelines, commodity-price volatility, jurisdictional risk, and in some cases first-of-a-kind processing requirements. These factors push the natural risk level beyond what most investors can support without some form of state participation. European capital markets function as they are designed to: they allocate capital where the balance of risk and return fits their mandates. When governments declare a project “strategic” but offer no risk-sharing, investors price the project accordingly — as high risk with uncertain delivery.

A former colleague once put it bluntly:

“When you see the word ‘strategic,’ read high risk.”

Investors behave this way because it has generally proven correct. Without policy support, valuations fall to a small fraction of the underlying economic potential. This is not a judgement on project fundamentals. It is a reflection of unmitigated risk.

Until governments move beyond strategy and introduce practical policies that share or reduce risk, Europe’s critical-minerals ambitions will remain difficult to deliver.

How Two Western Assets Became Part Of China’s Long Game

Over the past decade, two significant narratives have shaped the rare earth elements (REE) market: the revival of the Mountain Pass mine in California and the decline and eventual sale of the Ngualla project in Tanzania. While each story stands on its own, their interplay illustrates a critical trend: China has consistently out-strategised and out-manoeuvred Western capital markets. Mountain Pass may have remained operational, but at a cost that ultimately favoured China. Conversely, Ngualla, recognised as one of the world’s premier neodymium-praseodymium (NdPr) deposits, slipped from Western control at a fraction of its true value. This analysis is not merely commentary; it reflects two converging timelines with significant implications.

Over the past decade, two significant narratives have shaped the rare earth elements (REE) market: the revival of the Mountain Pass mine in California and the decline and eventual sale of the Ngualla project in Tanzania. While each story stands on its own, their interplay illustrates a critical trend: China has consistently out-strategised and out-manoeuvred Western capital markets. Mountain Pass may have remained operational, but at a cost that ultimately favoured China. Conversely, Ngualla, recognised as one of the world’s premier neodymium-praseodymium (NdPr) deposits, slipped from Western control at a fraction of its true value. This analysis is not merely commentary; it reflects two converging timelines with significant implications.

Mountain Pass: A Western Asset Sustained Through Chinese Leverage

Mountain Pass experienced a dramatic collapse into bankruptcy in 2015 after the Molycorp expansion proved unsustainable. This expansion was predicated on a temporary spike in NdPr prices, triggered by the China–Japan territorial dispute. Following the West's victory in the WTO case against China’s export quotas, Beijing retaliated by flooding the market, which led to a steep decline in prices and rendered Molycorp’s new processing circuit economically unviable.

In 2017, a consortium, including Shenghe, acquired the asset from bankruptcy. Shenghe's investment of approximately US$50 million in offtake and prepayment support facilitated the mine's restart. In return, Shenghe secured 100% of Mountain Pass' concentrate and nearly a 10% economic stake.

From 2017 to 2020, Mountain Pass operated primarily as a mining entity. While the upstream ore remained under U.S. ownership, the value-added processing occurred in China. When MP Materials went public via SPAC in 2020, U.S. investors transformed Mountain Pass into a strategic asset. Federal programmes reinforced this narrative, resulting in a significant valuation increase, with MP Materials trading at an estimated US$10–12 billion by 2025. For Shenghe, this meant that its initial US$50 million investment had appreciated to approximately US$800–950 million. Although Mountain Pass was nominally Western-owned, a substantial portion of the economic value generated from its revival ultimately flowed to China.

Ngualla: A High-Quality Deposit Undermined by Delays

Discovered between 2009 and 2010, Ngualla quickly emerged as one of the most promising NdPr deposits worldwide, boasting high-grade ore near the surface, low radionuclide levels, a straightforward mining plan, and successful pilot-scale metallurgical tests. However, the project faced significant challenges, including stalled Special Mining Licence approvals and a withdrawal of investor interest, rendering Western financing nearly impossible.

Despite efforts by Peak Resources to derisk the project and the delivery of an updated Bankable Feasibility Study (BFS) in 2022, prolonged regulatory uncertainty weakened the company's financial standing. Between 2023 and 2024, Shenghe acquired a 19.9% stake in Ngualla and, in 2025, moved to acquire the project outright for approximately US$90–100 million. While Peak Resources advanced the project through feasibility studies, major changes to Tanzania’s mining legislation in 2017 stymied momentum. The acquisition price represented a mere fraction of the deposit's underlying NdPr value, highlighting a significant disconnect between the resource's fundamental quality and the capital market's willingness to support it.

The Convergence: Two Timelines, One Outcome

When viewed in tandem, the dynamics of both situations become evident. Shenghe's MP Materials valuation surged by nearly a billion dollars from 2017 to 2025, while Ngualla's valuation plummeted due to regulatory delays and a lack of Western financing. The result was straightforward: a strategic Western asset that succeeded (Mountain Pass) and another that faltered (Ngualla) both inadvertently bolstered China’s position—one through capital appreciation and the other through acquisition.

The Western Role: Keeping Mountain Pass, Paying the Price

While the West often heralds the revival of Mountain Pass as a strategic triumph, the economic record suggests otherwise. The mine was sustained, but at a significant cost, much of which was paid to China. Without Shenghe’s support in 2017, the restart would not have been possible. Likewise, U.S. investor enthusiasm significantly increased Shenghe’s economic interest. Thus, while Mountain Pass remained operational under Western ownership, the value generated from its revival predominantly enriched Shenghe.

The Reality of the Ngualla Acquisition: A 2023 Decision Point

Shenghe's aim to acquire Ngualla was already established in 2023, independent of MP Materials' subsequent valuation increase. Shenghe would have sourced the necessary capital regardless. What shifted between 2023 and 2025 was the relative significance of the acquisition. The uplift in MP’s valuation merely diminished Shenghe’s accumulated capital gain from its Western asset exposure. The US$90–100 million needed to acquire Ngualla was absorbed within the broader capital gains context, enabling Shenghe to enhance its NdPr resource base by over 150,000 tonnes with limited financial impact.

Conclusion: One Pattern, Two Case Studies

Mountain Pass and Ngualla did not exist in isolation; they are interwoven elements of a larger narrative. China adeptly supported Western revival when it served its interests while capturing the value-added opportunities that others overlooked. Through this strategy, China accumulated capital gains realised in Western markets, which were then deployed to secure global resource positions.

In contrast, the West successfully financed Mountain Pass’s recovery but failed to protect Ngualla’s development. Consequently, China fortified its strategic position through both outcomes. These parallel stories culminate in a singular conclusion: China has masterfully outplayed Western capital markets, leveraging their mechanisms to enhance its strategic standing in the NdPr landscape.

Sources and Supporting Documents

MP Materials / Mountain Pass

MP Materials / Fortress Value Acquisition Corp, Form S-4 (Sept 2020)

MP Materials 10-K filings (2021–2024)

Form 8-K (April 2025)

U.S. Bankruptcy Court Case 15-11357 (2017 acquisition)

PRC MOFCOM Export Regulations, April 2025

U.S. Department of Defense funding announcements (2025)

Peak Resources / Ngualla

Peak Resources ASX Announcements (2017 BFS, 2022 BFS, 2023–2025 regulatory updates)

ASX Substantial Holder notice (26 March 2024)

Scheme Implementation Deed (15 May 2025)

Scheme Booklet & Independent Expert Report (Aug 2025)

Peak Resources resource statements and technical disclosures

Tanzania Written Laws (Miscellaneous Amendments) Act 201

Market and Regulatory Context

WTO Case DS431 (2014 ruling on Chinese export restrictions)

USGS Mineral Commodity Summaries, Rare Earths (2015–2025)

Asian Metal / SMM rare earth pricing archives

Industry reports on NdPr demand and price cycles

Africa at the Centre of the Transition Economy

The global energy transition is shifting industrial power in real time, and Africa is at the heart of it. Since my presentation in January 2025, the continent’s role in the global transition economy has become even clearer. As electrification accelerates and demand for critical minerals reshapes industrial strategy, Africa has moved from the margins to the centre of new supply chains.

Meanwhile, Europe has hesitated. While the UK and EU debated strategies and policies, others acted. China, the United States, and African institutions have stepped in to seize opportunities. The outcomes of projects like Ngualla in Tanzania and Longonjo in Angola show what decisive partnerships achieve—and what delay costs. Africa is moving with clarity. The question is whether Europe will participate or continue to watch the transition economy move on without it.

The global energy transition is shifting industrial power in real time, and Africa is at the heart of it. Since my presentation in January 2025, the continent’s role in the global transition economy has become even clearer. As electrification accelerates and demand for critical minerals reshapes industrial strategy, Africa has moved from the margins to the centre of new supply chains.

Meanwhile, Europe has hesitated. While the UK and EU debated strategies and policies, others acted. China, the United States, and African institutions have stepped in to seize opportunities. The outcomes of projects like Ngualla in Tanzania and Longonjo in Angola show what decisive partnerships achieve—and what delay costs. Africa is moving with clarity. The question is whether Europe will participate or continue to watch the transition economy move on without it.

Africa’s Strategic Role in the Transition Economy

The global shift to clean energy is driving unprecedented demand for rare earth elements, particularly neodymium and praseodymium (NdPr), essential for permanent magnets in electric vehicles, wind turbines, robotics, defence systems, and emerging technologies. Outside China, processing capacity is minimal, leaving the world’s industrial base largely empty.

Africa, home to a significant share of the world’s critical minerals, is uniquely positioned to supply and shape these new value chains. Minerals like cobalt, manganese, graphite, copper, platinum-group metals, and rare earths are disproportionately located on the continent. Between a third and two-fifths of global critical mineral reserves are in Africa. Battery chemistries, wind turbines, hydrogen technologies, grid reinforcement, industrial electrification, and advanced manufacturing all rely on African resources—not as optional extras, but as structural necessities.

China’s Dominance and Africa’s Opportunity

Geopolitically, China controls around 40% of the world’s rare earth and critical mineral reserves, along with dominant processing capabilities. These resources are not available for Western diversification and are aligned with China’s long-term strategic goals.

This reality makes Africa the most viable source of non-Chinese critical minerals. Its centrality has been shaped as much by Europe’s hesitation as by African ambition. For over a decade, the UK and EU talked about securing critical minerals and reducing dependence on China. They published roadmaps and strategies, but when African partners sought early commitment and capital, Europe froze.

The result: China advanced into projects abandoned by Western financiers. The United States aligned with African-led developments. African sovereign wealth funds and development banks stepped into roles Europe had assumed would remain theirs. Europe lost ground not to competition, but to inaction.

Case Studies: Ngualla vs Longonjo

The contrast between two African rare-earth projects illustrates the consequences of commitment—or the lack of it.

Ngualla: A World-Class Project Left Behind

Ngualla in Tanzania is a globally significant deposit with exceptional geology and straightforward engineering. Tanzania had the chance to anchor a strategic industry. Yet when Peak Rare Earths needed early financing, Western capital did not step forward.

Tanzania’s fiscal terms—a 16% free-carried government interest, 3% royalty, and limited tax incentives—added pressure that only a committed partner could absorb. Policy resets between 2017 and 2021 further slowed approvals and created uncertainty. By the time Western interest emerged, it was too late. The project drifted through its critical window, highlighting the cost of hesitation.

Longonjo: Partnership in Action

In contrast, Angola’s Longonjo project demonstrates the power of clear partnership. Angola offered stable fiscal terms, including a 2% royalty, five-year corporate tax holiday, customs duty exemptions, and investor-friendly capital allowances. Its sovereign wealth fund, FSDEA, bought equity into Pensana, aligning financial interests and signalling confidence.

When Pensana’s share price fell in April 2023, Angola maintained stability. African institutions—including ABSA and the African Finance Corporation—added commercial and technical support. The United States later aligned behind the project. Today, Longonjo is the most advanced NdPr project outside China, achieved not through Western support, but because Angola chose partnership, clarity, and consistency.

Europe’s Missed Opportunities

Europe’s hesitation cost more than African projects—it cost downstream industries that could counter China. Teesside in the UK, a planned NdPr refinery dependent on Ngualla, never materialised. Saltend, another first-of-its-kind rare-earth separation facility, stalled due to lack of upstream financing. European capital markets, despite their rhetoric on strategic autonomy, failed to fund the projects needed to realise it.

Africa’s institutions stepped in where Europe did not. Projects that could have secured Europe’s industrial future now advance without it.

Africa Moves Forward

Africa has not been harmed by Europe’s absence. The continent is adapting, partnering, and setting terms to retain value. Europe, by contrast, has forfeited influence and ceded ground to China and the United States. Supply chains are forming without it, and early influence rarely returns once lost.

Africa is no longer a passive exporter. It is defining its role in the transition economy while Europe risks becoming a permanent taker of strategic materials rather than a maker of industrial futures. The decisive decade has begun. Europe must now decide whether it intends to be part of this future or continue watching from the shore.

Who got it, Who gets it, And Who Still Needs To Smell The Coffee

The story of how China came to dominate the global rare earth magnet industry does not begin with China. It begins in the laboratories of Japan and the United States in the late 1970s and early 1980s, when researchers at Sumitomo Special Metals in Osaka and General Motors in Indiana independently invented the neodymium-iron-boron (NdFeB) magnet. These were revolutionary technologies—one sintered, one bonded—that placed the West at the centre of a supply chain that would become foundational to electronics, automotive engineering, defence systems, and later the entire electrification economy. At that moment, it was unthinkable that China, then still industrially undeveloped, would one day control nearly every stage of this value chain.

1. WHO GOT IT — CHINA’S 30-YEAR HEAD START

The story of how China came to dominate the global rare earth magnet industry does not begin with China. It begins in the laboratories of Japan and the United States in the late 1970s and early 1980s, when researchers at Sumitomo Special Metals in Osaka and General Motors in Indiana independently invented the neodymium-iron-boron (NdFeB) magnet. These were revolutionary technologies—one sintered, one bonded—that placed the West at the centre of a supply chain that would become foundational to electronics, automotive engineering, defence systems, and later the entire electrification economy. At that moment, it was unthinkable that China, then still industrially undeveloped, would one day control nearly every stage of this value chain.

What changed was not geology but a series of decisions, incentives, and industrial strategies that gradually shifted not just capacity, but capability—specifically IP and process knowledge—out of the West. The pivotal moment came with the sale of Magnequench, General Motors’ magnet subsidiary. Originally protected by conditions intended to keep production in the U.S., Magnequench was eventually bought by a consortium involving Chinese and Japanese interests. When those restrictions expired, the machinery, the people and the operational knowledge were relocated to Tianjin. The West did not merely lose a factory; it lost the tacit knowledge that underpins manufacturing: the “how”, not just the “what”. Magnequench was not the only example, but it was the most symbolic. It helped seed the first serious capabilities in China’s magnet industry.

Throughout the 1990s and 2000s, China’s approach to intellectual property followed a consistent pattern: IP was respected when convenient—and ignored when it created barriers to national industrial goals. Western companies entering the Chinese market often did so through joint ventures requiring technology transfer. IP enforcement was inconsistent, legal frameworks were still maturing, and the distinction between proprietary methods and broadly understood industrial practice blurred quickly. Magnet technology spread rapidly across Chinese plants through observation, replication and cumulative learning. Much of this happened long before Western patent holders mounted serious legal challenges.

Those challenges came, but too late. Hitachi Metals, which held hundreds of patents covering alloy compositions, sintering conditions, grain boundary diffusion and coercivity enhancement, eventually acted in China. The defining moment came when a lower Chinese court ruled that Hitachi’s patents were “monopolistic” and granted a compulsory licence allowing Chinese producers access to patented processes. Years later, China’s Supreme People’s Court overturned the decision—but by then most of the key patents had expired, and China had long since absorbed their value. The ruling was symbolic; the industrial outcome was already settled.

As these capabilities grew, China aligned them with deliberate industrial policy. Through the 1990s and 2000s, China expanded extraction, built vast solvent extraction complexes, developed metal and alloy production, and invested heavily in magnet-making cluster regions. Export quotas constrained the flow of rare earth materials to the rest of the world, protecting domestic industry. Subsidies and low environmental enforcement reduced costs. The strategy was simple: scale, integrate and undercut.

The moment the rest of the world finally recognised its vulnerability came in 2010, when a diplomatic dispute between China and Japan resulted in a temporary suspension of rare earth shipments to Japan. Prices spiked more than twenty-fold. Supply chains froze. Policymakers panicked. The U.S. attempted to rebuild its lost domestic industry through Molycorp, restarting the Mountain Pass mine and developing new processing operations. But Molycorp lacked modern midstream IP, lacked downstream alloy and magnet capability, and lacked the decades of accumulated operational experience China already possessed. When the WTO later forced China to remove export quotas, China responded by flooding the market with additional supply. Prices collapsed. Molycorp’s economics disintegrated. By 2015, the company was bankrupt. The West had lost the midstream a second time—first through IP migration, then through price warfare

2. WHO GETS IT — JAPAN, THE UNITED STATES, AND THE NEW STRATEGIC SUPPLIERS

Japan, meanwhile, drew a different conclusion. Determined never again to rely solely on China, and recognising the fragility of U.S. industrial capacity, Tokyo made a strategic investment in Lynas. JOGMEC and Sojitz provided financing, offtake guarantees and technical support. Lynas survived the price collapse because Japan treated rare earths as strategic. Molycorp failed because the United States did not. By the mid-2010s, Lynas had become the only major non-Chinese producer of separated rare earth oxides in the world.

Having achieved capability and dominance, China reversed its earlier openness. Advanced magnet-making technologies were reclassified as strategic. Export controls tightened. Technical information and talent became more restricted. Processes that had once been flexible to access became rigidly protected. China had completed the industrial cycle: open on the way up, closed once it arrived.

This is the landscape the United States re-entered in the 2020s—without domestic separation capacity, with minimal metallisation capability, with no large-scale magnet production and with defence supply chains fully dependent on China. The shift began not with markets but with policy. Section 1260H of the 2021 National Defense Authorization Act set a clear requirement: from 2027, the Department of Defense would be prohibited from procuring NdFeB magnets, SmCo magnets or components containing them if any stage of production originated in China. For the first time in four decades, the U.S. created a legal forcing mechanism to rebuild a non-Chinese supply chain.

Meeting the 2027 requirement required more than mining projects. It required IP. China’s advantage was built on 30 years of accumulated process knowledge. The U.S. could not simply “catch up” through investment. Instead, it began acquiring the IP it lacked.

ARA Partners’ acquisition of VACUUMSCHMELZE (VAC) brought one of the world’s most advanced magnet-making intellectual property bases—German, not Chinese—into the U.S. sphere. USA Rare Earth’s acquisition of Less Common Metals (LCM) in the UK brought Western strip-cast alloy IP under U.S. ownership. These two transactions recovered decades of lost capability.

The third pillar came not from acquisition but invention. ReElement Technologies developed a chromatographic separation and metallisation platform that reduces capex, slashes opex and avoids dependence on China’s large-scale solvent extraction complexes. Because ReElement’s process is new, American-owned and structurally different from legacy SX, it bypasses the IP bottleneck entirely. This offers the U.S. a genuinely alternative midstream technology—something it has not possessed in 30 years.

Upstream, projects aligned with U.S. strategic priorities began receiving EXIM and DFC funding: Serra Verde in Brazil, MP Materials in the U.S., and increasingly Pensana in Angola, which offers a non-Chinese, high-grade NdPr source backed by sovereign African capital. Pensana’s low strip ratio, renewable hydroelectric power, rail integration and proximity to port make it one of the most economically advantaged upstream projects in the world—synchronised with the 2027 timeline in a way few others are.

These developments represent the first coherent Western reconstruction of a rare earth magnet ecosystem since the 1980s. The strategy is fundamentally different from China’s, but based on the same principle: commercial capability, not rhetoric, determines industrial reality

3. WHO STILL NEEDS TO SMELL THE COFFEE — THE UK AND EUROPE

The UK and Europe have produced strategies, frameworks, risk assessments and declarations—everything except actual industrial capacity. While Japan wrote cheques and the U.S. wrote cheques and acquired IP, Europe issued press releases. The result is predictable: no large-scale separation plants, no metallisation, no magnet plants of consequence, and no cost-competitive alternative to China.

The UK’s Saltend project obtained planning permission but never funding. The EU launched the Critical Raw Materials Act yet still has no serious magnet capacity behind it. Across the continent, there remains a mismatch between political rhetoric and industrial execution. Committees form. Reports are written. But the factories, engineers and process IP simply do not exist.

In a market defined by cost, capability and learning curves—not declarations—Europe is becoming a spectator rather than a participant

4. THE REAL GAME — EXTRACTIVE ECONOMICS & MIDSTREAM INNOVATION

The West’s new supply chain blends reacquired IP (VAC, LCM), new IP (ReElement), advantaged resources (Pensana, Serra Verde, MP) and policy certainty (the 2027 DoD requirement). For the first time in decades, the pieces align.

Pensana demonstrates how a modern rare earth project can be built on fundamentally advantaged geology, low strip ratios, renewable power and integrated rail logistics—delivering feedstock at a cost base few competitors can match.

ReElement shows how new chemical engineering can reduce the capex and opex of separation and metallisation to levels that challenge the economic assumptions China has relied on for decades.

Together, these models create the first commercially credible route to produce rare earth products outside China at competitive cost.

5. CLOSING — IP AND INNOVATION TO NEUTRALISE CHINA’S ADVANTAGE

Ultimately, the only way to counter China’s dominance is through a combination of extractive economics upstream and innovation-driven efficiency downstream. Pensana demonstrates how a modern rare earth project can be built on fundamentally advantaged geology, low strip ratios, renewable power and integrated rail logistics — delivering feedstock at a cost base few competitors can match. But upstream advantage is only half the equation. The other half lies in technologies like ReElement’s, which reduce the capex and opex of separation and metallisation to levels that break the economic logic China has relied on for decades. Together, these approaches show the path forward: use resource quality and operational efficiency to drive costs down at the mine, then use new IP and new processes to drive costs down in the midstream. If the West can combine these two strengths — Pensana’s extractive economics and ReElement’s disruptive cost profile — it can finally begin producing rare earth products competitively enough to neutralise China’s advantage. In the end, this is what matters: IP and innovation deployed to deliver rare earths as economically as possible, turning strategic ambition into commercial reality.

From Complacency to Panic to Delusion — How the West Misread China’s Pause

In March 2025, the new United States administration under President Trump reintroduced a series of tariffs on Chinese industrial products, including electric vehicles, batteries, and critical minerals. The measures were justified as a response to what Washington described as “market distortion and state subsidy.” Beijing’s response followed just over a week later, not through tariffs of its own but through regulation. On 4 April, the Ministry of Commerce issued Announcement No. 18, designating several heavy rare-earth elements — samarium, gadolinium, terbium, dysprosium, and lutetium — as “dual-use technologies” under China’s 2020 Export Control Law. The message was clear: if Washington intended to use trade as leverage, Beijing would use access.

MOFCOM 18 set the tone for the rest of the year. It became the first in a series of policy actions that reshaped sentiment across the rare-earth industry and revealed how differently China and the West interpret economic strategy. Beijing acts within a coherent framework; the West reacts to headlines.

The Policy Catalyst

In March 2025, the new United States administration under President Trump reintroduced a series of tariffs on Chinese industrial products, including electric vehicles, batteries, and critical minerals. The measures were justified as a response to what Washington described as “market distortion and state subsidy.” Beijing’s response followed just over a week later, not through tariffs of its own but through regulation. On 4 April, the Ministry of Commerce issued Announcement No. 18, designating several heavy rare-earth elements — samarium, gadolinium, terbium, dysprosium, and lutetium — as “dual-use technologies” under China’s 2020 Export Control Law. The message was clear: if Washington intended to use trade as leverage, Beijing would use access.

MOFCOM 18 set the tone for the rest of the year. It became the first in a series of policy actions that reshaped sentiment across the rare-earth industry and revealed how differently China and the West interpret economic strategy. Beijing acts within a coherent framework; the West reacts to headlines.

Complacency

For several years, critical minerals had been discussed in Western policy circles but rarely acted upon. Strategies were drafted, committees formed, and targets set, yet the investment required to build alternative supply chains never followed. Projects outside China were treated as interesting but non-essential. Investors assumed that China would continue to supply the world, just as it had for two decades. That assumption did not survive the re-emergence of tariffs.

The rare-earth market responded immediately to MOFCOM 18. Prices strengthened, trading volumes increased, and projects such as Pensana, Iluka, Arafura, Lynas, Vital Metals, and Mkango returned to analyst coverage. Their valuations remained low but began to rise for the first time in years. As the new export-licensing rules started to take effect, several automakers reported temporary factory closures and reduced production, citing the non-availability of magnets and alloys dependent on Chinese rare-earth supply. The classification of rare earths as dual-use materials signalled that these were no longer routine commodities but inputs critical to both industrial and defence manufacturing. The linkage between policy and production became visible within weeks.

Panic

Through the summer, confidence continued to build. The United States and Europe began to align policy on critical minerals, and financing discussions moved from theory to implementation. Export-credit agencies and development banks started assessing offtake-linked project funding. Pensana confirmed African backing for its Longonjo project, and construction was scheduled to begin. For the first time, the market was responding to delivery rather than narrative.

Then Beijing issued MOFCOM Announcement No. 62. It was not a refinement of earlier measures; it was a demonstration of control. The order expanded the April framework to cover not just materials but the full spectrum of rare-earth technology — mining, separation, smelting, magnet manufacturing, recycling, and any technical services or software that could support production outside China. It was a clear statement of ownership and intent, showing that Beijing was prepared to wield its advantage without hesitation.

The effect was immediate. Rather than cooling sentiment, the announcement intensified it. Investors interpreted it as proof that China regarded rare earths as a strategic instrument and was prepared to use them accordingly. The Financial Times described the order as “Beijing’s most comprehensive single-sector intervention to date.” For Western governments, it confirmed what developers had been arguing for years: diversification was no longer a commercial objective but a strategic necessity.

The rally only broke in the days before the Trump–Xi summit in Korea. On the Sunday preceding the meeting, U.S. fund manager Scott Bessant told a television panel that “a deal was done” and that China’s rare-earth restrictions were effectively over. Algorithms reacted instantly. Within hours, positions reversed. MP Materials in the United States and Lynas Rare Earths in Australia — then the sector’s two largest companies — led the decline. By mid-week, coordinated short positions had appeared across the sector from Sydney to London. The entire complex lost nearly forty per cent of its value in less than two weeks.

Companies that had just achieved major progress found themselves using that progress to stabilise their share prices. The fundamentals had not changed; sentiment had. The correction was not driven by operational failure but by misinterpretation.

Delusion

Beijing’s next move came on 7 November, when MOFCOM and the General Administration of Customs issued Announcement No. 70, a one-page notice suspending enforcement of the October controls for one year. The document did not revoke the earlier measures; it simply deferred their application until 10 November 2026. Yet the nuance was lost. Western media ran headlines claiming that China had “backed down.” Analysts and policymakers interpreted the announcement as evidence of de-escalation. Few had read the document itself, which existed only in Chinese.

The market largely missed that distinction. The announcement was interpreted as a relaxation of policy rather than a procedural delay. In reality, there appears to be no mechanism to extend or renew the deferral. Once it expires, the controls automatically return in full effect unless replaced by a new directive. The structure of the policy remains intact, unchanged in scope or intent.

The immediate reaction, however, was relief. Liquidity improved slightly, but conviction did not. Coverage across the sector thinned, and the term “non-Chinese premium” disappeared from analysis. Projects that had begun to attract fair-value attention were again priced as speculative. The West congratulated itself on a perceived diplomatic success, while China quietly retained every lever of influence.

Five days after MOFCOM 70 was issued, the market was still cautious. Prices had stopped falling, but there was no clear sense of direction. Investors understood that the logic for developing independent supply remained sound but were reluctant to act. The momentum created by funding and construction progress now has to rebuild itself under greater scrutiny.

Reflection and Reckoning

Share prices are inching higher, yet confidence is still lagging behind. The same companies that were finally recognised as undervalued before October now have to prove again what is already obvious: their fundamentals were never the problem — only perception. The West misread a pause as a concession and, in doing so, reinforced the leverage it hoped to avoid. MOFCOM 70 confirms China’s position: enforcement of the October rules is deferred, not withdrawn, and the April export restrictions remain in force. Nothing has been lifted; only the timeline has changed.

As the sector tries to make sense of events, Financial Times columnist Simon Edelsten offered a timely analogy. In his 8 November 2025 opinion piece, “AI bubble: don’t throw the baby out with the bathwater,” he warned investors not to mistake short-term volatility for structural failure. His words apply just as clearly to rare earths. The only thing most Western investors saw was an opportunity to profit from panic by shorting the very companies positioned to solve the problem. There was little recognition of fundamentals or of the long-term need for secure supply. The market trades on days and quarters; China plans in decades.

What changes now is time. The market has less than a year before the deferral expires and enforcement can resume without further notice. The pause is administrative, not ideological — a deferral, not a reprieve. MOFCOM 70 contains no provision for renewal; the deferral itself is not renewable. When the year ends, the original controls automatically regain force. The window for Western producers to demonstrate tangible progress is narrow. Momentum must return — not gradually, but decisively — because when the pause ends, Beijing does not need to announce anything new. It simply continues.

Who Are We Really Fighting? The West? China? or the Markets Between Them

It started quietly. In the middle of October 2025, MP Materials began to soften after climbing toward an extraordinary high of around a hundred dollars a share. Nothing in its published numbers justified that price, but nothing justified what came next either. As MP began to fall, it dragged an entire sector with it—Australia Lynas, UK’s Pensana, USA Rare Earths and American Resources from the United States—companies that together represent a large proportion of the West’s attempt to build an independent rare-earth supply chain separate from Chinas monopoly.

In less than three weeks the group lost roughly half its market value. It wasn’t project failure or falling demand; it was the behaviour of markets that now react faster than they think. Watching it happen, felt like observing an automated reaction that no longer knew what it was reacting to.

THE PATTERN BEGINS

It started quietly. In the middle of October 2025, MP Materials began to soften after climbing toward an extraordinary high of around a hundred dollars a share. Nothing in its published numbers justified that price, but nothing justified what came next either. As MP began to fall, it dragged an entire sector with it—Australia Lynas, UK’s Pensana, USA Rare Earths and American Resources from the United States—companies that together represent a large proportion of the West’s attempt to build an independent rare-earth supply chain separate from Chinas monopoly.

In less than three weeks the group lost roughly half its market value. It wasn’t project failure or falling demand; it was the behaviour of markets that now react faster than they think. Watching it happen, felt like observing an automated reaction that no longer knew what it was reacting to.

THE SETUP

Through late September and early October 2025, trading volumes across the sector were unusually high. That was understandable. It came against the backdrop of escalating tension between the United States and China, where rare earths had again become part of the language of economic warfare. Beijing was signalling that it could weaponise its dominance in critical minerals. The rest of the world—particularly the United States—had to demonstrate it could respond.

That mixture of anxiety and opportunity drew investors in, pushing liquidity in rare-earth stocks to its highest levels in years. MP Materials, the largest Western producer with the highest market capitalisation, naturally sat in the crosshairs.

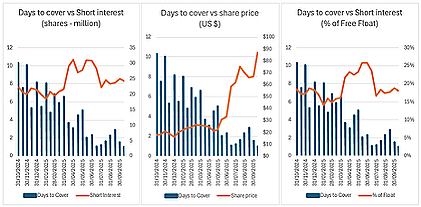

Short interest in MP had been elevated for months—reaching as high 34% of the free float in June 2025—but that extreme level itself didn’t create the selling pressure. At that time, the stock was trading around fifty dollars and the days-to-cover ratio stood at roughly eleven. It would have taken almost two weeks of average volume just to unwind the existing positions. With liquidity that tight, adding to shorts was hazardous: any sustained rally could have left funds unable to buy back shares fast enough to close their positions leaving them exposed to same situation they were exploiting. The scale of the short exposure showed conviction, but it also represented constraint.

What changed was liquidity. As MP edged toward a hundred dollars and trading volumes surged, the days-to-cover ratio collapsed to almost one. Suddenly, the equation flipped. The risk of being trapped disappeared, and with valuations now difficult to defend, the opportunity became irresistible.

By mid-October 2025, nearly eighteen percent of the stock was sold short—well down from Junes 34% but still unusually heavy position for a company of its size. On the following days, more than half of all trades were short sales. Once the first cracks appeared, capital rushed in to widen them.

BEYOND POLICY CONTROL — WHEN MACHINES RUN THE MARKET

Modern equity markets now operate with a level of automation that leaves policymakers reacting to outcomes rather than shaping them. Research by JP Morgan (2017) and the European Securities and Markets Authority (2023) shows that algorithmic and passive strategies account for most of the global trading activity, leaving less than ten percent to traditional discretionary investors.

These systems respond to movement, not motive. As the Bank for International Settlements (2020) observed, automated trading amplifies short-term volatility by reacting to order flow and correlations rather than fundamentals. The subsequent integration of artificial intelligence has intensified this reflex. The BIS (2024) noted that machine-learning models capable of analysing multiple markets simultaneously can reinforce one another when responding to similar signals, accelerating both rallies and declines.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

Most investors outside the UK rarely encounter the mechanics of the London Stock Exchange (LSE), yet those mechanics shape how its company’s trade.

The LSE operates two main electronic systems: SETS, a continuous order book for liquid securities, and SETSqx, a hybrid model for smaller or less-liquid shares that relies on market-maker quotes and four daily auctions. Although both are LSE-domiciled, they connect through global liquidity networks with similar platforms, linking London’s trading flow to exchanges in New York, Frankfurt, Hong Kong, and Singapore. The result is a market, policymakers nominally oversee but no longer have any control—a self-sustaining ecosystem where liquidity, volatility, and sentiment circulate at machine speed.

Algorithmic and AI-based trading now form the reflexes of modern finance—efficient, fast, and largely self-referential. Market behaviour increasingly reflects the logic of code rather than the direction of policy. Decisions made in central banks or ministries move more slowly than the algorithms interpreting them.

THE SLIDE

Once MP began to slip, the machines took over. Large funds now rely on models that react to movement, not motive. They don’t ask why something is falling; they see that it is and search for connected names to trade the same way.

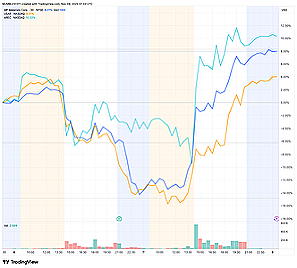

Within days the pattern spread through Lynas, Pensana, USA Rare Earths and to a lesser extent, AREC. Each market followed the next as the trading day moved from New York to Sydney to London.

Figure 2:Lynas, Pensana and AREC moved in lockstep with MP Materials. The sell-off spread globally across time-zones, driven not by fundamentals but by algorithms chasing correlation.

Fundamentals hadn’t changed; the correlation was mechanical. By the third week the decline was feeding on itself. Selling created more selling. For smaller companies like Pensana and USA Rare Earths, whose prices had never reflected even a fraction of their long-term value, the damage was wildly out of proportion

HOW THE SYSTEM AMPLIFIED IT

The rare-earth sell-off offered a clear demonstration of how that system behaves in practice. The link between these companies wasn’t geological; it was digital. All five traded on exchanges visible to the same network of U.S. investors and algorithmic funds. MP and AREC sat on NYSE and NASDAQ; Lynas on the ASX but tracked heavily by U.S. ETFs; Pensana on London’s SETS order book and cross-quoted on the U.S. OTC; USA Rare Earths on the OTCQX.

Every tick and order from these platforms feeds the same data engines. When MP fell, the others lit up on the same screens. Companies

like Mkango and Rainbow, however, trade on SETSqx—a slower, quote-driven system with periodic auctions rather than continuous matching. Their prices update less frequently and don’t feed directly into global trading models.

It wasn’t a question of quality; it was one of exposure. If your stock sits inside that global feedback loop, you move with it whether you deserve to or not.

This structural distinction became critical during the rare-earths sell-off. Pensana, which trades on SETS, appeared continuously in global trading models and was swept into the automated reaction that followed the fall in MP Materials. Mkango (MKA) and Rainbow Rare Earths (RBW), listed on SETSqx, were largely shielded. Their auction-based pricing refreshed too slowly to trigger the same algorithmic responses. The difference was not one of quality or fundamentals—it was structural exposure.

THE BOTTOM

On 6 November MP announced its quarterly results. The figures were solid—strong cash, no unpleasant surprises—but headline-scanning algorithms saw “earnings miss” and sold immediately. The share price dropped six percent within minutes. Then human investors read the report. The picture was fine. Within hours the stock had reversed course, finishing the session roughly twelve percent higher after the close as short sellers scrambled to cover.

The next day, 7 November, the reversal spread across the U.S. market. USA Rare Earths and AREC followed MP’s rebound almost point for point, climbing as the same shorts unwound their positions. That move happened after the London and Sydney markets had closed, which is why Pensana and Lynas didn’t move at the same time—their shares simply couldn’t trade. But for the US traded stocks. It was a textbook bottom—weeks of pressure released in a few hours of forced buying

Figure 3:After MP’s earnings release on 6 November, headline-scanning bots sold first, humans read later. Shorts were forced to cover, sending the whole group sharply higher — the mechanical rebound that marked the floor.

WHAT IT SHOWED

Parts of the sector had overheated, MP Materials most of all. Its valuation had become detached from its published numbers, with Lynas not far behind. But most of the sector, especially the developers, hadn’t yet reflected their underlying fundamentals.

This wasn’t a cleansing correction; it was a mechanical swing that shifted cash, NOT VALUE—mainly from private and retail investors to the trading desks that profit from volatility. MP and Lynas finished the episode still expensive. Everyone else finished it badly bruised and disillusioned.